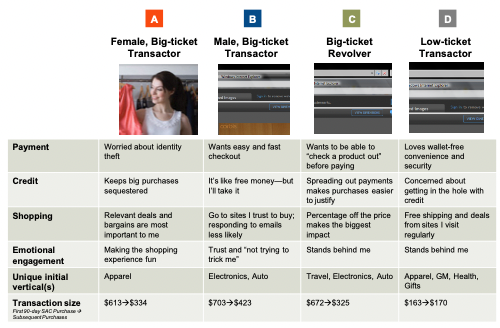

Customer selection is critical across fintech

Pop quiz

Would you prefer to get your hands on a list of 5,000 prospects or 25,000?

25,000, right?

Most enterprise sales folks will answer correctly, but others often don't, especially fintech folks (until they're battle-hardened after many years on the job).

It depends! You'd want the one with more quality prospects. The incumbents know this, so you need to as well. If you can't survive, you can't create immense value. Be selective to be protective.

I love fintech founders. Many waltz around with rose colored glasses while dreaming about financial inclusion and a future better than the past. It's why I was a practitioner for so long at various fintech companies prior to becoming an investor. I'm one of these people at heart. But it took me a long time to learn something that many new founders and even investors dabbling in fintech need to appreciate: thoughtful customer selection.

Thoughtful customer selection in practice

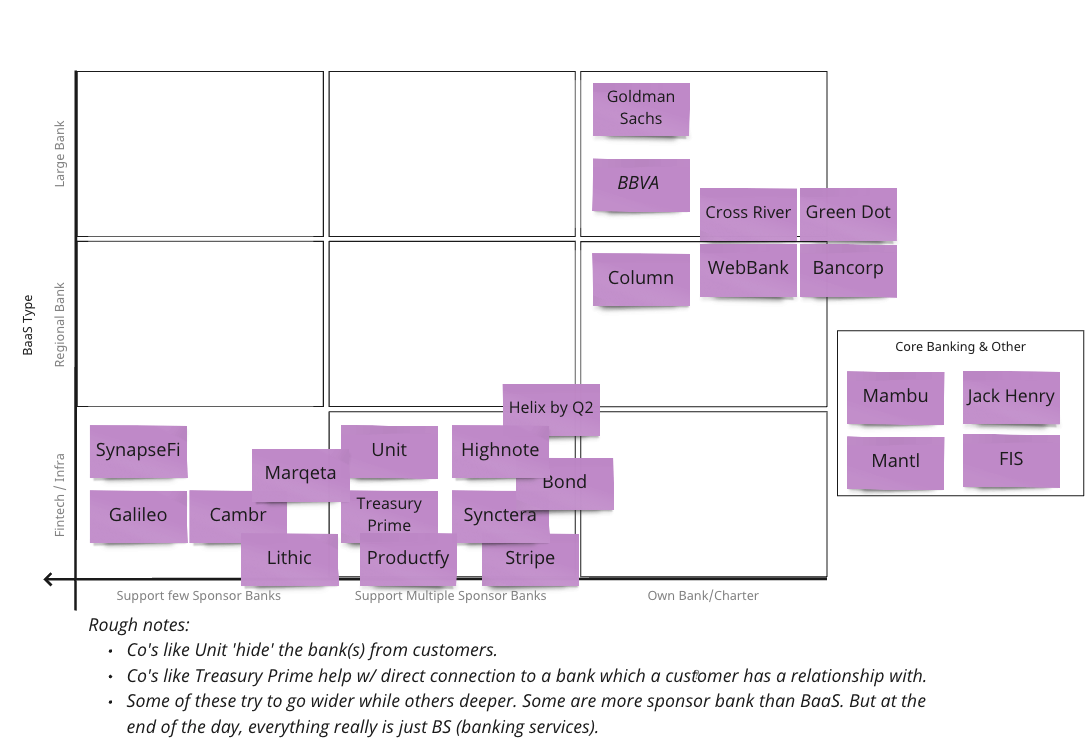

BaaS infra providers & sponsor banks

It's not perfect but slapped this diagram together quickly as a landscape refresher for myself.

The space has a few players. The devil is in the details. Many of these don't offer the same services or target the same customer segments. For instance, Green Dot has fewer programs but they're comprised of large customers with large customer bases (like Walmart, Uber, and Apple). Arguably, the space is large enough for many competitors. These aren't winner take all markets. But not all of these will survive. Sometimes, the ones who grow the fastest out of the gate are quick to plateau. Regulatory and operational burdens are challenging to scale responsibly.

Sponsor banks choose their customers carefully because a single customer can bring them down. They're assuming the risk. They have the most to lose. People complain about how they aren't easy to work with or aren't willing to work with them at all. But you have to see it from their perspective. They're going to work with customers who are some combo of:

- Least likely to get them in trouble.

- Most trustworthy and experienced teams who understand compliance and risk.

- Have sufficient backing from top investors and the likelihood to raise more when needed.

- Outside of grey or red zones.

- Have solid chances of immense growth and long-term survival.

Therefore, most startups that go to sponsor banks will get turned away. Or they may not quite get assigned the A team when going through the sales or onboarding process. They may get extra scrutinized. Ultimately this leads to a widespread belief that "sponsor banks suck to work with and aren't sufficient and should be displaced."

I think most of this applies to BaaS infra providers as well. They should be relatively selective in who they work with, looking for customers with the same lens outlined above. But since they don't bear as much risk, they can often move a bit quicker and are willing to be more flexible. There's a cultural difference. But you likely don't want to be the provider taking the customers nobody else wants. That's the dangerous self-selection that takes place. But if you raise money, you need to grow, and you'll do whatever it takes. So this is an example where someone may grow quickly, be able to raise even more, but ultimately reach a plateau, especially if their sponsor bank(s) step in to slow them down.

