Faster payments with FedNow

With the rise of stablecoins, several real-time payment systems live in the US, and the launch of FedNow nearing, I decided to spend some time getting up to speed with faster payment systems.

Faster payments

Defining faster payments

There are three main attributes for the definition of a Faster Payments System according to Faster Payments Council:

- Systems must enable immediate funds availability to the beneficiary.

- System must be available 24 x 7 x 365.

- System must allow for instant confirmation to sender and receiver.

Value & use cases

Financial supply chains (in the US) have innovated slower than actual supply chains. More times than not, it still takes a few days just to transfer money between your own accounts at different banks. You can often receive an order from Amazon faster than Amazon can receive your payment. Faster payments can improve the experience for various use cases, and should be able to spur new use cases that weren't possible.

Obvious examples:

- Faster issuance of loans to borrowers.

- Faster payments to employer-sponsored retirement plans.

- Faster real estate transactions given how many parties are involved.

- Faster disbursements of funds to customers during emergency situations.

- Faster payments to employees who earn commission or need expenses reimbursed.

This FedNow is almost here report states, "several industries have proved the value of real-time payments and will be early use cases for FedNow. These include payroll, utilities, telecom, and insurance. Use cases are also emerging within higher education and healthcare. It is becoming clear that the value of real-time payments is not use case dependent; it is desirable for all payments to be more efficient. Some FIs struggle to explain to clients the value of a real-time payment as a working capital tool. Allowing funds to be sent at a specific moment is valuable to small businesses whose cash flow dictates daily decisions, such as vendor payment timing."

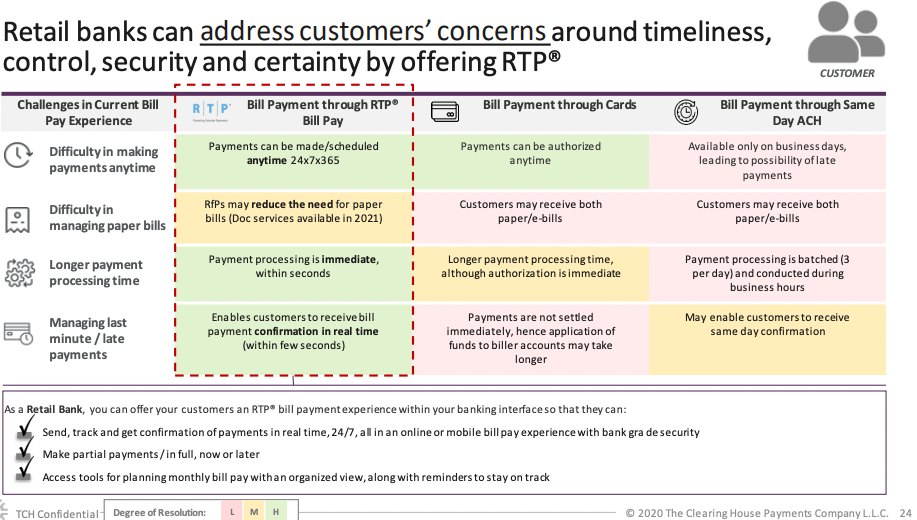

This bill pay experience at point of disruption report from The Clearing House highlights how real-time payments are "well positioned to resolve bill pay pain points." Today, more bills are paid via ACH than debit and credit cards combined. Customers expect payments to be processed immediately and billers are plagued with high costs of paper, inefficient reconciliation, and needs to maintain high cash reserves.

Offering faster payments will be a way to differentiate from competitors and attract customers to your services. But not everyone is necessarily incentivized to support faster payments. For instance, many business models reliant on revenue from float (banks, insurance, payroll service providers, etc.) may get stuck in an innovators dilemma.

