B2B2C / B2B2B / B2B2E

People often ask me areas of fintech that I'm excited about. Like many, embedded fintech is one of them. More particularly, startups with B2B2X business models. Notice I didn't just say 'distribution models,' but, 'business models.' Companies that do B2B2X well have it engrained in their DNA – it's core to how their products function, their unit economics, and their operations. Benefits go beyond acquiring a user. They extend to offering a product that's incredibly useful to a user at a relevant time of need.

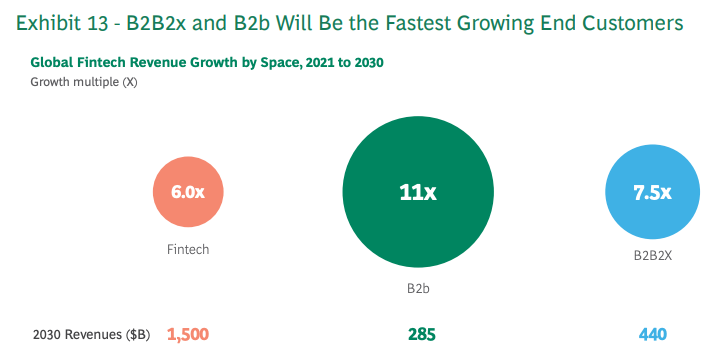

I'm not alone. BCG and QED highlight their excitement for B2B2x in this recent report. "B2B2X [fintech] already represents a fast-growing segment, and there is still room for it to spread its wings. The market is expected to grow at a 25% CAGR to reach $440 billion in annual revenues by 2030."

I've worked at several B2B2C fintech companies over the years.

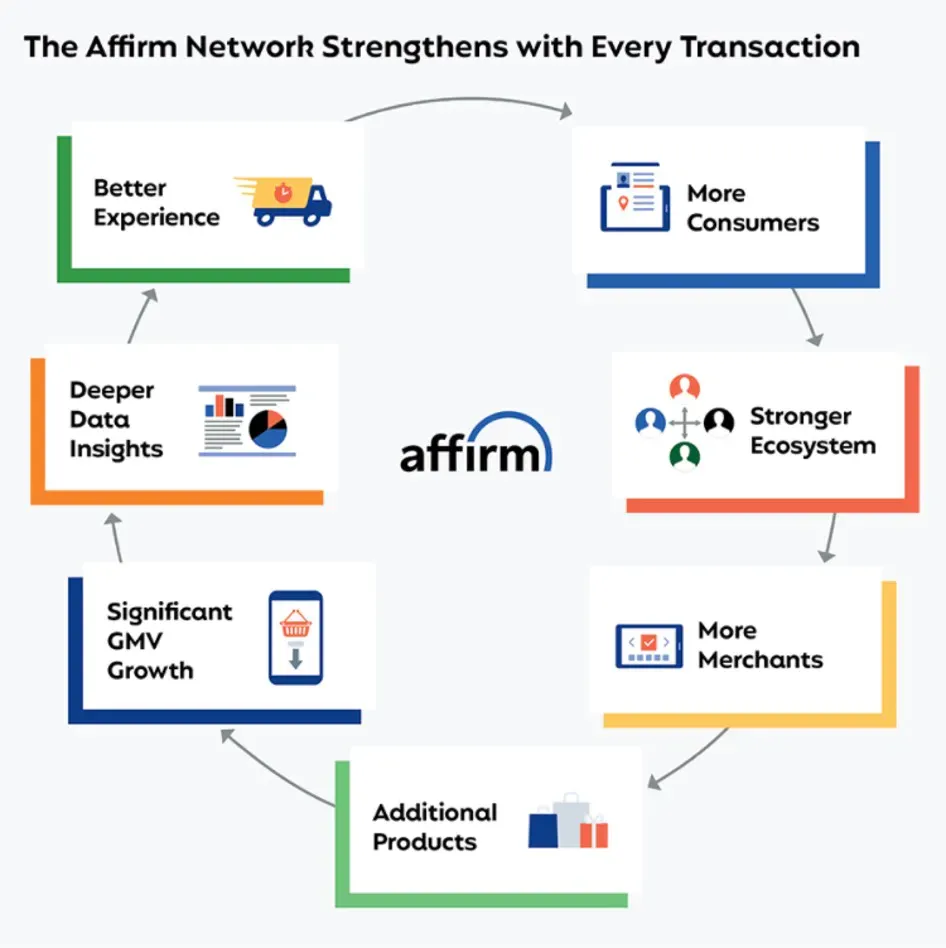

- BillMeLater (now called PayPal Credit): Offered alternative credit at checkout to shoppers on merchant websites like Walmart, Overstock, JetBlue, and hotels.com.

