$11 Trillion

"Although most older Americans own some form of assets, the value of these assets is generally quite small. Equity in the home is usually the most important form of asset for the elderly; liquid or income-producing assets are generally very limited in amount... Consequently, many older Americans find themselves with little choice but to considerably reduce their standard of living after retirement." I pulled this excerpt from a 1981 Social Security bulletin post.

House rich, cash poor. Does this statement hold today?

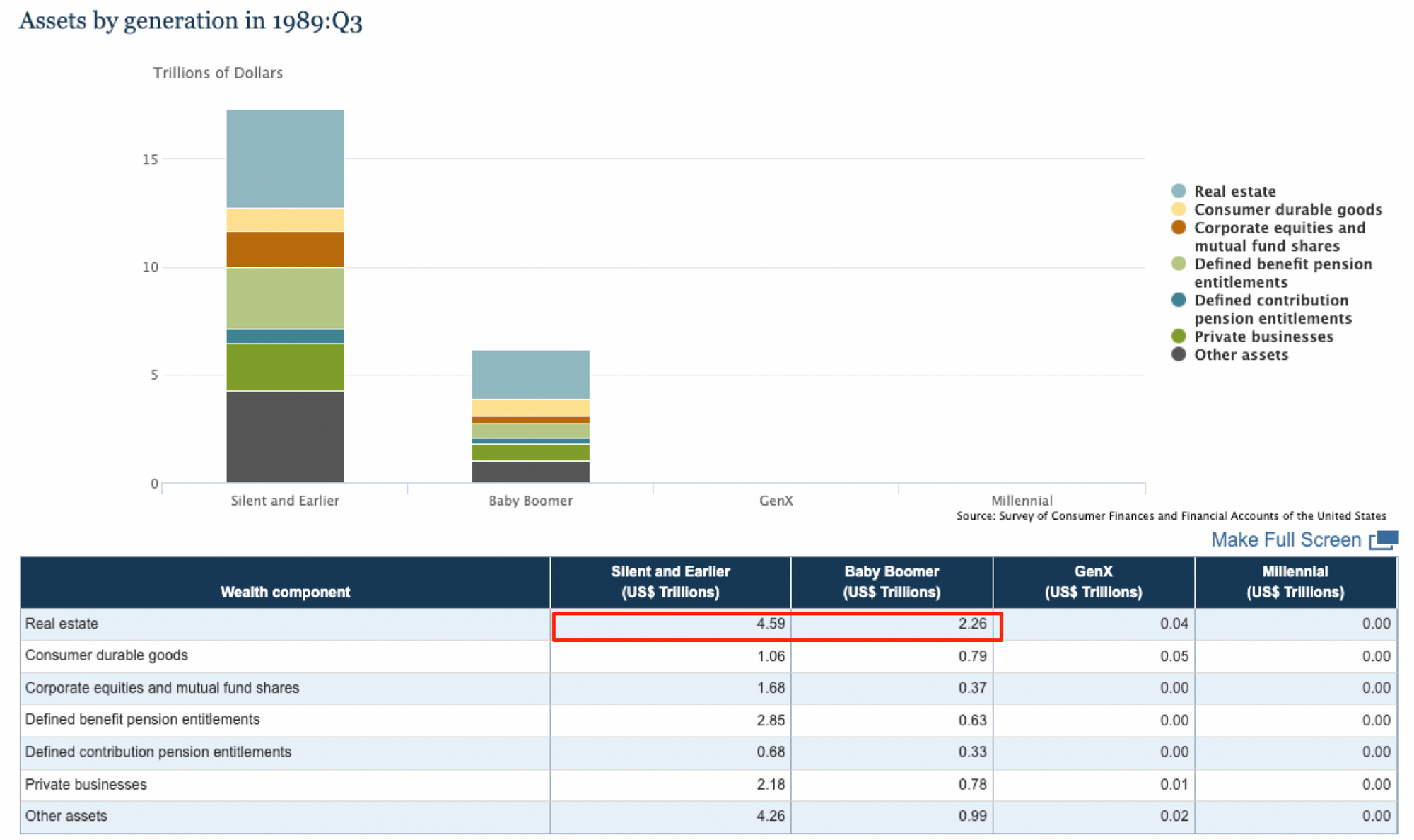

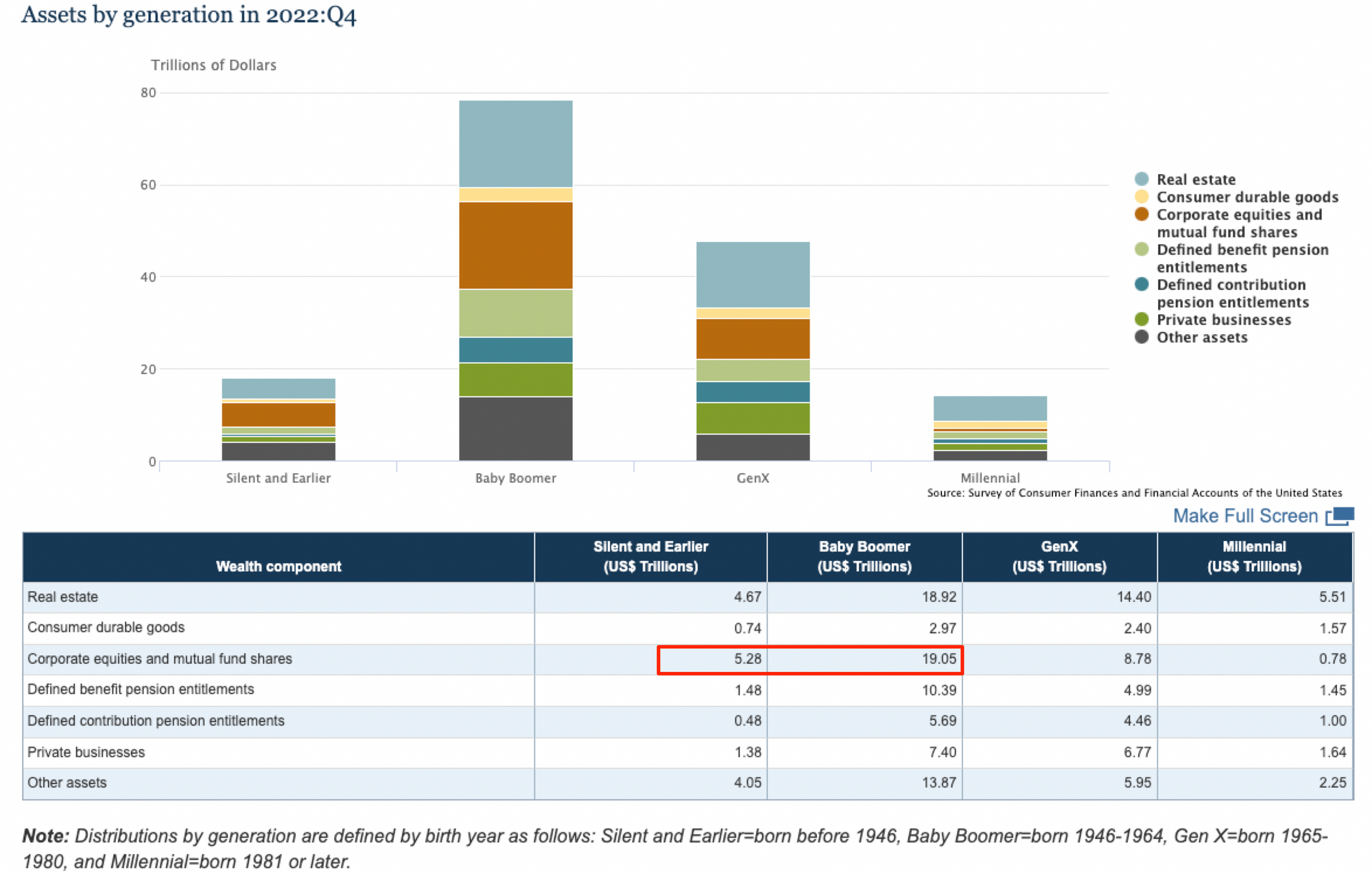

