Calibrating for a new era of fintech

Early-stage venture is more art than science. It's a never-ending calibration exercise. Drafting this helped me think through:

- The 2009-2021 market cycle

- The highest valued fintech companies

- If fintech is as investible going forward

- Optimizing for breakout winners

2009+: When fintech became cool

Some of the most loved financial brands of all time were created since 2009 like Venmo, Stripe, Apple Pay, and Square (ugh, Block).

I think 2009 kicked off the period of fintech becoming "cool" for builders and investors. Company formation and investment ramped up as the decade progressed.

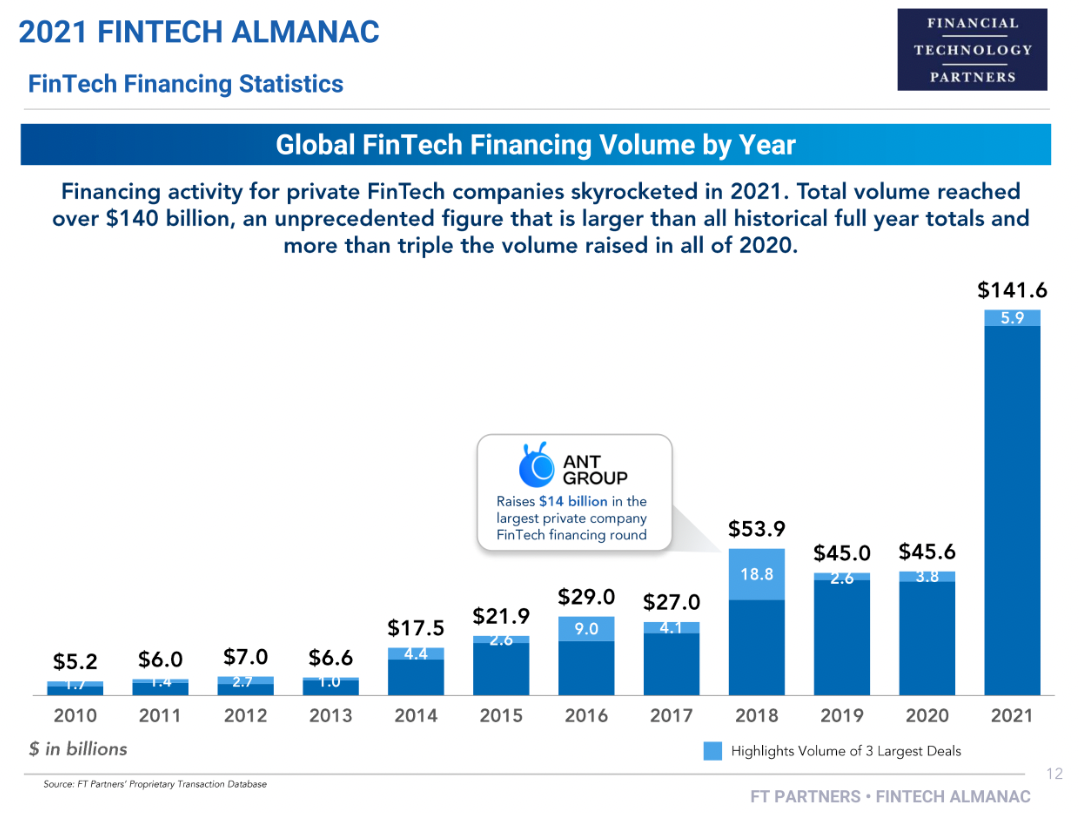

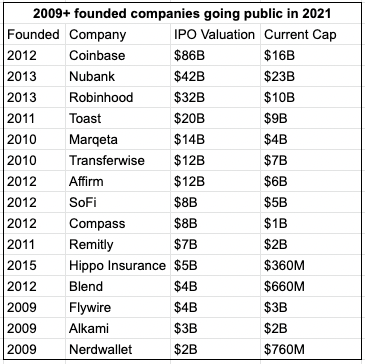

2009 and 2021 were bookends on a market cycle. 2009 was the year with fewest IPOs. 2021 was the year with the most. It got frothy across the board. Fintech was no exception.

According to SVB, "the number of deals larger than $100M jumped from 333 in 2020 to 601 as of Q3 2021."

Not to mention some M&A that already seems like a lifetime ago. Acquisitions like Square buying Afterpay ($29B) and Intuit buying Credit Karma ($7B). And mergers of giants like FIS & Worldpay ($35B), Fiserv & First Data ($22B), and Global Payments & TSYS ($22B).

