Competitive Advantage

I encounter startup founders and product builders ecstatic about their product idea, mostly due to their hate for incumbent offerings. "Nobody likes using that! That company is awful! They charge too much! I can create a much better product!"

As a product person at heart, I also get excited about products that look better than the status quo. But excitement about a product doesn't necessarily make for a great opportunity, especially in specific industries and sectors. You have to go big if you're going after financial services or healthcare. You have to do something really unique and really valuable.

Strategies

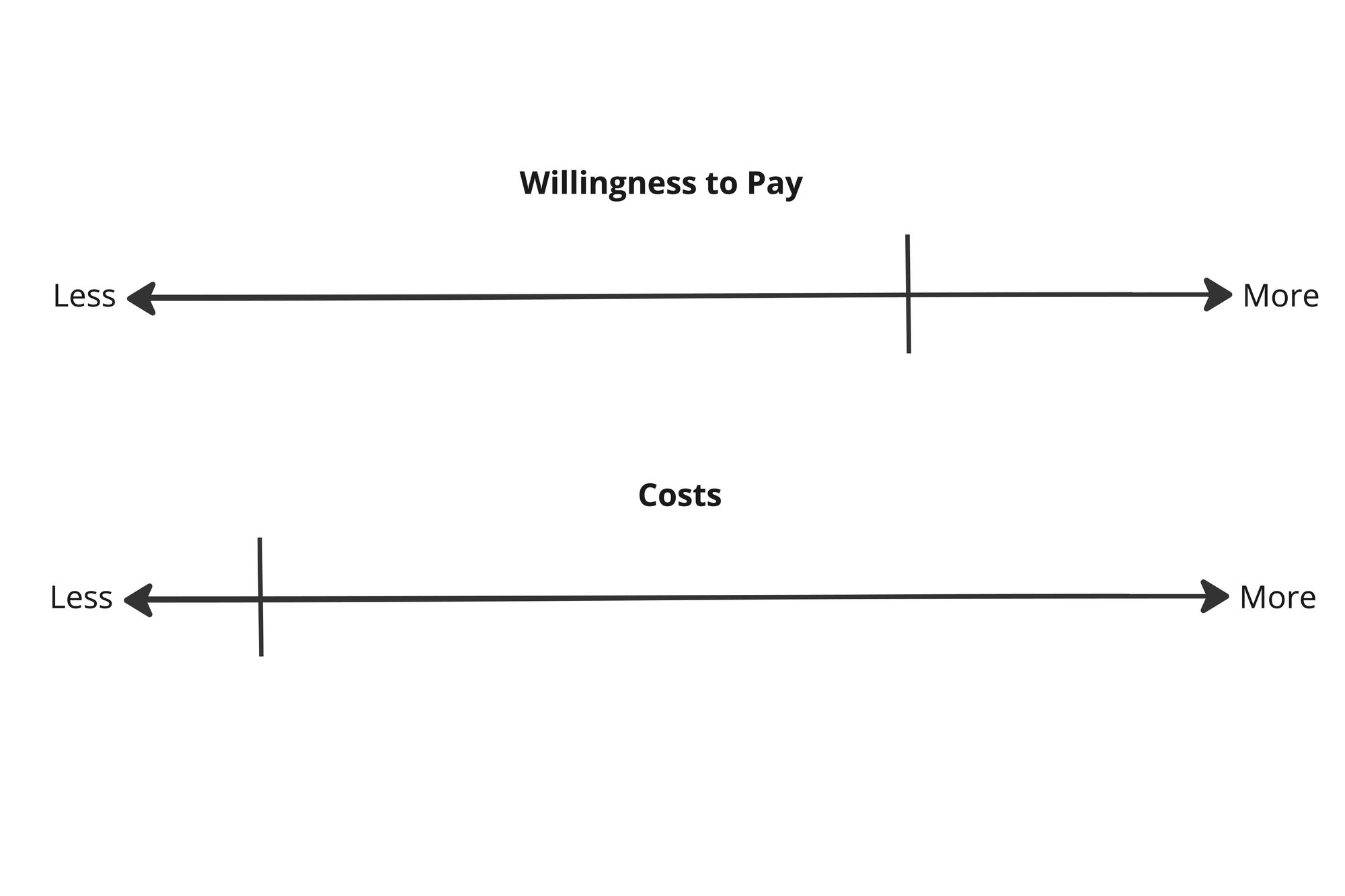

One has a competitive advantage over competitors if they have a wider gap between their costs and the amount customers are willing to pay. To have competitive advantages is to have strengths over rivals.

