Busy Categories

Softsoap

I read The Greatest Business Decisions of All time back in 2012. Fun book.

Chapter 9 featured the story of Robert Taylor and his small Minnesota company, Minnetonka. They introduced Softsoap to the market in 1980. New concept, old industry – liquid hand soap.

This serial entrepreneur knew he couldn't just manufacture the soap, fill bottles, and distribute them. First to market wouldn't be enough. Robert knew he needed to play defense against Proctor & Gamble, the 100-ton gorilla. For a product so great, he knew P&G and other competitors would flood the market quickly after launching. So he spent $7m on a national advertising campaign and $12m to buy every pump (100m at $.12 each) that could be manufactured in the foreseeable future. He bet the company, and it worked. 100+ fast followers entered the market, but not until more than a year later when could they finally get their hands on pumps. In just the first six months, they crossed $25m in sales. Colgate-Palmolive bought Softsoap in 1987.

His timing and bets gave him an incredible distribution and branding advantage.

Two years after Colgate-Palmolive bought Softsoap and a few of Minnetonka's other brands, Unilever bought the rest of his company for $376m. Robert Taylor was prolific at introducing new products, marketing aggressively, and acting boldly to box out new entrants. Robert was a real risk-taker.

Busy Markets

Obviously Softsoap wasn't a pick-and-shovel for the liquid soap industry. But it's relevant to the points in this post because he launched it while it was a nonobvious category, knowing it would become obvious soon after.

You and I see it all the time. Catalysts catapult emerging [technical] markets into popularity. Then a talented founder hacks together an innovative, useful pick-and-shovel, essentially birthing a new category overnight. They get some traction. They seemingly have some PMF. Shortly after, every VC wants a similar pick-and-shovel in their portfolio, many YC companies pivot to the category, and many new entrants ultimately flood the market. The newer entrants may even have subpar teams and products compared to the earlier entrants. But they all have money to spend on marketing and short-term incentives to offer their product cheaper than competitors, often at a loss, in order to get some traction. They may be irrational operators. And just like that, the pick-and-shovel category switched to being obvious instead of nonobvious. Obvious pick-and-shovel businesses are hard to differentiate from one another, hard to compete in, and it's hard to figure out if the eventual winner needs to do much more than outlast everyone else by raising a war chest while hoping the emerging market grows into a mature market one day.

Some example waves we've recently seen are/were around observability in AI, text-to-SQL apps, blockchain analytics, or real-time risk management and security monitoring in crypto.

Frontier [software] markets attract a lot of talent. Barriers to entry are low. Unfortunately, the growth of obvious tools can outpace the growth of attractive buyers. Notice I said, "attractive." Often in emerging categories, the buyers may lack big budget or an appetite for commitment.

These are tricky scenarios that many investors and startup founders find themselves in, especially when money isn't flowing like it was in a zero-interest rate environment.

When you have 7 startups all getting funded at the same time, trying to solve the same problem, it's likely going to be a race to the bottom. They're all on a collision course given they're competing for the same [potentially few] customers. It's not necessarily a recipe for success.

A busy market is one in which Robert Taylor knew they'd be in after introducing Softsoap. The liquid soap category would quickly switch from nonobvious to obvious. The primary lesson here is that Robert knew survival and winning would require extreme measures – bet the company measures. Most products are commodities or become commoditized quicker than entrepreneurs would like to think, especially in hot emerging categories. Being the best product or first to market often isn't enough to make it through busy markets.

Industry Evolution

Robert Taylor was able to box out competitors for a year. But what happens when it's 2023, and you're building software? You can't just buy all of the widgets ahead of fast-followers to slow them down. For this, it is valuable to step back and think about the evolution of markets.