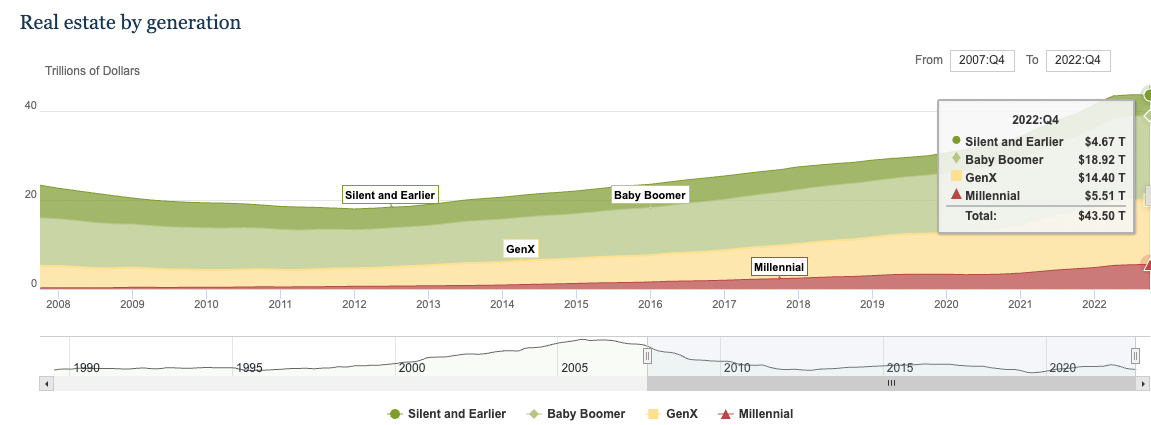

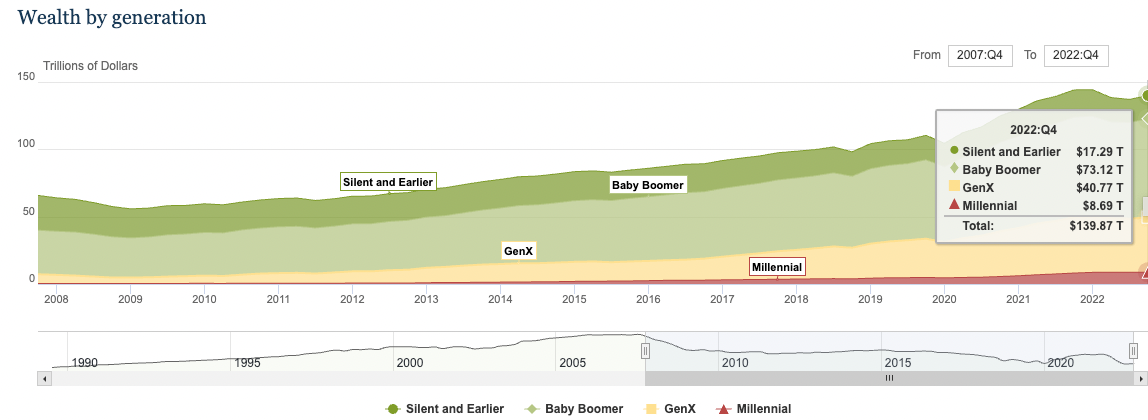

Here's a breakdown of assets by generation in 1989 (as far back as the Fed has) vs. 2022:

Well, times have changed. Real estate is a slightly smaller component of wealth today than stocks and bonds for seniors in the US. That said, real estate is still one of the largest assets across all generations.

Seniors hold the majority of real estate assets.

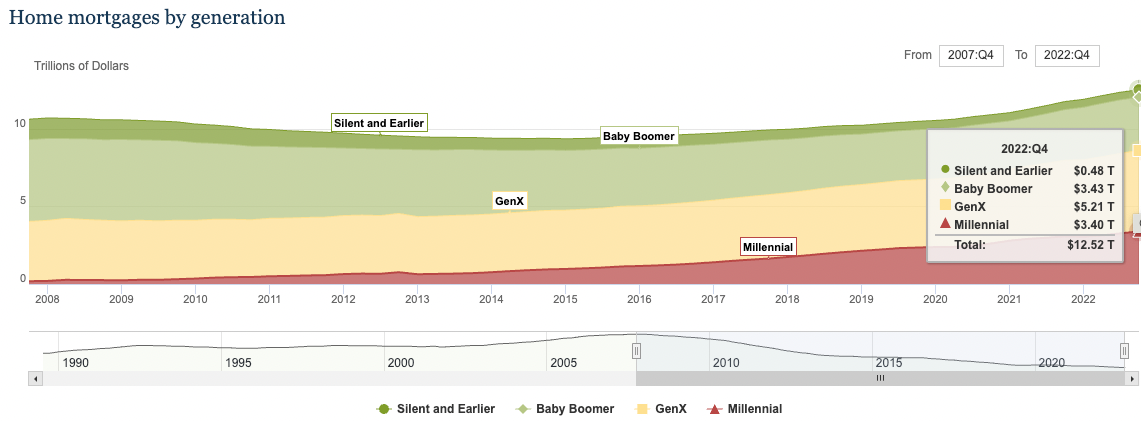

The majority of home mortgages are not.

This leads us to the demographic megatrends. The composition of our population is changing. The ‘silver tsunami’ was a term coined as a metaphor for the large baby boomer population reaching retirement age, outnumbering younger generations still in their productive years. The number of adults older than 65 will more than double to 1.6b by 2050, growing from 9.4% of the US to 16.5%. There were 11.7 working-age people for every person over 65 in 1950, but today there are 7, dropping to 4.4 by 2040. This dynamic creates unique threats to the healthcare system, housing market, workforce, and specific cohorts like older, low-income, and impoverished adults.