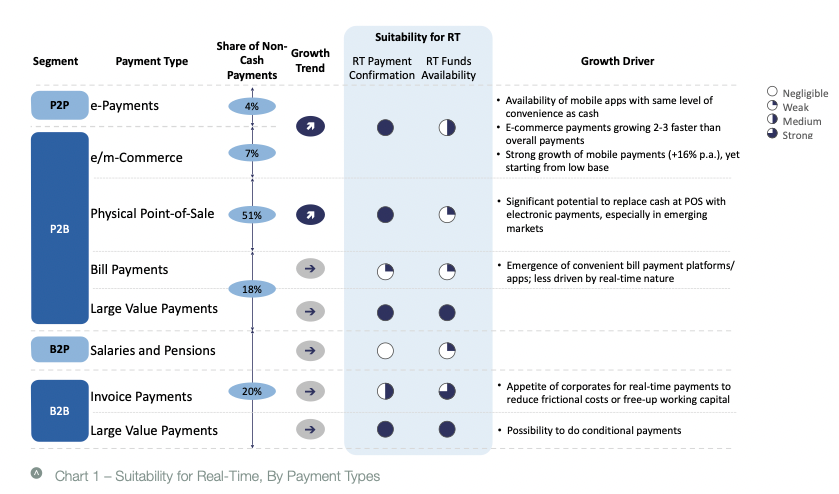

A survey in The Global Adoption of Real-Time Retail Payments Systems (RT-RPS) shows which use cases are more or less suitable for faster payments. For example, it found that large-value P2B (peer-to-biz) purchases like houses and cars, and large-value b2b payments are suitable for faster payments due to the value of immediate funding and immediate confirmation, which makes sense when I think about how I feel the few times I've needed to send money via wire.

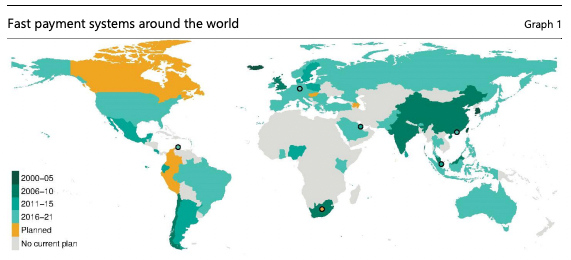

Adoption around the globe

Faster payment systems have existed for over 50 years, starting with Japan in the 1970s. The FIS global payments report states that 60 markets have real-time payment systems.

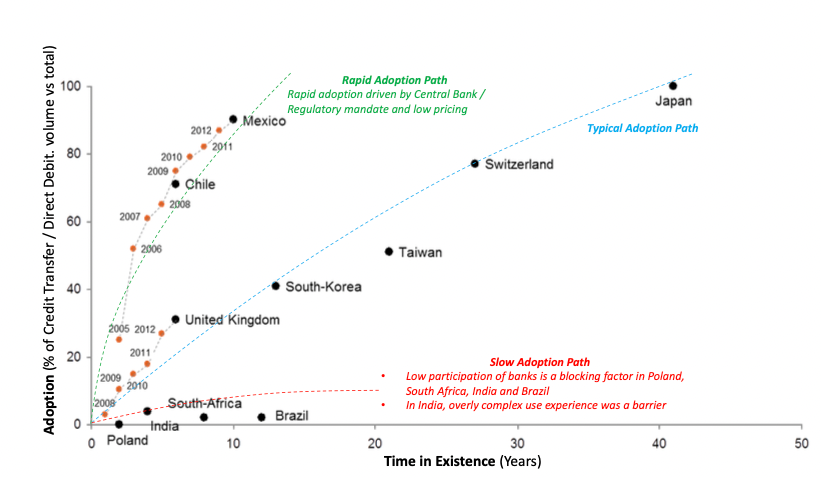

The payment systems launched more recently are actually the systems with the most rapid adoption. It also helps when countries and regulators play an active role. As an example, Mexico advertised the use of its system, SPEI to the public to help reduce the use of cash.