BNPL

I worked at two BNPL companies: BillMeLater (now called PayPal Credit) and Blispay (acquired by Alliance Data). In a way, can maybe include ADS in there but I prefer not to. B2b2c lenders need to strive to get two things right:

- Merchant mix

- Consumer mix

Obvious, right? Merchants bring in the customers. Therefore, get as many merchants as possible, right? Wrong.

You need to identify and partner with the right merchants. Customer bases are unique. Some are more creditworthy or needy than others. It's a tough act to balance. Your marketing and sales team will want to bring in as many merchants as possible, while your risk and underwriting team will want as many qualified consumer applicants as possible. Even worse, your investors may not understand why you can't be everything to everyone or why your growth doesn't look like a social media app.

At Blispay, Jared Young spearheaded our effort to segment merchants properly. He defined a methodology for cataloging by tier, with 1 being the most attractive (by application count, approval rate, and consumer mix). He analyzed early partners and provided a framework for best qualifying inbound prospects and our outbound efforts. With a framework in place, you can properly align your entire organization.

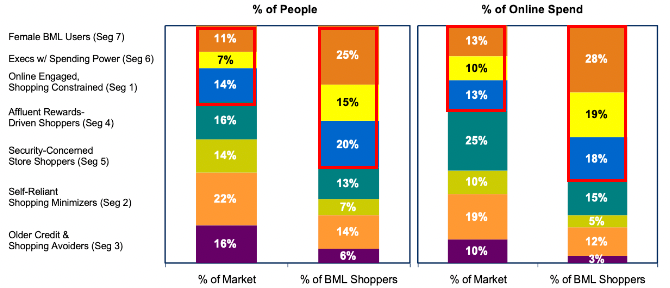

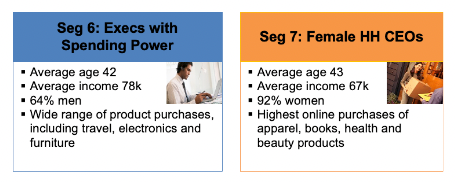

BillMeLater was extremely data driven and intentional. I didn't appreciate how great they were at this at the time (12 years ago, and my first professional job). Carolyn Groobey, Greg Lisiewski, and many others were/are top notch. This led us to leaning heavily into the "Female Household CEOs" and "Professionals with Spending Power" segments. By identifying attractive customer segments from a business standpoint, you can then focus on addressing their needs and cater to their behaviors. You can align the entire organization to fuel growth. It flows to product decisions, marketing campaigns, merchant sales efforts, etc.

They really, really dug in and aligned the entire organization accordingly...

Customer segmentation and intentionality is critical. There's nothing more naive than a pitch touting proprietary alternative underwriting models to be able to lend to anybody with the proper terms out the gate. It misses too many important points. Similar to sponsor banks and BaaS providers, b2b2c lenders must be selective in who they partner with and bring on as customers. You likely don't want to be the provider willing to accept all of the merchants others are rejecting for a BNPL service or all of the consumers that nobody else will lend to. The alternative shows impressive growth out of the gate but goes out of business just as fast. With that said, it's a generality. There are some exceptions that I'd be glad to chat about offline with anyone interested.

The fintech feeder system

Both examples above show that some businesses and consumers aren't well served. This is what I'm calling the fintech feeder system. Anyone doing customer discovery will easily identify these gaps. Founders will start companies based on these findings and investors will continue to fund them. There will forever be problems to solve in fintech and underserved people to solve them for. And I actually love this about the space. But it's also dangerous.

Founder tips

- You likely haven't landed upon undiscovered land if you find a customer segment poorly served by the financial services market. It's likely that other providers purposefully aren't serving them. Recognize that you need an insight and breakthrough in technology or approach to be able to serve an unhappy or underserved audience sustainably, no matter how well-intentioned you are. Be thoughtful from day 0 with customer selection.

- Treat customer selection like a first-class citizen while crafting your idea. And certainly while pitching seed investors. Seasoned fintech investors will want to talk about this anyway. And those who are less seasoned may not know to talk about it but will surely bring it up when your growth doesn't resemble that of a hockey stick like they may be used to in some other consumer sectors. Avoid this misalignment by partnering with investors who understand that most areas of fintech are fundamentally unique, which will impact your expenses, organizational structure, GTM, growth rate, and business model.

- Similar to investors who don't have fintech experience, employees who have worked in high-growth sectors will have trouble grokking why things need to go differently from how they did in their past. Growth tactics, marketing content, speed, flexibility, review flows – all of these will break their brain. You'll need to be really thoughtful in who you bring on to lead different parts of the organization, including sales, marketing, and customer support. Not everything translates.

- If you think moving up-market (to large FIs or merchants) will be required to survive long term, then don't just assume you'll start out mid-market and make the transition over time. Suss out signal early on, and consider starting there from the beginning.

Let's discuss

While I think the content in this post is directionally right for most situations, I recognize that it doesn't apply to all. Firstly, there are many areas of fintech. I just honed in on a couple. Secondly, there are counterexamples to those I supplied above. In fact, I have a great one involving a leading BNPL provider who partnered with a multi-billion dollar retailer with a hideous loan book that still ended up more successful than Blispay (where we focused on lending to a high-quality customer base with an average FICO of 741).

The top takeaway from this post is to be extra thoughtful regarding customer selection when exploring an idea and pitching investors.

I'd love to chat about anything in this post that triggered you (positively or negatively). Reach out to riff.