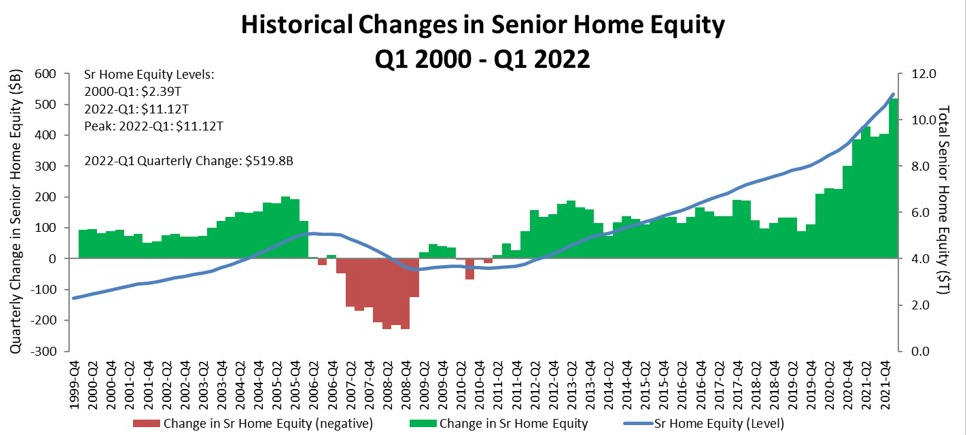

In 2022, senior home equity exceeded $11t for the first time.

For seniors, the equity built up in their homes often represents a significant portion of their net worth. And although tapping this equity becomes more important, the mechanisms to do so and the know-how is sorely lacking. Regarding personal finance, most people need to improve with accumulation strategies. I may not even pretend like anyone gives enough thought to distribution and spending strategies. I'm probably the only person who read Retire Secure in my 20s (nudge to others to read it, especially if you have parents over 50 who may need your help).

Like many have been or eventually will be my wife and I were abruptly thrown into this fire when her parents each got cancer. Intense care over 3 years and deaths 6 months apart from one another. Despite the data in the wealth component breakdown by generation, they didn't have significant investments. A reverse mortgage was an incredibly useful and important tool for them. This was my first exposure to reverse mortgages.

Reverse mortgages are not necessarily an attractive way to tap the only or largest asset a senior has as they age. However, they may be their only current option, if they quality. And like any financial instrument, they come with their own unique benefits, drawbacks, and intricacies.

Innovations in product construct and/or distribution that enable seniors or families of aging loved ones to tap their home equity are one of the largest opportunities in the shifting demographic megatrend. I'd love to talk with entrepreneurs exploring this space.

The rest of this post was a selfish endeavor to get up to speed on reverse mortgages. I figured I'd share for others interested in learning more.

Reverse Mortgages

Reverse mortgages are loans for seniors (62yo+), enabling them to convert a portion of their home equity into cash. Instead of making monthly payments to a lender, like a traditional mortgage, the lender makes payments to the homeowner. The loan is ultimately repaid when the homeowner leaves the house, usually upon sale or passing.

Costs

Reverse mortgages come with several costs. These can include:

- Mortgage Insurance Premiums (MIPs): Fee paid to the FHA for insuring the loan.

- Origination Fee: Fee paid to the lender for processing the loan.

- Appraisal Fee: Fee paid to the appraiser who determines the value of the home.

- Closing Costs: Fees paid at the closing of the loan and can include costs for a title search, title insurance, surveys, inspections, recording fees, mortgage taxes, credit checks, and other costs.

Types

Here are the most common types of reverse mortgages:

1. Home Equity Conversion Mortgages (HECMs)

The most common and widely available type of reverse mortgage. They're insured by the Federal Housing Administration (FHA) and are subject to regulatory oversight to protect borrowers. They allow homeowners to convert a portion of their home equity into cash.

HECMs offer several payout options, including a lump sum, a line of credit, monthly payments, or a combination of these. They also require potential borrowers to attend a consumer information session with an HUD-approved counselor before they can apply for the loan.

2. Proprietary Reverse Mortgages

Private loans backed by the companies that develop them. Unlike HECMs, they aren't federally insured. These 'jumbo' reverse mortgages are designed for high-value homes and may allow access to more substantial loan proceeds than HECMs because they're not subject to the same FHA lending limits. However, they might come with higher costs and fewer consumer protections than HECMs.

3. Single-Purpose Reverse Mortgages

The least expensive option and are offered by some state and local government agencies and nonprofit organizations. These loans can only be used for one specific purpose, which the lender will typically specify. That could be anything from home improvements to property taxes. While they may not offer as much flexibility as other types, single-purpose reverse mortgages can be helpful for seniors who need cash for a specific reason.