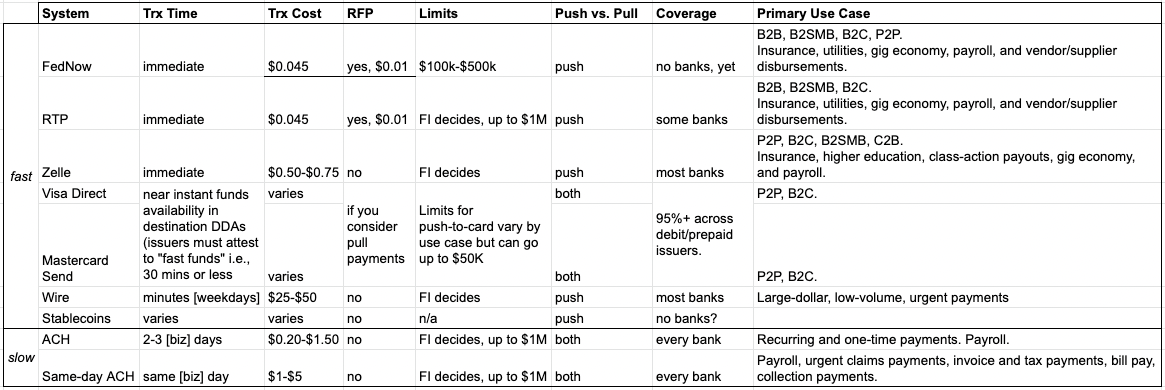

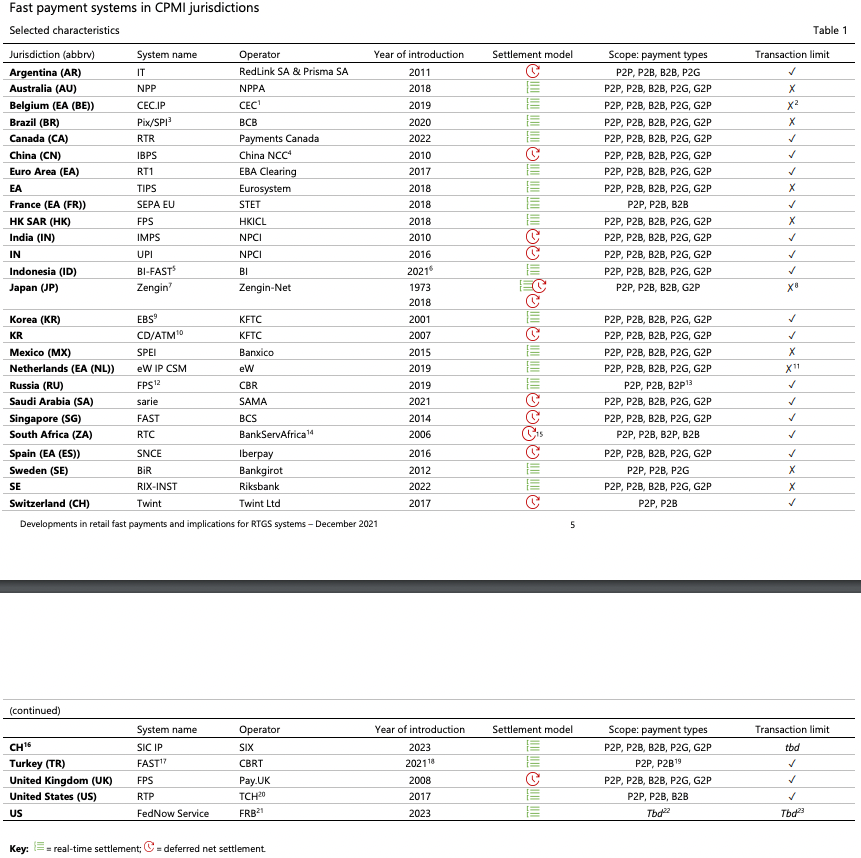

The US has a few real-time payment systems live right now. Here's a non-exhaustive list depending on how one could categorize these.

- RTP

- Zelle

- Visa Direct & Mastercard Send

And another called FedNow is supposed to launch in 2023. My curiosity has mostly been with the differences between RTP and FedNow, so that's where the rest of this post will focus. tl;dr, there aren't too many but FedNow is much cheaper.

RTP & FedNow

RTP and FedNow are both designed with the same attributes of faster payments in mind. They have many similarities but are completely separate rails. So, with that said, FedNow being the newest player on the block, will be contributing to payment system fragmentation. But there's good reason to believe it's better than RTP and will ultimately have much more adoption. The fragmentation bodes well for players like Modern Treasury who provide easy access to both systems through a single integration, while handling all of the communication behind the scenes for clients.

FedNow

- Expected to launch in 2023. Designed by the Federal Reserve.

- More than 110 organizations are participating in the pilot program.