There are three strategies to widen the wedge:

- Differentiation: Increase willingness to pay at a higher rate than cost offsetting.

- Low-cost: Decrease costs without sacrificing willingness to pay.

- Dual advantage: Simultaneously decreasing costs while increasing willingness to pay.

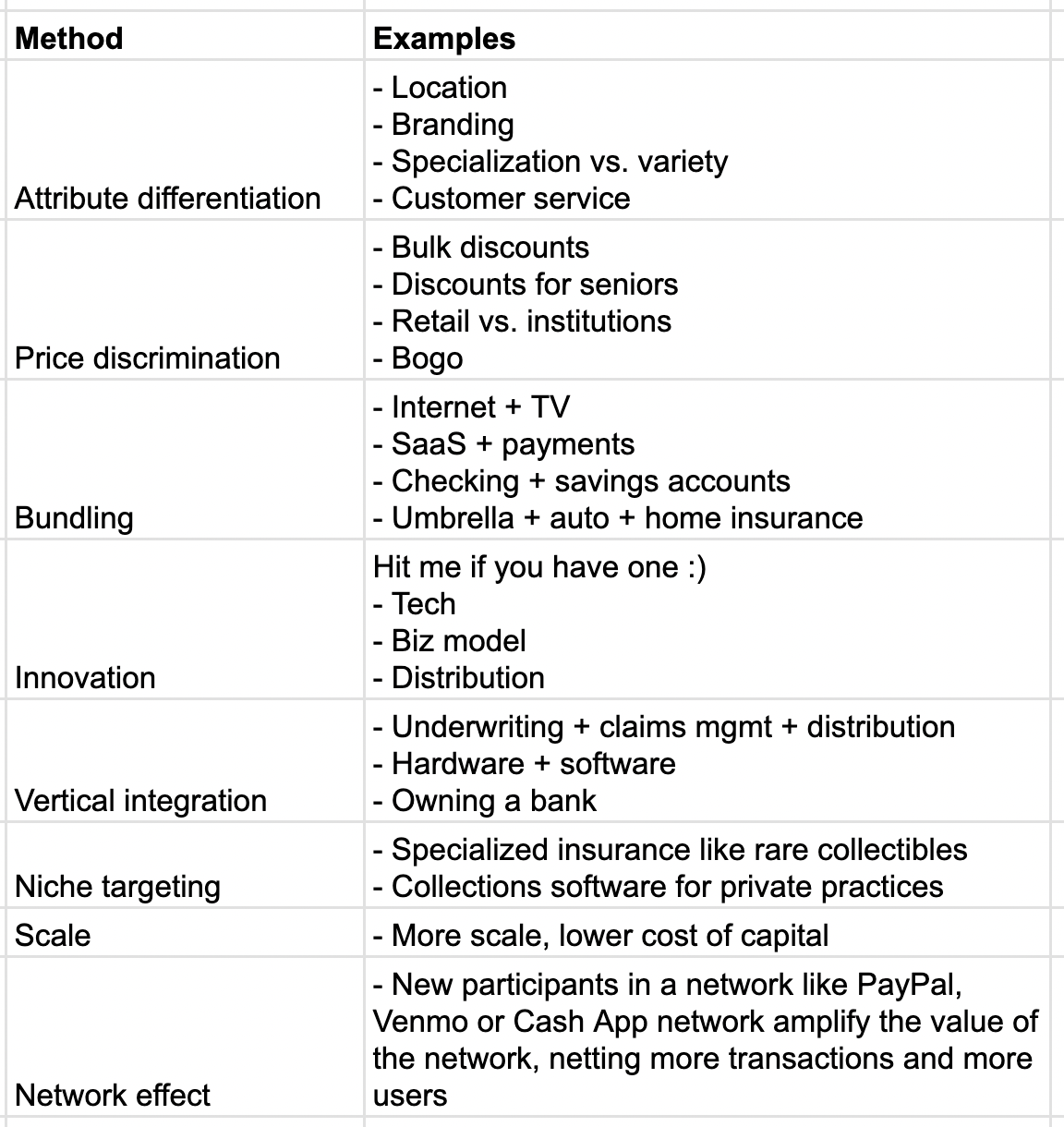

By having a competitive advantage, you inherently have a better product (or the only product) in a market by some unique definition, dependent on your exact case. Below are some methods contributing towards the size of your wedge between costs and willingness to pay.