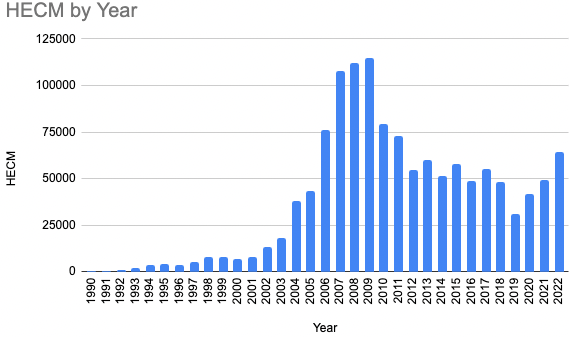

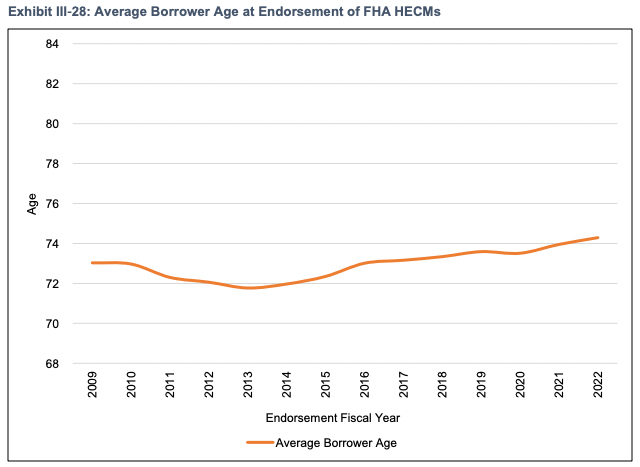

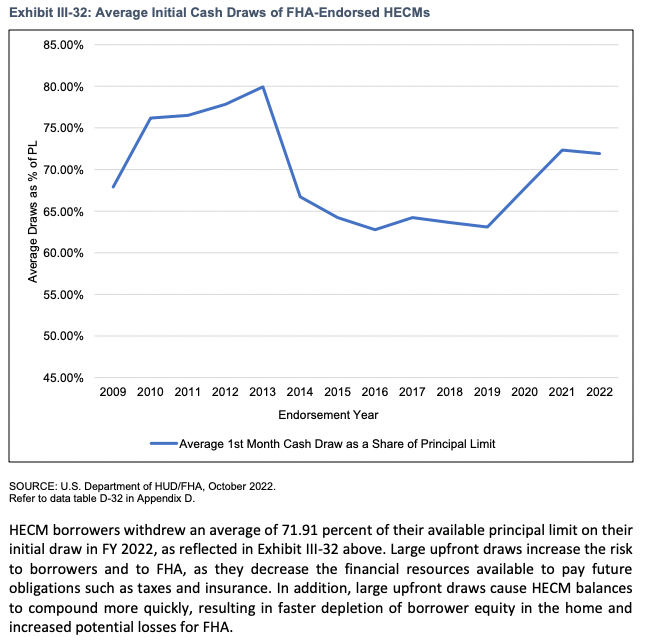

FHA HECM Data

Reverse mortgages are still a niche product. Less than 1% of eligible homeowners have taken up the product.

Limitations, Qualifications, Caveats

Devil is the details, so I don't want to confidently say everything below is valid for all lenders across the 3 types of reverse mortgages. I'm pretty sure most are true for HECMs and that specifics for Propriety and Single-Purpose are a bit different.

- Age: The youngest borrower on the title must be at least 62 years old.

- Primary Residence: The home you're borrowing against must be your primary residence. You must live in your home for more than half of the year.

- Equity: You must own your home outright or have a low mortgage balance that can be paid off with the reverse mortgage. Generally, the more equity you have in your home, the more you can borrow.

- Financial Ability: You should be able to cover ongoing costs associated with the home, such as taxes, insurance, and maintenance expenses.

- Mandatory Counseling: You must participate in a consumer information session with an HUD-approved counselor.

- Loan Limits: The amount you can borrow with a reverse mortgage is limited. You can usually receive 40-60% of your home's appraised value and the older you are, the more you can receive. The limit is determined by a variety of factors, including the borrower's age, current interest rates, the appraised value of the home, and the FHA's mortgage limits. As of 2023, the maximum limit was $1,089,300, but this number may change. I don't think the FHA spending limits apply to Proprietary Reverse Mortgages.

- Upfront Costs: Reverse mortgages can come with high upfront costs. These can include origination fees, closing costs, and mortgage insurance premiums.

- Interest and Fees Accumulation: The interest and fees on a reverse mortgage are added to the loan balance over time, which means the amount you owe can grow.

- Impact on Government Assistance: Because the funds received from a reverse mortgage are considered loan proceeds and not income, they generally won't affect Social Security or Medicare benefits. However, they could affect Medicaid or Supplemental Security Income (SSI) eligibility.

- Equity Reduction: A reverse mortgage reduces the equity in your home. Over time, as interest and fees accumulate and add to the loan balance, your equity decreases.