- Blispay: Offered financing (and an everyday credit card) to shoppers of SMB's at the point of sale in-store and online at omni-channel merchants like Murdochs and Evo.

- Alliance Data: One of the oldest forms of B2B2C in fintech, offering private label and co-branded credit cards to shoppers at retailers like J.Crew and Victoria's Secret.

The model is complex, but it continues to present exciting opportunities for innovation, particularly within the fintech and healthcare sectors. In this post, I'll explore these models and highlight considerations for teams as they design their B2B2X strategy.

B2B2C and B2B2E Examples

B2B2C (Business-to-Business-to-Consumer) and B2B2E (Business-to-Business-to-Employee) involve partnering with other businesses to deliver value-added products or services to end customers or employees. This is unique from a purely white labeled model or channel partner model because in B2B2X, the first B ultimately has a direct relationship with the end customer or employee.

Examples

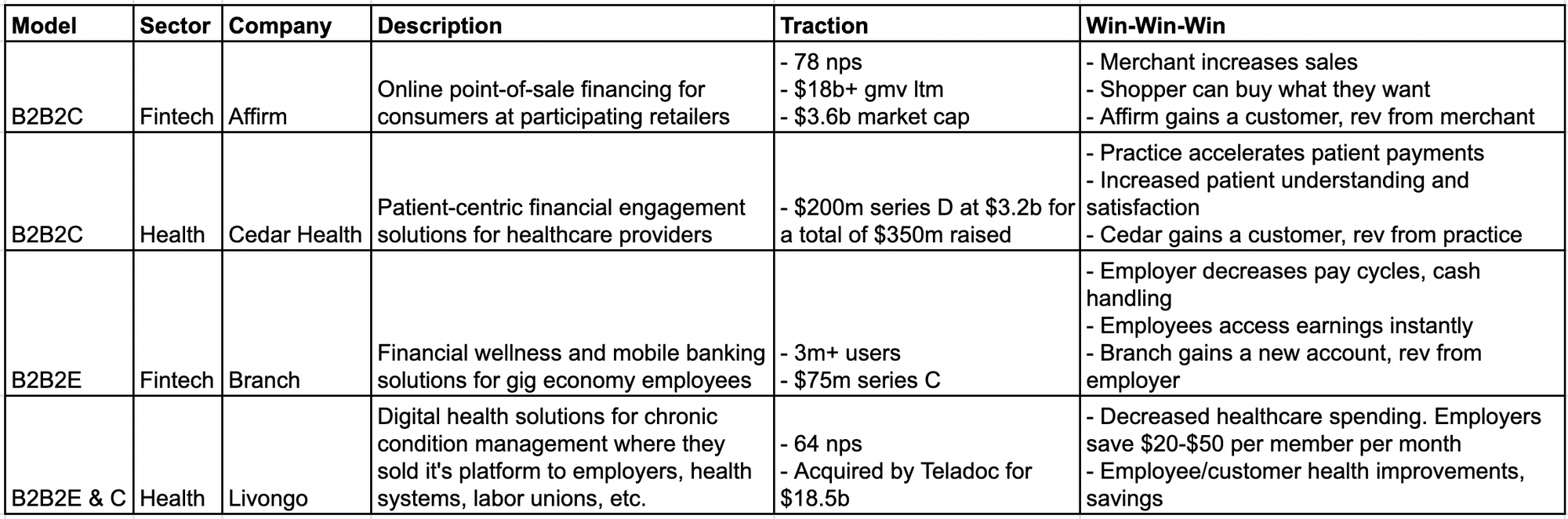

Affirm, Cedar Health, Branch, and Livongo are fun examples to think about across fintech and healthcare.

Noteworthy commonalities:

- High NPS (of the service directly, or by the end user of the middle B who is offering it). Either way, end customers tend to love these products.

- Clear Win-Win-Wins, perhaps my favorite part about these models. They only work when every party is benefiting.