As an example, network effects were the primary method and reason certain fintech offerings reached success. They made a product like Venmo valuable and unique.

Strongholds

I purposefully excluded regulatory advantages from the list above. They're so important in areas like financial services that I think they should live in a category of their own. I think they're more of a moat and, therefore, barrier to participating in certain capacities than just an input to the size of the wedge.

Incumbents have strongholds in areas like banking and insurance. Those include long-standing customer relationships, deep-rooted expertise, distribution channels, and regulatory access. These are advantages. They make it difficult to enter and compete. But it is possible to compete if you offer something truly unique that customers value and offer it in a truly unique way (some flavor of B2B2C / B2B2E for instance), giving you a business model advantage that an incumbent can't structurally pull off.

Could you develop a competitive advantage?

Here's a simple thought exercise for brainstorming the potential for a competitive advantage: Determine if you're offering something truly valuable and unique.

To qualitatively gauge this, imagine a future where you have traction. Awesome, congrats! Now think about the impacts of your business suddenly disappearing. How disruptive would that be to the value chain? How would customers get by? Who could replace you? How quickly? How dramatic is this?

I think it's appropriate to bucket the concept of competitive advantages with that of moats at the early stages. You won't have them for a while. The early years should literally be a quest towards positioning yourself to eventually grow that gap between costs and willingness to pay. And quest is the right word because it's not guaranteed and will take many years.

Naturally, the concept of scarcity is highly relevant to this topic. It's often easier to charge more and take your time building product the right way for the long term if there aren't 32 others with a similar offering flooding the market, even if yours is superior. Uniqueness matters (read more about busy categories).

What about team?!

Teams are one of the top factors when it comes to startups, so they deserve a section in this post even though it's slightly off-topic.

I always hear this from companies: "our team is our competitive advantage."

Teams aren't competitive advantages. A great team is a differentiator and tool for accomplishing hard, unique things that most people couldn't successfully execute on. And while unique things can often be valuable due to scarcity, value is not a given.

Take our portfolio company, Highnote, and take Nubank for instance. Both have special founders. This helps them accomplish really hard and amazing things; unique things that most others couldn't accomplish. John MacIlwaine led product and tech at Braintree. He was CTO of Lending Club. He led global development at Visa. He was CTO at SunGard. He's special. That makes him uniquely suited to tackle unique problems at Highnote. Highnote has a good chance of ending up with a competitive advantage over time. David Velez was a Stanford grad, and an investor at General Atlantic and Sequoia before founding Nubank. He grew up in South America. He intentionally went directly at Brazil's biggest and most profitable industry knowing it was dominated by five banks who controlled 80% of the market. Nobody else was thinking of entering that space. He intelligently skirted high hurdles for bank charters by launching a credit card instead of a bank account to start. He's special. He saw a unique opportunity in vulnerable incumbents and designed a best-in-class product for the market. Notice he wasn't the 17th neobank competing on a thin value prop. Both John and David are special founders pursuing big, hard, and naturally unique opportunities.

But the fact is that nearly anyone can be special. You're mostly viewed as special after accomplishing something great. So when dreaming about your endeavor, dream about something hard and unique so I can write about how special you are 10 years from now.

Western Union, TransferWise

Let's use Western Union as an example of a dominant player with a competitive advantage, specifically in the global remittance market. WU raked in $4.5b in revenue in 2022.

Factors contributing to its competitive advantage:

- Vast network: Over 500k agent locations globally.

- Established brand: Long history, trust, and widespread recognition.

- Variety of service channels: physical locations, digital.