- Non-Borrowing Spouse Risks: If a spouse isn't listed as a borrower, they may not be able to keep living in the home after the borrowing spouse passes away or moves out of the home permanently.

- Heirs' Inheritance: A reverse mortgage must be repaid when the last borrower dies. This can impact the amount of inheritance left for heirs, as the loan balance, which includes the amount borrowed plus interest and fees, must be repaid.

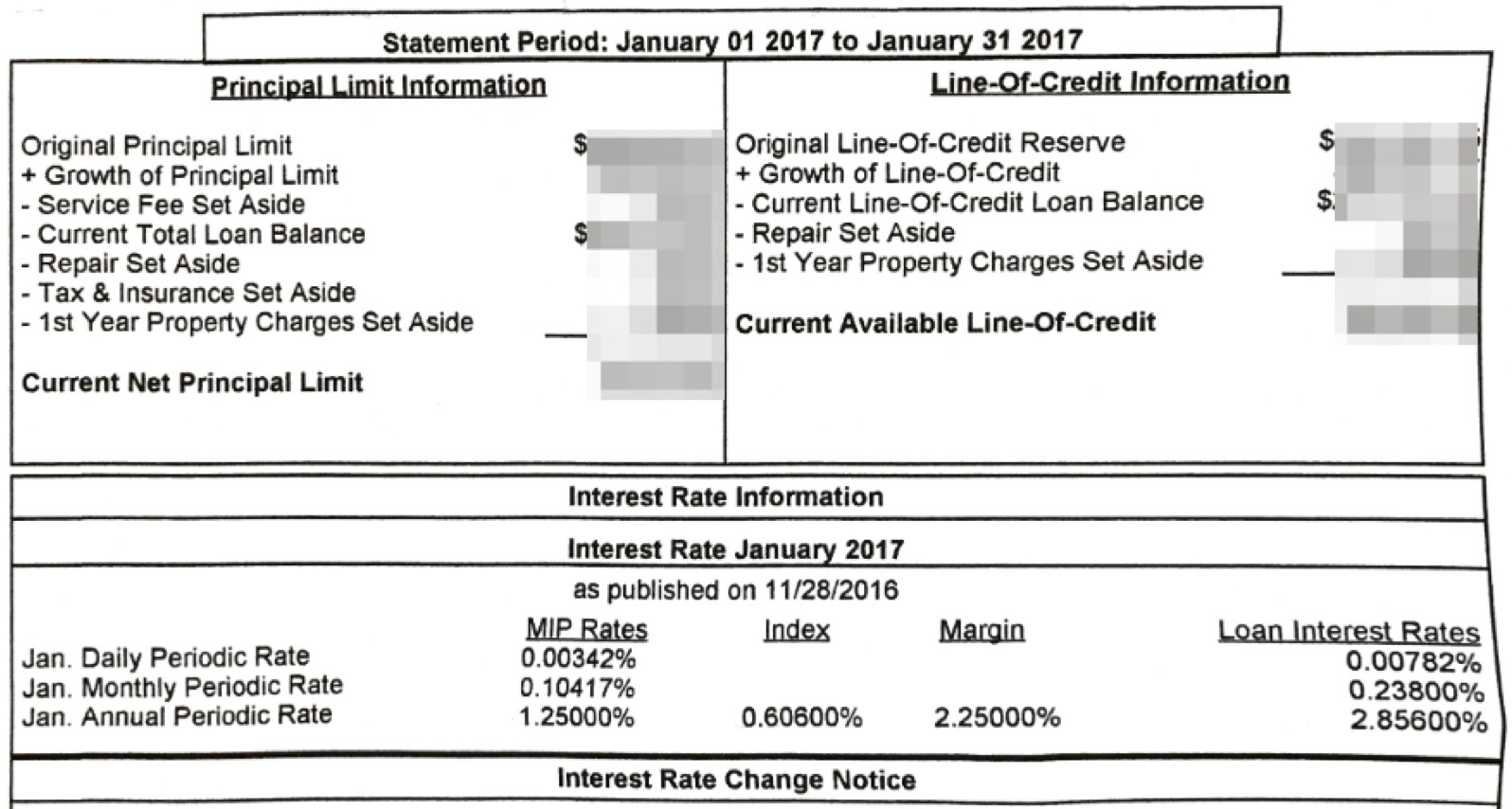

Expanding on the FHA imposed limitations, the FHA manages its HECM risk exposure in two primary ways:

- Defining the Principal Limit Factor that limits the percentage of the initial available equity that a HECM borrower can draw. Conceptually, the Principal Limit Factor is similar to the LTV ratio applied to a traditional forward mortgage.