- Will serve all federal banks through the FedLine network, providing payment and information services to over 10k FIs.

- Available to both individuals and businesses.

- Unlike ACH, but similar to RTP, FedNow only supports credit or 'push' payments. You can't 'pull' or debit another bank account. Therefore, it reduces risk because payments won't fail due to insufficient funds.

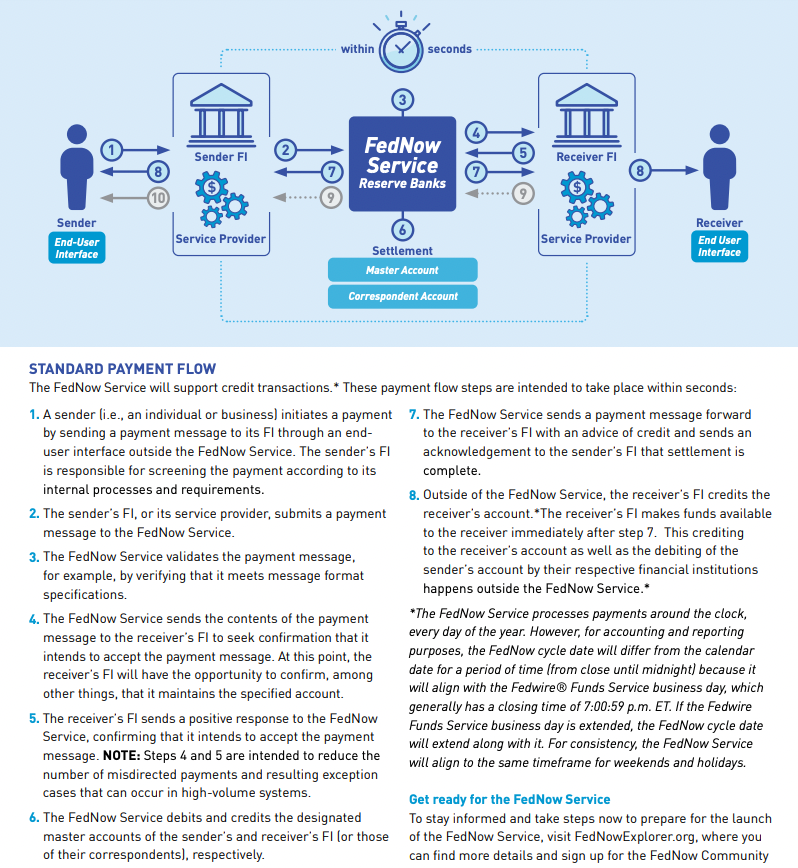

- Enables real-time payments for financial institutions of any size, in any community 24 x 7 x 365. Similar to wires, it's final when money leaves your account.

- Pricing. FedNow is mandated by the government to operate at break even. There's a $25 monthly FedNow service fee, $0.045 fee per credit transfer to be paid by its sender, and $0.01 fee for a request for payment (RFP) message to be paid by the requestor.

- Launching with RFP support. In the case of bill pay, this enables a business like a utilities provider to send a payment request for a bill due, that you can see via an alert on your phone, click a button to pay, and money leaves your account and settles instantly. The planned credit transfer transaction value limit will have a default limit of $100k, with the option to adjust down or up to $500k.

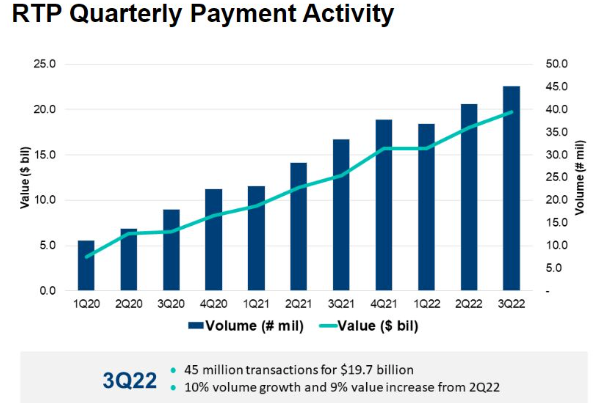

RTP

- Launched in 2017. Operated by The Clearing House.