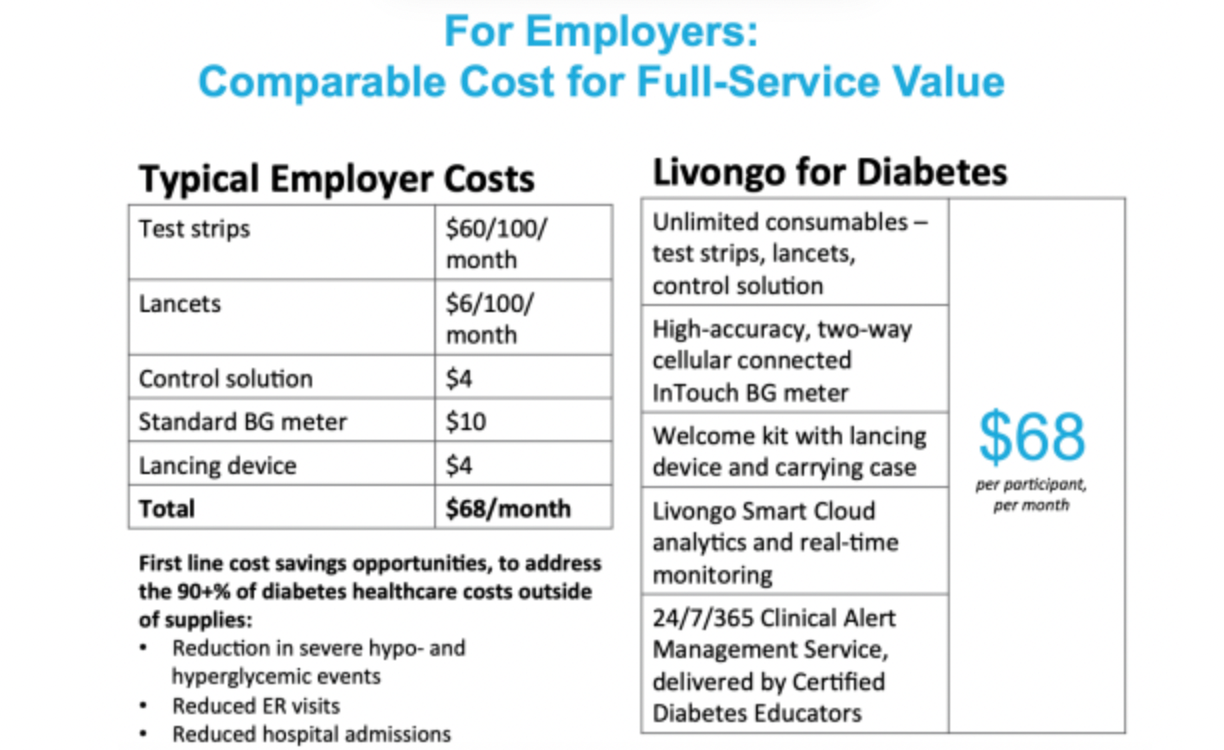

Let's touch on Livongo for those who aren't familiar (ignoring recent events since the Teladoc acquisition). Incentives in healthcare are fundamentally misaligned usually. Providers make more money from sick patients than healthy ones, punting prevention out the window. I actually covered some of these issues and what healthcare 3.0 may look like in this post. Anyway, in the case of Livongo, they decided to make self-insured employers their primary customer – those who paid for patient care. Healthy patients/employees meant lower insurance bills and less sick days. This is how they landed on charging employers a monthly fee per member (employee) and a B2B2C business model. The insight that employers could save money by promoting good health, that Livongo they could charge for this, and that members would benefit made for a great win-win-win. Livongo also did some revolutionary things such as giving out test strips for free.

From a business development perspective, other payers like insurance companies wanted to resell Livongo after seeing the success of large self-insured employers. Like all sales, the first 10 can be much harder than the next 100. From 2015 to 2017, Livongo grew from 6k members to 53k, 30 clients to 200, and $2.3m in revenue to $30m. They reached $68m in revenue in 2018, expanded verticals to hypertension, and went public in 2019.

I'm ready for the next ambitious, passionate entrepreneur to pick back up and find a way to offer insulin and test strips and CGMs at no cost to patients (my wife has T1)!

Designing a B2B2X Product

When thinking through a B2B2X startup idea, an obvious starting point is thinking through the win-win-wins for all parties involved. Beyond that, here are additional considerations:

- What does the flywheel look like? Does it strengthen with each additional middle B and/or end C or E?

- How does the B2B partnership add value to the core product or service offerings? How is value amplified within the ecosystem?