Catalysts for the burgeoning fintech ecosystem

I think there are five reasons why fintech became so cool in the 2010s.

- The GFC

The global financial crisis of 2007-2008 was a significant catalyst for financial technology and newer models of servicing customers. It brought mistrust and anger towards banks while also resulting in regulation that significantly increased compliance costs. Both of these contributed to a wave of talent who was both capable and passionate about unbundling banks and providing better services. - Cloud + Digital + Mobile

Around the time of the worst economic disaster in decades, Amazon launched revolutionary products like S3 (cloud storage), EC2 (elastic cloud compute), and RDS (oltp db). The first iPhone and the public developer beta release of Android were released in 2007. The ability to efficiently develop products that could reach digitally savvy customers was a game changer for new entrants competing with incumbents. - Early startup successes

By the time 2009 came around, there were some successes and several innovative companies early in their lifecycle. Zoot was nearly 20 years old. PayPal and BillMeLater were both around for about a decade at that point. Bill.com, Mint, OnDeck, Betterment, Zong, and Payoneer were just a few years old. - Composability & fintech infra for fintech

Fintech infra providers born during this period, like Stripe, Plaid, Marqeta, and Alloy, made it easier than ever for other fintech companies to get started or for non-fintech companies to offer financial services, greasing the flywheel. The barrier to entry decreased significantly. - Sponsor banks

This may surprise some, but there are banks behind non-bank fintech companies (that's the "issued by xyz bank" on the footer of your favorite neobanks' site). Often they're smaller banks. Partnering with fintech startups enables these less tech-savvy financial institutions to grow without competing on direct customer acquisition. Growth is critical given the industry is consolidating with less than half as many banks today as there were in 1990, and many were in rough shape after the GFC. Some of the most active sponsor banks include Cross River, Sutton, Celtic, WebBank, Comenity, Bancorp, Nbkc, and Evolve. Many also happen to be in Utah, which could perhaps be named the fintech capital of the US. With more banks willing to support non-banks, more fintech companies could be supported.

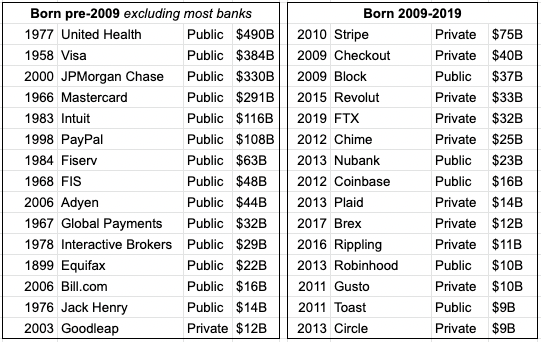

Most Loved ≠ Highest Valued

While many of the most loved companies and products were created in recent years, most of the highest-valued companies are much older. They aren't generally thought of as being as well-liked or even widely known.

Empire building and compounding takes decades, so it makes sense for older companies, on average, to be worth more than younger companies.

Nonetheless, below are a few thoughts that came to mind while constructing this table.

- Stripe is the outlier.

- Companies on the right are obsessive about a great user experience.

- The most valuable companies are the actual banks and insurance companies.

- Banks have proven to be incredibly resistant to disruption. These are massive businesses with deep moats, sticky customers, and strong network effects.

- Insuretechs haven't really broken out yet, despite a few exits. It seems like bank-like and insurance-like startups will ultimately be valued like their 'boring' legacy incumbents. Like others, I'm curious about what that will mean for modern BaaS banks in the future (like Column).

- Joel Monegro's fat protocol thesis may be relatively applicable to the fintech sector. Will the market cap of the underlying banks and insurance companies (base layers) grow more than the value of the companies (applications) built on top of them?

- We've seen fintech companies acquire charters (like Varo with a $2.5B valuation) and new startups start with a bank from day 1 (like Column). Buying and operating a bank isn't for the impatient, but there's reason to believe it's a viable strategy to become a breakout winner. I spoke about this recently with Alex Johnson. He highlighted how good LendingClub ($1.3B market cap) finally looks following their acquisition of Radius Bank, enjoying record revenue and profitability. Square has one now as well. Complicated topic that has been discussed for years. But maybe it is actually necessary to eventually grow into $100B+ companies instead of $1-10B. Can you really displace and compete with them if you aren't one yourself?

- Some of the most interesting breakouts were very differentiated. Some weren't competing with banks at all. And most private market valuations are rather generous given the retreat in those who went public in 2021.

Bloom Credits' Matt Harris phrased it like this:

Consensus fintech is not performing well. Everyone got marked up.