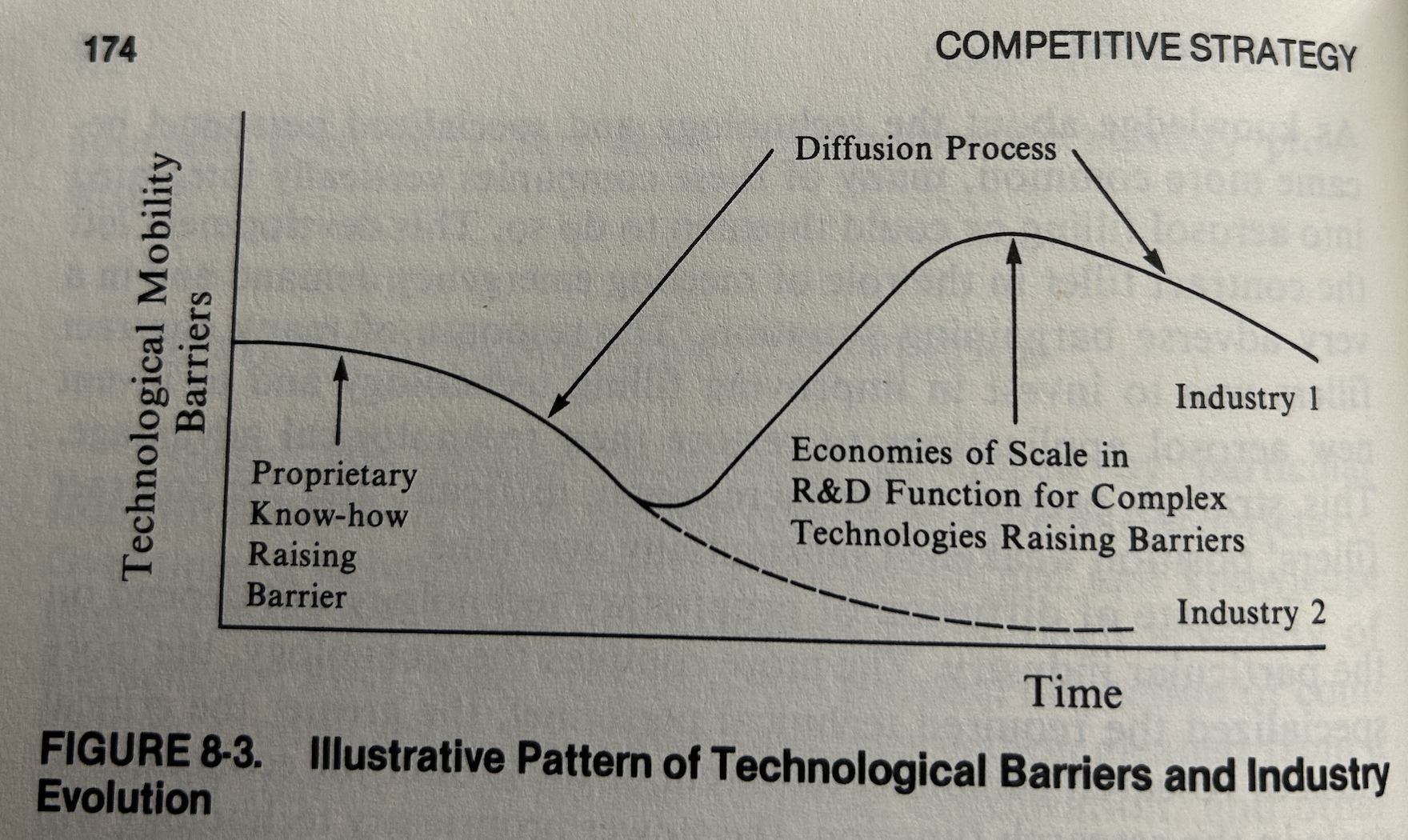

Chapter 8 of Michael Porters' Competitive Strategy is one of my favorites. It describes the evolutionary processes involved as a market moves from its initial structure toward its potential structure.

- Long-run changes in growth

- Changes in buyer segments served

- Buyer's learning

- Reduction of uncertainty

- Diffusion of proprietary knowledge

- Accumulation of experience

- Expansion (or contraction) in scale

- Changes in input and currency costs

- Product innovation

- Marketing innovation

- Process innovation

- Structural change in adjacent industries

- Government policy change

- Entries and exits

Diffusion of proprietary knowledge is one of the processes that talented software startup founders in busy markets seem to underappreciate the most. Obvious pick-and-shovel businesses get commoditized really fast.

Proprietary advantages tend to erode quickly in busy markets. This is one of the main reasons a category becomes busy in the first place – it's really easy for competitors to spring up and for the relatively small customer pool to bounce around.

"The rate of diffusion of proprietary technology will depend on the particular industry. The more complex the technology, the more specialized the required technical personnel, the greater the critical mass of research personnel required, or the greater the economies of scale in the research function, the slower proprietary technology will be to diffuse. When heavy capital requirements and economies of scale in R&D confront imitators, proprietary technology can provide a lasting mobility barrier."

Patent protection is a key offsetting force, albeit rarely interesting to hide behind. The other is "the continual creation of new proprietary technology through R&D. New knowledge will provide companies with additional periods of proprietary advantages."

Naturally, a busy category likely has a very short diffusion process. If it didn't, it likely wouldn't be too busy. By the time a category is obvious, the diffusion process has accelerated. To have a shot at surviving and thriving through a busy emerging market, you need to hire insanely special talent, get traction, and continually leverage the scale for further technological development. Keep the product velocity and customer learnings going! Your initial technical barriers are not strong in a busy market with a short diffusion process. Think deeply about how you'll compound barriers. Just being early to market won't be enough, and you can't buy time by boxing out competitors from offering a competitive alternative.