- Limiting the Maximum Claim Amount, which defines the greatest HECM insurance claim a lender can receive. The Maximum Claim Amount is determined at origination and does not change over the life of the mortgage.

Cases to Use Reverse Mortgages

Reverse mortgages might be most beneficial for homeowners who plan to stay in their homes during retirement, have significant equity in their homes, and need supplemental income. A reverse mortgage can provide substantial financial relief for a homeowner living in a $300k home with no plans to move. This is the situation I found my in-laws in.

They're less suitable for those who don't plan to stay in their home for a while, want to leave their home as an inheritance, or can meet their financial needs through other means.

In short, a reverse mortgage can provide some financial relief to those who qualify in cases with few other viable options.

Low Take-up Rate

Less than 1% of eligible homeowners have taken up the product. Likely reasons:

- Desire to leave an inheritance.

- High upfront spending including the initial MIP, origination fee, and 3rd party charges. Combined upfront costs are high with fees exceeding those for alternatives like HELOCs.

- Mobility risk and long-term care. Reverse mortgages can make more sense in the case that you receive in-home care, a luxury not available to all.

- Moral hazard and adverse selection. Some homeowners don't keep up their home once their loan balance exceeds market value, or pay bills like taxes. But lenders may not evict homeowners due to repetitional risks and adverse publicity – headlines about evicting elders.

- Complexity, perceived and actual.

- Perception that a house should be a store of value rather than a source of retirement income.

- Fraud and misunderstanding leading to negative sentiment. As they're targeted toward older consumers, there's discrimination, uninformed decision making, misleading advertising, and discriminatory practices.

- Foreclosure risk as homeowners fail to pay property charges. Headlines alone have contributed heavily to a widespread distrust of reverse mortgages.

Legal Landscape

We're talking about a financial product here...

At the federal level, reverse mortgages, particularly Home Equity Conversion Mortgages (HECMs), are regulated by the Department of Housing and Urban Development (HUD) and insured by the Federal Housing Administration (FHA).

HUD has established rules and regulations to protect borrowers.

- Mandatory Counseling: The FHA requires potential HECM borrowers to meet with an HUD-approved counselor who can explain the costs, financial implications, and alternatives to a reverse mortgage.

- Cap on Loan Amount: FHA sets a limit on how much money a homeowner can borrow, which is a portion of the home's value, the homeowner's age, and current interest rates.

- Non-Recourse Loans: All HECMs are non-recourse loans. This means that the homeowner or their heirs will never owe more than the home is worth when the loan becomes due.

- Spousal Protections: Spouses of borrowers, even if not named on the loan, can stay in the home even after the borrowing spouse dies or moves out, provided certain conditions are met.

Many states also have their own laws and regulations that provide even more consumer protections.

- Cooling-Off Periods: Some states have "cooling-off" or "right of rescission" periods that allow borrowers to cancel the loan without penalty for a short period after closing.

- Counseling Requirements: Some states require additional counseling or have stricter regulations for counseling.

- Loan Terms and Conditions: States may have rules around the terms and conditions of reverse mortgages, such as interest rates, fees, and disclosures.

The CFPB, a federal agency, plays a significant role in protecting consumers in the reverse mortgage market. They enforce federal laws related to reverse mortgages, supervise companies that provide them, and educate consumers about them. They also collect and investigate consumer complaints about reverse mortgages.