But it has weaknesses as an incumbent with legacy infrastructure in a modern world evolving quickly:

- Slow[er] transaction speeds: traditional methods can take longer to process than digital offerings.

- Digital adoption: core business was and still is reliant on physical locations. The company isn't a digital native.

- High fees and exchange rate margins: digital-first solutions can have higher margins.

Western Union has a long and fascinating history dating back to the 1850s. The money transfer service was introduced in 1971, pioneering the remittance industry. They've been durable, have had to remain innovative and react to modernization by adopting digital channels. But they clearly have some attractive vulnerabilities.

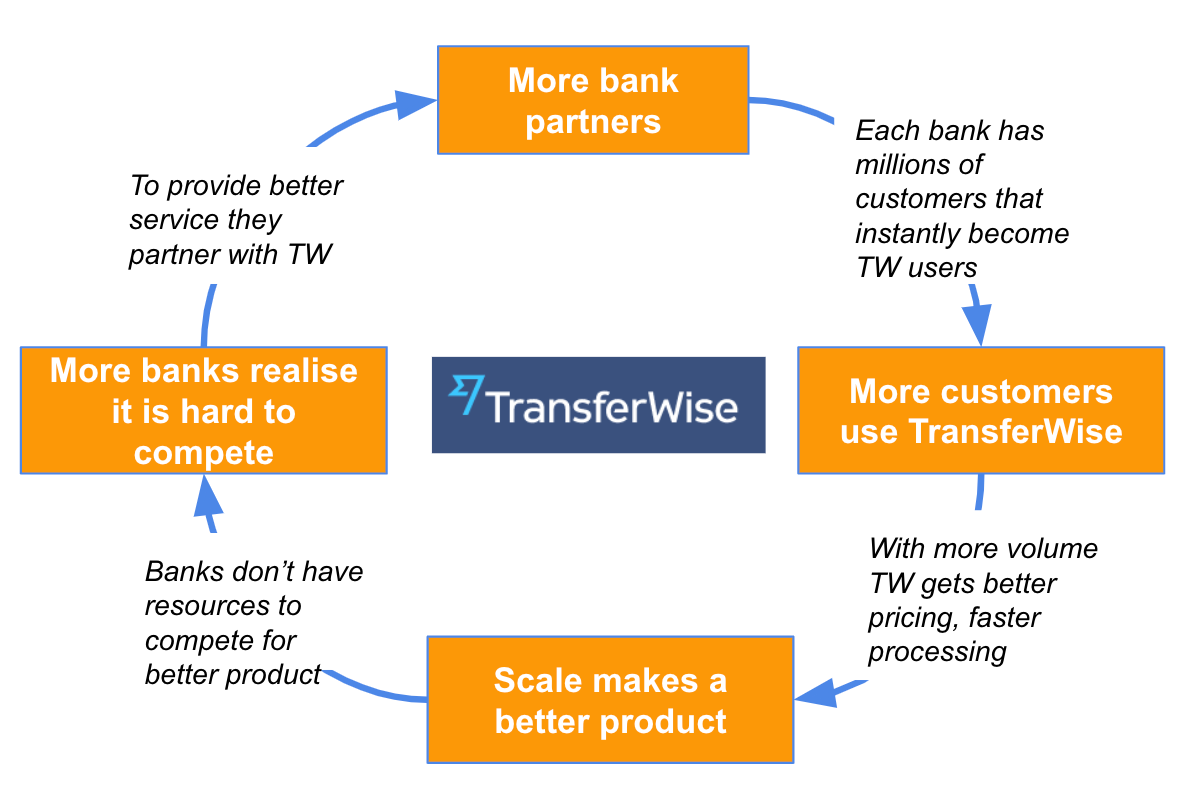

Transferwise (now called Wise) set out to make international money transfers more affordable, more transparent, and more friendly. Like David targeted the Brazilian banks with Nubank, Taavet Hinrikus, and Kristo Kaarmann targeted Western Union and other traditional remittance providers with Transferwise. Here's a great post on their business model and history. Once established, they grew through methods discussed above, like bundling, adding capabilities around P2P payments, direct debits, and savings. They're well on their way on their quest.

