Popular sponsor banks for fintech programs

When I helped build Blispay in 2015, we went 'direct,' integrating with TSYS and one of the Utah sponsor banks. Building a fintech program from scratch is an arduous process which is why these days, many companies choose to work with modern providers like Highnote, Lithic, Unit, or Treasury Prime. Regardless of whether you build direct or through a BaaS-like provider, there will be a [sponsor] bank behind your program.

Matt Janiga and Reggie Young conducted a master class on the subject recently (link below), so most of the credit for the content in this post goes to them. I also augmented with a few other sources.

- Selecting a Bank Partner podcast episode with Matt Janiga & Reggie Young

- Banks behind Fintechs post & tweet thread from Samir Rao

- Open Source BaaS, Banks, and Processors worksheet

- What it Actually Takes to Launch a Card Issuance Program on Your Own blog post from Highnote

- How to select a bank partner? from Aaron Frank / Notafintechco

Notes

Why fintechs partner with banks?

- Partnering with a bank allows a fintech to access a Fed Master Account which lets you access payment systems like Fedwire and ACH. Access is limited to banks for now. There’s some chatter about fintechs getting direct access eventually.

- In the US, only banks and bank-like entities like credit unions can be principal members of Visa and Mastercard. So you need to work with a bank partner to get a BIN to offer a debit, credit, or pre-paid card product.

Bank sponsorship history

- A handful of banks have been in the sponsorship market for a long time, like Webbank, Celtic, Bancorp, Metabank, and TAB. BillMeLater partnered with Webbank back in the early 2000s. The Utah Industrial banks were mostly lending focused.

- Others started entering like Cross River Bank, Evolve, and Sunrise. Cross River went beyond lending, offering a wider range of services. For instance, bank accounts and Visa/Mastercard push-to-debit. Customer Bank came and left.

- Following 2008, many community banks found themselves in a low interest rate environment. They needed to diversify away from interest income towards fee income. The Durbin amendment following the GFC also allowed smaller banks to enjoy higher interchange than larger banks, making them attractive for fintech startups launching bank accounts with debit products (wrote a bit about this in this post). Partnering with fintechs and BaaS startups was a way to do this. Sutton partnered with Marqeta and rode their growth. Others like Piermont, Blue Ridge, and Coastal got more active.

- Not all banks and charters are the same. Learn about the types and regulators in this report as well as some of the changing policy convos: An Analysis of Bank Charters and Selected Policy Issues.

Capabilities

- Not all Bank partners are the same. Actually, none are. They tend to focus on different offerings and obviously have different processes for working with customers.

-Lending vs. Payments

-Non-card Lending vs. Card

-For cards, Credit vs. Debit

-Payment Acceptance - Just because you partner with a bank doesn’t mean you get free rein to do anything you want. Banks get first priority on things that impact its charter like capitalization payment settlement risk (why banks take a 3-4 day reserve against your volume), consumer protections. Banks want to make sure the fintech program won’t cause compliance issues for the bank.

How to partner

- Decide on your needs. Card products? Lending? Debit? Need Durbin exempt pricing?

- Do an RFP with 5-10, 20 banks at once. If you have a bigger budget and are a more established company adding a fintech program, then go to Ben Brown at Accenture. I've known him since his First Annapolis days. As Matt says on the podcast, he and his team are excellent. They can run the RFP process for you and always get the right people at the right banks on the phone. They can also be a big help when figuring out pricing.

- Leverage experienced counsel for bank partnership contracts.

-Peter Luce at Ketsal. Great with credit and always current on the latest trends. Can handle negotiations with bank partners.

-Crystal Kaldjob at Morrison Foerster (mofo). She's great at negotiating credit sponsorships and is helpful with anything related to lending, like collections.

-Eli Rosenberg at Baird. He often resporesents banks and fintechs in the sponsorship market. - Hire people with a lot of experience evaluating, standing up, and running programs as a fintech company partnering with a sponsor bank. For instance, people like Tonya Flickinger, Matt Janiga, and Ben Brown who have done this many times.