Parting Questions

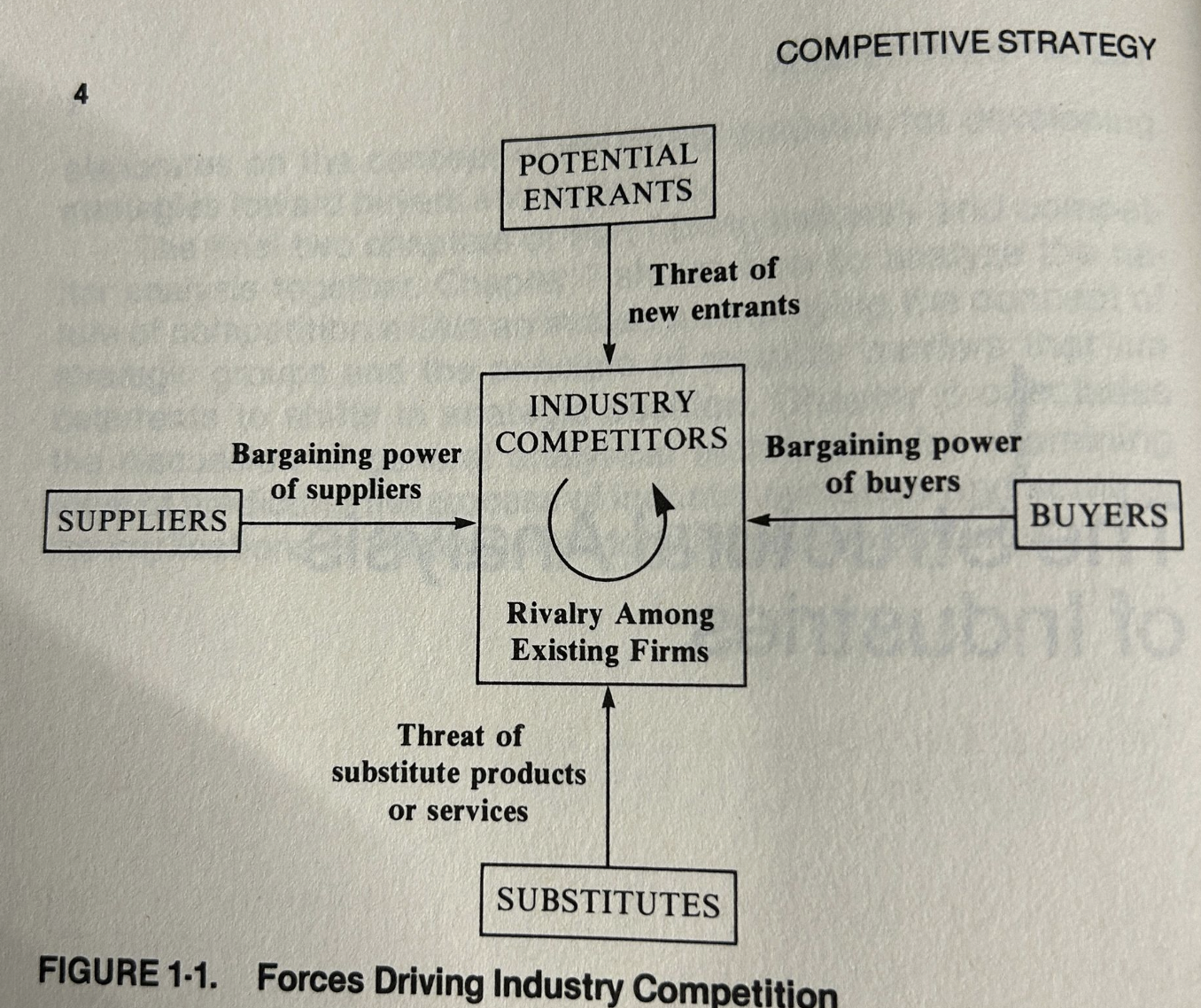

We're all familiar with the five basic competitive forces. But many often need to remember to think about their impacts on the profit potential of an entire category and, therefore, on each competitor. The more competitors, the fewer the attractive pool of buyers, the more intense the competition, the busier the category.

Defense is hard, especially in software, especially without scale. You can't hold competitors back by a year to two by buying up a critical widget.

If you have an obvious pick-and-shovel idea, it's smart to operate under the assumption that it'll become commoditized quickly after launching. The market will become busy, fast. Someone with a weaker product will still raise more money than you, spend more than you on marketing, and charge customers less (maybe even offer it for free for a while).

What's your answer for how you'll win in a busy market?

- Why will value accrue to you?

- How will you get as many of the attractive buyers in the emerging market to pay for your product?

- How will you make your product so sticky that the only way for customers to churn is if they go out of business?

- Can you compound technical barriers by leveraging early scale for further technical development?

- Are you ready to make bet-the-company-sized risks?