- Created to address shortcomings of ACH and wires.

- Similar to FedNow, RTP only supports credit or 'push' payments.

- Initially launched with a $25k transaction limit but has increased to $1M over time.

- Pricing.

- Only available at ~25 select banks, but they cover ~60% of checking accounts given their size.

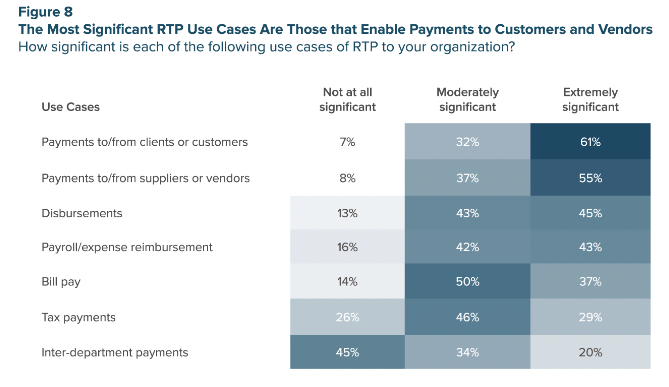

- According to this FIS/Worldpay Global Payments Report, "with a push toward more advanced business, corporate and government agency services, RTP supports real-time bill payments with just-in-time settlement, and instant government payout and collection capabilities. Many insurance and loan services utilize RTP for instant settlement, and same-day employee wages facilitate the growing gig economy."

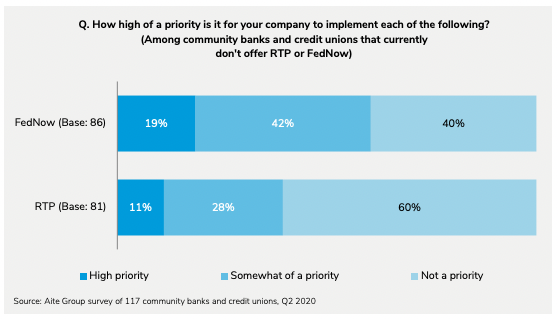

So, FedNow or RTP?

According to FedNow is Almost Here, implementing FedNow sounds like a higher priority than implementing RTP.

I asked Alex Johnson for his thoughts on the topic:

One thing that I think gets underestimated by folks in fintech is the degree to which adoption of RTP has been hampered by small banks’ distrust of big banks (who own the Clearing House). I think FedNow will see more adoption and faster adoption than you might otherwise expect because of small banks’ preference for it. Also, small banks tend to do more on the commercial side than the consumer side anyway and faster payments is much more beneficial to businesses than it is to consumers. It’s a bit like if the Fed had created a P2P network as an alternative to Zelle. If they had, I doubt as many community banks would have signed up with Zelle.