Grouping sponsor banks

As Matt and Reggie highlight, tiering does not mean one bank is better than the other for any given program. This tiering is strictly an opinion regarding operational maturity.

Operationally mature banks:

1. Understand the key risks.

2. Can explain the business to the regulators.

3. Keep operating your program on an uninterrupted basis.

If working with an operationally immature bank, then your fintech company needs to be extremely mature. You just need to bring the maturity to the bank.

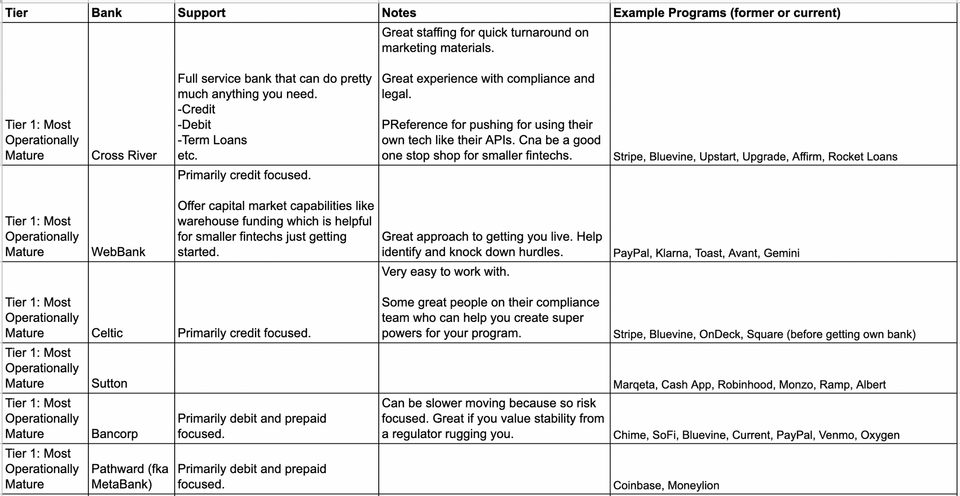

Most Operationally Mature

- Cross River Bank

Full service that can do pretty much anything you'd need with great staffing for quick turnaround on marketing materials.

Example programs: Stripe, Bluevine, Upstart, Upgrade, Affirm, Rocket Loans. - Webbank

Primarily credit focused with capital markets capabilities like warehouse funding.

Example programs: PayPal, Klarna, Toast, Avant, Gemini. - Celtic

Primarily credit focused with a great compliance team who is easy to work with.

Example programs: Stripe, Bluevine, OnDeck, Square (before getting own bank). - Sutton

Example programs: Marqeta, Cash App, Robinhood, Monzo, Ramp, Albert. - Bancorp

OG sponsor bank. Primarily debit and prepaid focused. Can be slower moving because so risk focused. Great if you value stability from a regulator rugging you.

Example programs: Chime, SoFi, Bluevine, Current, PayPal, Venmo, Oxygen. - Pathward (fka MetaBank)

Primarily debit and prepaid focused.

Example programs: Coinbase, Moneylion. - Sunrise

Example programs: AT&T debit, True Link, Gift Rocket, Orbis. - Evolve

Example programs: Mercury, Rho, Bond, Sila, Stripe Treasury, Synapse, Deserve, BlockFi, OnJuno, Dave. - Patriot

Generally not searching for sponsoring, mostly wanting fintechs to work with Lithic to get to them.

Example programs: Lithic, Privacy.

Moderately Operationally Mature

- Coastal

Example programs: Aspiration, Carta, Synctera, Aven. - Piermont

Example programs: Unit, Treasury Prime. - Blue Ridge

Example programs: Unit, Increase. - Green Dot

Example programs: Kabbage, Uber, Stash, Walmart, Intuit, - First Electronic

Example programs: Frys, Blispay, Cardless. - Stride

Example programs: Chime (credit), Lyft (driver), Lime, PayForward. - TAB

Example programs: Snap, EasyPay, Integra.

Operationally Immature

- Column