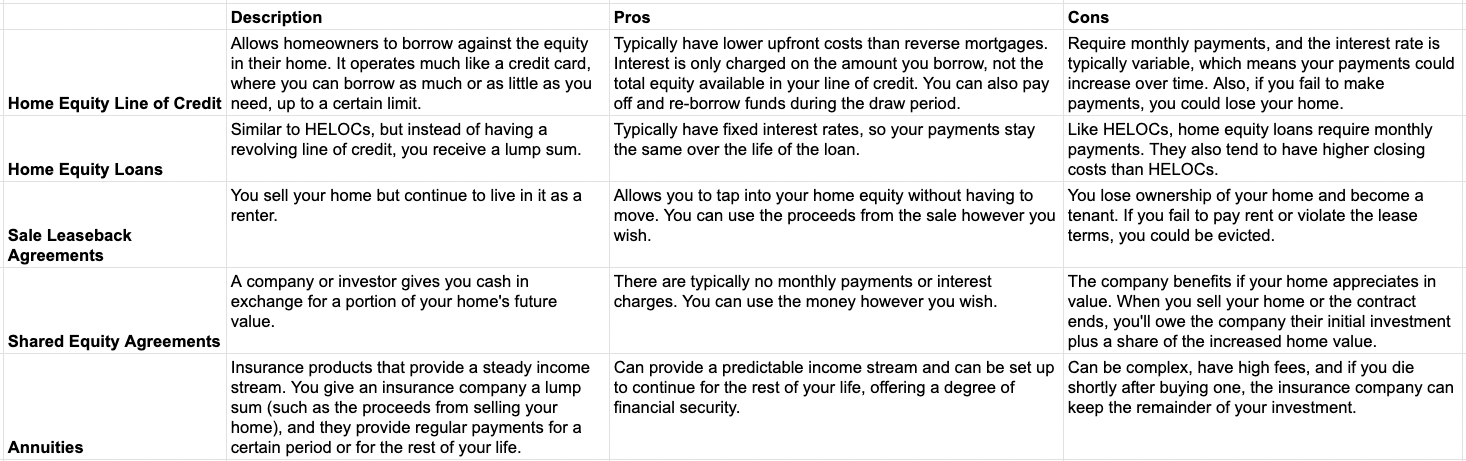

Alternatives

While they're alternatives, they're not necessarily great ones.

Conclusion

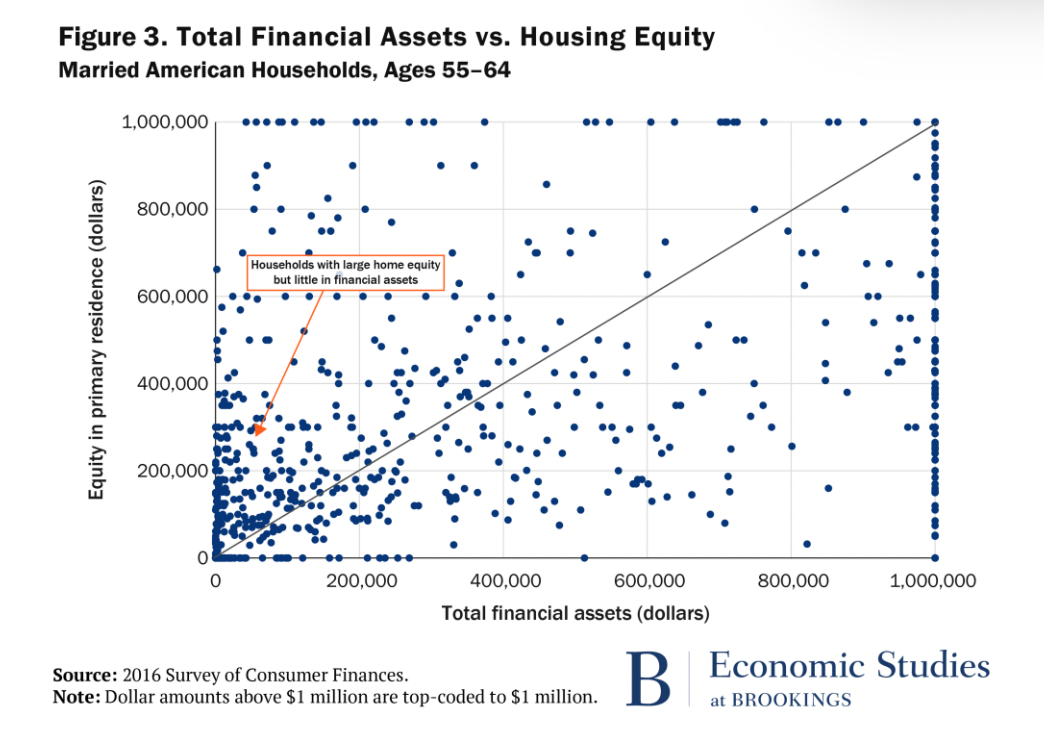

Many people have little financial wealth relative to their home equity.

Reverse mortgages can be a lifeline for some homeowners. But their theoretical appeal has yet to translate to mass adoption. Shortcomings suppress both supply and demand. Policy reform could address many of these shortcomings. For instance, reforms to mitigate foreclosure risk likely boost supply and demand and lower costs. Regardless, it's apparent that innovations in product construct and/or distribution that enable seniors or families of aging loved ones to tap their home equity are among the most interesting opportunities in the shifting demographic megatrend. I'd love to talk with entrepreneurs exploring this space.

Further reading

- CFPB reverse mortgages

- CFPB 2021 mortgage market activity and trends

- FHA 2022 annual report regarding the FHA mutual mortgage insurance fund

- Brookings Economic Study 2019 unfulfilled promise of reverse mortgages

- Senior home equity exceeds record $11.2 trillion

- Fed: distributional financial accounts

- Fed: distributional financial accounts by generation comparison

- SSA Assets of the elderly as they retire

- Reverse mortgage faq

- 2023 reverse mortgage lending limits

- NOLO reverse mortgage restrictions and requirements

- Investopedia reverse mortgage pros and cons

- Experian reverse mortgage downsides

- Bankrate reverse mortgage pros and cons

- Retire secure