Pace, Promise

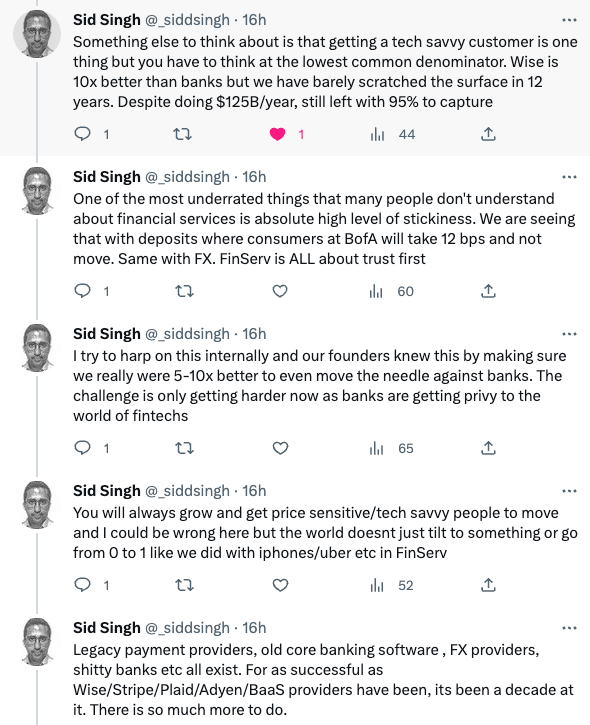

Sid Singh from Wise replied to a recent tweet by Plaid's Bruno on Twitter the other day with insights that are both humbling and promising:

~$800b of global remittences will be sent by migrant workers back to family members in low and middle income countries in 2023. The industry will net ~$37b from fees that senders pay to remit. These flows are estimated to exceed $5t by 2030.

I want to unpack what Sid is highlighting:

- Mexican migrants sent $54b in personal remittances back home in 2021, and sent $59b to relatives in 2022 (2nd highest country behind India at $100b).

The average cost to remit money between US and MX is 4%.

The average Wise cost to move money between USD > MXN is .68%.

So, Wise is economical in this use case. - Wise is arguably 10x better than traditional banks by some definitions.

- Wise does $125b/yr in remittences, and is just scratching the surface.

- Trust is everything in financial services. A slick app, clever marketing, and cheaper fees aren't enough to overcome trust and inherent fear. I think Wealthfront is offering over 4% on deposits right now while Bank of America is under 50bps but you're not seeing a mass exodus from one to the other.

- "Wise/Stripe/Plaid/Adyen/BaaS providers have been, its been a decade at it. There is so much more to do."

This exchange is a great example of trying to penetrate industries dominated by an incumbent with a competitive advantage.

It takes special teams to execute. It takes vulnerabilities in the incumbents structure. It takes a long time to succeed. But it's possible. Lots of opportunity ahead!

Parting Thoughts

Financial service incumbents have a competitive advantage. Competing with them on storing deposits, lending, moving money, investment products, and insurance is hard. But it's not impossible to chizzle away at these monster profit pools.

The last few eras of fintech were exciting, but as Sid says, Wise, Stripe, Plaid, Adyen, etc., have all been at it for over 10 years and have barely made a dent. These are gigantic markets. To make an impact and become a meaningful, durable company, you must work on something truly valuable and truly unique. There needs to be chaos when you envision what happens after you disappear. And you have to expect it to take 10+ years.

Hopefully, this post provides useful references for entrepreneurs thinking about starting a company or pivoting. With the emergence of new platforms and technologies (like LLMs), we (the startup ecosystem) always see an explosion in early-stage entrepreneurship. But we also see a lot of copycats and lower-value offerings. I hope that this post helps push talented entrepreneurs to think big – go after hard, unique, and valuable things. There's a reason that big, weird, crazy ideas from talented people get funded.

Further reading

- Aika's TransferWise and its Many Pivots

- Fintech Ruminations Network Effects in Fintech

- Wise Business Breakdowns pod ep.

- Wise ep. on Wharton Fintech podcast

- Calibrating for a new era of fintech

- Global remittances will surpass $800 billion in volume, but pricing is pressuring revenues

- Western Union 2022 Annual Report

- NFX The Network Effects Bible