Consensus fintech defined by neobank, frontend'ish insuretechs backed by a reinsurer, and marketplace lenders.

Companies that offer products that are competitive with incumbent financial institutions.

Fintech will remain hot, but won't be as cool

Here's what hasn't changed since 2009:

- Incumbents are slow.

- Incumbents are smart.

- These markets are ginormous.

- Usually room for many winners.

- Often don't need to be first to market.

- Winners can remain winners for decades.

- Secular and cyclical shifts always create unique opportunities.

- Few customers love incumbent providers of financial services or infrastructure.

But 2021 was an anomaly. It was an end cap on a fun period of fintech becoming cool. Late-stage private market valuations still need to reset, and that ripple effect needs to play out. What was considered cool before won't be as cool going forward. As Matt said, consensus fintech isn't performing. What's considered consensus will change, but we don't yet know how. Rebalancing to normal isn't as easy as it sounds like it should be. This is how cycles go. I have no doubt that fintech will remain an incredibly investible sector.

Breakouts

Below are some attributes of the biggest winners in the 2009-2021 vintage.

- Inspiring missions. Is this a cheesy topic? Sure. Regardless, it's something I care about. Few examples:

- Coinbase: "To increase economic freedom in the world."

- TrueML: "To restore hope and financial stability for those who lost them."

- Stripe: "To increase the GDP of the internet." - Situations where there's a huge and growing market with a vulnerable incumbent (banks probably don't count given their resiliency). Perhaps this is one of the takeaways from the Adobe-Figma acquisition.

- Contrary to the previous bullet, talented founders building in unpopular, tiny, new markets where a big leap of faith is required regarding the future market growth among many other stars aligning. Think 2012 Coinbase, 2013 Circle.

- Thoughtful customer selection. Targeting an underserved audience isn't attractive without a breakthrough in approach or tech. For instance, it's more scary than exciting if an insurtech startup wants to provide tree service insurance in Florida when nobody else will without a significant innovation.

- Business-critical infrastructure. It's important to be needed instead of wanted. Think Mambu, Thought Machine, FIS, Global Payments, Hummingbird, Alloy, Bloom Credit, Sardine, Plaid and even the credit bureaus.

- Hairy, unsexy, hard, impactful problem solvers. Think Nova Credit and TrueML.

- Ambitions of comprehensive product suites. The harder a company makes a market map makers life, the better. Empires like Experian, Fiserv, PayPal, Coinbase, Intuit, FIS, Stripe, and Square ended up with many products on their way to breaking out. I'm open-minded to the path to getting there. Everyone has to go from 0-1 somehow. Most companies try to build one thing really well. They end up building some other things on their way in support of making their first product or broader value prop stronger. On the other hand, a company like Rippling is known for building as a "compound startup," which you can hear about on a recent 20VC episode. Both are viable paths. The first is easier. The second requires an experienced operator with masterful execution. Both can produce big winners.

- Founders who...

- are special. Cheesy but true. I have a bias toward people with deep domain expertise. But it would be a mistake to require it. Special people come from all backgrounds.

- treat compliance like a first class citizen. A great compliance culture and talent is a competitive advantage in many areas of fintech. - Founders who bet the farm on any of the following...

- new technology like advancements in faster payments systems, process automation, open banking, crypto, etc. The tech needs to alleviate severe pain points, produce massive efficiency gains, or open up brand-new design spaces.

- impactful regulatory changes. Financial services is one of the most regulated industries in existence. Many make a huge impact. Look at Dodd Frank as the obvious example. Here are some thoughts on a potential Durbin v2. Change is inevitable, which can create both headaches and opportunities.

- secular & cyclical economic shifts. This 2023 banking and capital markets report states that "the global economy is in a fragile and fractious state." We're coming out of a decade long soft cycle. Interest rates are up. Consumer credit card balances are up. The average monthly rent continue to go up every year. Public stocks have been going down since the end of last year. There was a lot of new company formation. Profit margins were good. NIM will likely go up, but non-interest income continues to decline so banks and insurance companies will focus on efficiency gains. The list goes on. The following 10 years could look very different than the last. Again, this will create both headaches and opportunities.

{kind=link}

So, what makes for a special fintech company?

I thought it would be fun to ask some industry experts what they think.

Amy Cheetham (Costanoa)

Building a company with the ability to create long lasting change in the financial services industry requires a combination of unique insights into a corner of the market that hasn't been disrupted effectively combined with a differentiated distribution strategy. It's rare to see real innovation and not just a slightly updated version of a previously created business model or strategy — when I see a truly distinct and novel idea combined with a strong team with deep industry expertise capable of navigating the complexities of the regulatory environment, that's when I get excited.