- What's your customer (middle B) selection process and guardrails? You'll likely need to be very selective to manage risk and costs appropriately.

- How scalable is the B2B partnership?

- How can you capitalize on network effects?

- What operational efficiencies and competitive advantages are gained through the B2B partnership?

- Does the B2B partnership help reduce operational risks?

- What has to be true to achieve complete incentive alignment between the B's?

- What are the KPIs each B will monitor and hold each other accountable for to track the partnerships success?

- What's the sales motion that makes sense for attaining the middle B?

- What's the integration process going to look like between the B's?

- What's the ongoing engagement model have to look like between the B's?

- Who owns the end customer or employer servicing responsibilities for various scenarios?

Key Challenges

It's worth highlighting a few common gotchas that will be harder to deal with than you'd think. With that said, these are always challenging when it comes to dealing with businesses, especially at the enterprise level.

- Education & training.

- Initial integration.

- Initial and ongoing customization.

- Ongoing relationship management.

- Customer service and complaints.

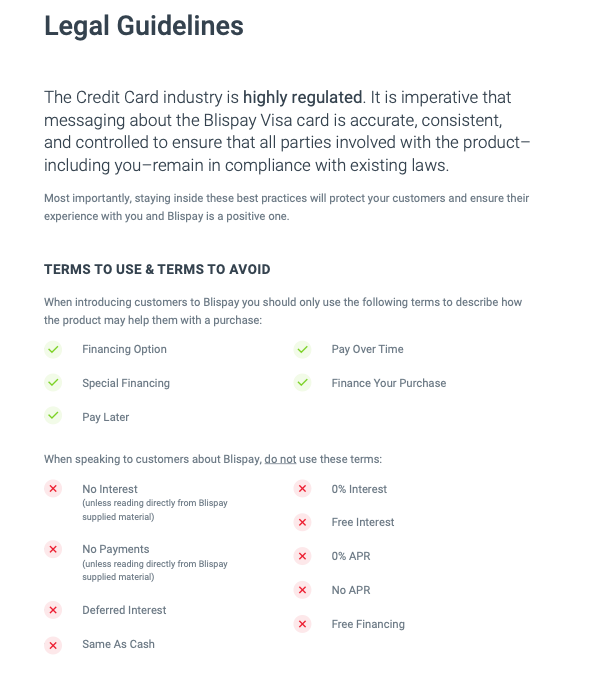

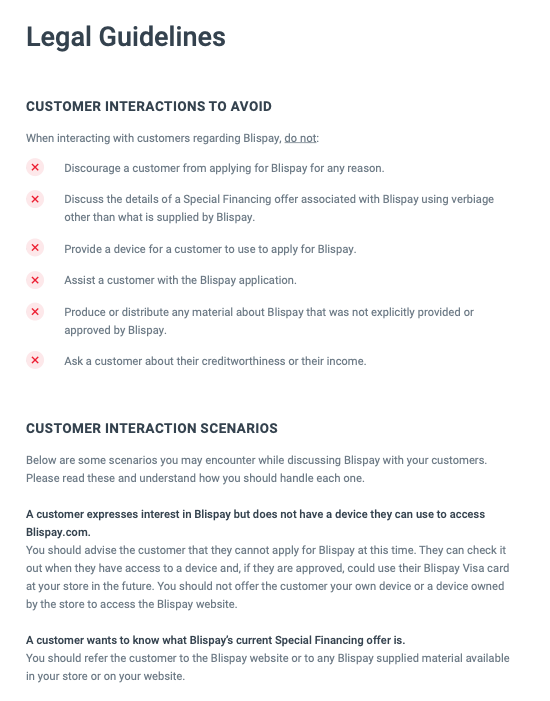

It doesn't matter how detailed you get with documentation. You'll have to hand-hold partners in every department including product people, developers, designers, customer service, finance departments, etc. Below is an example implementation guide we created a while back at Blispay. Guides are never enough to get a partner up and running on their own. They're useful as a reference, and little more.

Conclusion

There is still immense potential for innovation in the fintech and healthcare sectors by leveraging B2B2C and B2B2E business models. These models impact not just distribution, but also product, organizational design, unit economics and revenue models. Although these models are complex and challenging to execute, I'm hopeful that ambitious founders with some thoughtful design and strategic thinking will birth many exciting new B2B2X companies over the next decade. And like most technological advancements (including recently around AI), it's you and I, the end users, who benefit most from these products – another reason to be excited about the future!

References