Info on others

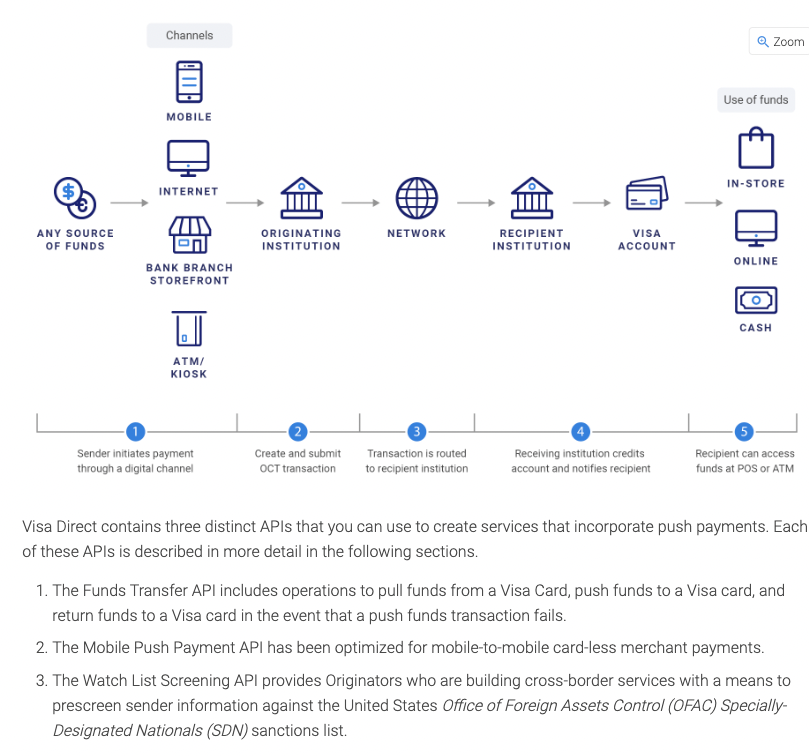

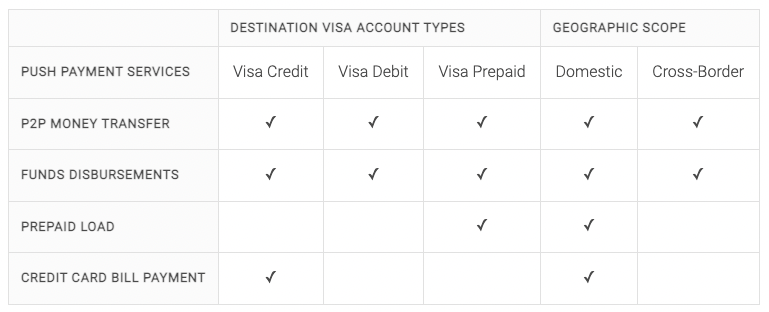

Visa Direct

- Enables individuals, businesses, and governments to send & receive, domestically and internationally, in near real-time (Visa docs say "actual funds availability varies by financial institution. Visa requires some issuers in some countries to make funds available to its cardholders within a maximum of 30 minutes of approving the transaction."

- Leverages the Visa network and debit cards to introduce pushing money from a bank account to another. Prior to Visa Direct, pulling was the primary method of money movement. There appear to be three API's to support various capabilities: Funds Transfer API, Mobile Push Payment API, and a Watch List Screening API.

- They tout it as being a great solution for p2p payments and for funds disbursements (delivery payments, tip disbursement, refunds, rebates, payouts, government distributions, etc.).

- A Nilson report shared, "issuers reported $89.38 billion in outflows with Visa Direct accounting for 91.5% of the total. Outflows are almost exclusively comprised of person-to-person funds transfers using third-party apps led by Square Cash, Apple Pay Cash and Facebook. Square Cash dominates those transactions. It is more than three times bigger than its nearest competitor. There were $66.49 billion inflows in 2020 with Visa Direct accounting for 89.1%. The top use cases for inflows are tied to P2P transactions from Square Cash and Venmo, from payments insurance companies make to claimants and from payments that companies such as Uber, Lyft, Instacart and DoorDash make to drivers. There are more outflows than inflows because most recipients choose to leave funds in their third-party app such as a Venmo account. Venmo is a business unit of PayPal. When a Venmo transaction flows from a consumer to a business, that payment will occur through PayPal, not Visa Direct or Mastercard Send. Currently, there are no consumer-to-business Visa Direct or Mastercard Send transactions in the U.S."

- I recommend trying to get in touch with my friend Gaurav Gollerkeri if you want to learn more.

Mastercard Send

- Pretty similar to Visa Direct. Like Visa Direct, funds can be transferred to most debit and prepaid cards in the US, typically within seconds.

- They tout it being ideal for domestic & cross-border p2p transfers, gig economy, insurance claims, and emergency disbursements.

- The Mastercard Send API supposedly works for domestic p2p and disbursement providers while the Remittance API is used by providers to enable cross-border payments according to these FAQ.

Zelle

- Launched in 2017.

- Created by Early Warning Services (EWS) which is basically many of the largest banks.

- Enables customers to send money to an email or phone linked to a recipients account.

- Mostly used to facilitate real-time P2P payments, even though Zelle actually clears and settles using older, slower rails.

- FIs usually set limits between $2,000 and $20,000 per transaction and/or week.

- Zelle's growth is pretty mind-blowing. It proves the value of distribution advantages in fintech. Nearly $1.5T from 5B transactions has moved across the network with 1,700 banks and credit unions offering the option to their customers. "Overall payments in Q2 2022 equated to $155 billion sent through the Zelle Network® on 554 million transactions. Year-over-year payment values increased by 29%, while payment volume increased by 27%."