Sid Powell (Maple Finance)

A focus on doing something in a fundamentally different way. In the next 3 years, finance will change more than it has in the last 30. The fintechs which capitalize on this will be the ones that offer a fundamentally different way of doing things. The days where a fancy user interface on 50 year old banking systems could cut it are over.

Ohad Samet (TrueML)

A combination of a meaningful mission, differentiated distribution, and positive unit economics that improve over time and at scale with better technology. Companies like that attract talent and funding at critical junctions that allow them to survive 1-2 years of turmoil and gain market share when competitors are struggling.

Aaron Huang (Productfy)

A balance of idealistic optimism and grounded pragmatism in a founding team that manifests throughout its culture. These diametrically opposed angles happen either through sheer synchronicity, or from a specialist on either the supply (former banker) or demand side (technologist). This usually suits prior operators who have seen the guts of the engine or have prior expertise forging scalable bank / fintech partnerships - coupled with folks who can see where the customer is going to be 12-18 months out from today. In today's environment, I would add an acute ability to read regulatory sentiment in a market turning risk-off. All of these factors enable the highest probability of success when managing working capital and longer times to scalable revenue.

Jason Henrichs (Alloy Labs Alliance)

An over abundance and a growth at all costs mentality created many “unicorns” by valuations but little value. Breakouts of the future need to do more than smear a digital veneer on existing products. They must reinvent the way value is created and distributed.

Jon Coffey (Current)

The special ones have an ability to recognize the reasons why gaps in the market exist and what has to be true to fill those gaps. There are very few truly new ideas in finance, but there are new opportunities enabled by lower costs of servicing and changes in regulation. The standout companies marry both.

Dan Kahn (Plaid)

Solve real problems. Solve real problems. Solve real problems. There is so much duct tape in this industry that (mostly/sorta/kinda) works, but that also means there is still a ton of opportunity to re-imagine how things are done, delivering either cost savings or a better experience for consumers and small businesses.

Dan Mottice (Ansible Labs)

Customer stickiness is difficult to achieve and maintain - especially in web3 and crypto. At Ansible Labs, we strongly believe in the concept of “flight to quality” - users will accrue to the most painless and safe tools. Truly special FinTech/web3 companies can capitalize on this idea with a hyper-focus on constantly improving user experience. This will only get more difficult as more competition enters the space. You risk getting left behind if you don’t have an obsessive focus on improving ease-of-use.

Kevin Dahlstrom (Swell)

The best fintech companies don’t just make existing financial products better/faster/cheaper, they rethink them from first principles. Banking is a trillion dollar industry with outdated products, low customer satisfaction, and incumbents that resist change. We’re in the earliest stages of disruption, but a sea change is coming.

Alex Johnson (Fintech Takes)

Solving a money-adjacent problem rather than a money problem. Fintech is way too obsessed with outperforming banks in traditional financial product categories. The real value of fintech is turning financial services into software primitives and using those primitives to build new software products that solve money-adjacent problems. The TAM for solving money-adjacent problems is infinitely bigger than the TAM for solving money problems.

Ben Brown (Accenture)

Financial services is a difficult industry to innovate in because it's highly regulated and it's important - you are taking care of peoples' money, making lending decisions that enable peoples' dreams, and protecting people against catastrophic risks. The most effective fintech innovators appreciate this unique dynamic and are able to balance a clear focus on solving customer pain points, navigating regulatory compliance obligations, and building a profitable business that has resilience through economic cycles.

Charley Ma (Alloy)

I like fintech companies that are much more tech vs financial services and that usually means I'm more focused on infrastructure. I like to see some clear path towards being a true software business with a high potential for software margins + high growth/adoption. It then comes down to the founder(s) + team for me - some combination of grit, relentlessness, and vision is required to build in this space. There's a ton of legacy debt in regards to technology, regulation, large FI's, etc that it just takes a lot of time to compound a product and build something meaningful - no quick wins (generally speaking) in fintech infrastructure.

Samir Rao (Unit)

I think the magic happens when you've built a financial product or platform that not only changes how financial services can be offered but does so in ways that are actually sustained by core unit economics. Too many fintechs sell products unprofitably and then mistake usage for long-term adoption when in fact they only have users *because* it's cheap (and they depart as soon as the prices right-size). When you've built a product so good that people use it even when it's not cheap, and when they go out and become your biggest advocates and source of leads, that's when you've hit the jackpot.