Same-day ACH

- ACH usually takes 1-3 business days. An amendment was made in 2015 to speed them up to same-business day processing. It was introduced for credit payments in 2016 and debit payments in 2017.

- The limit per transaction increased from $25k to $100k in 2020, and from $100k to $1M in 2022.

- In Q2 of 2022, there were 185M same-day ACH payments transferring $486B, and increase of $24.% and 94.4% over the same quarter a year earlier.

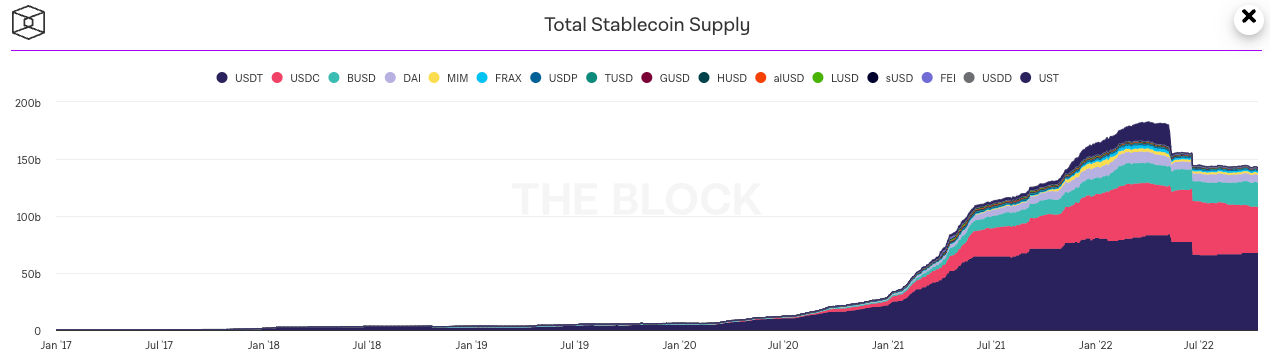

Stablecoin

- Stablecoins have been one of the bright spots of crypto during this bear market, proving to be an area of the market with real PMF.

I asked my friend Scott Alcorn for his brief thoughts on what it takes to handle fraud on faster payment systems:

The big challenge is truly building fraud risk controls at the network level. For example, Zelle is a closed loop where the sender and receiver must be signed up to participate. Doing analytics on both sides of a transaction is necessary to mitigate the "final" irrevocable nature of these transactions.

Conclusion

The US is trying to catch up to the rest of the world when it comes to faster payment systems. The five year old RTP system will likely see less adoption than FedNow after it launches next year. When it comes to fintech, distribution matters. The cheaper pricing with FedNow is a huge leg up over RTP.

But maybe there are more reasons why RTP isn’t more popular, signaling FedNow may not be either, be it a lack of demand and real need, misaligned incentives amongst key parties, or something else.

At the end of the day, increased competition between RTP, FedNow, Visa Direct, Mastercard Send, Zelle, Venmo, and stablecoins is great for consumers and businesses. We're likely to see a bigger shift in payments over the next ten years than we did over the last twenty.

Reach out if you want to school me or talk about potential product and startup ideas. Hit me on Twitter or LinkedIn.

Thanks to all of these fantastic sources:

- FedNow Service Product Sheet

- FedNow FAQ

- Faster Payments Council: What’s in a Faster Payment (or Faster Payments System for That Matter)?

- Swift Paper: The Global Adoption of Real-Time Retail Payments Systems (RT-RPS)

- FIS/Worldpay Global Payments Report for Financial Institutions and Merchants

- BIS report: Developments in retail fast payments and implications for RTGS systems

- Volante Report: FedNow is Almost Here

- Clearing House: Bill Pay Experience at a Point of Disruption

- Levvel 2021 RTP Market Insight Report

- Modern Treasury: What is RTP?

- Modern Treasury: What is FedNow

- Modern Treasury: How RTP Works: A look at ISO 20022

- TheClearingHouse: RTP Pricing

- Samir Rao Interspace: The instant payment method that every neobank wants to offer