Personal Finance… a thread.

Crossposting my long Twitter Thread of Personal Finance tips, tricks, and resources:

2/ I’m going to share short and concise opinions each day and see how long I can go on for. Note that personal finance is highly… personal. Not everything is advisable and applicable to everyone.

3/ Keep your personal burn low.

Budgeting is important (and it’s actually easy). @PersonalCapital is the new @mint. Open an account and use their free service. Tracking income and spend is the first step to developing a budget and lowering expenses.

4/ These 9 themes influence every aspect of personal finance (and business, relationships, life, etc.):

* Simplicity

* Cycles

* Expertise

* Time

* Diversification

* Judgement

* [Low] Fee’s

* Risk Management

* Unfairness

5/ Investment portfolios are heavily influenced by cycles.

Everything around us including ourselves are in a cycle of some sort. Learning to recognize & embrace cycles in investing and life is both 👁 opening & liberating.

This 📖 is a great primer: The Little Book of Stock Market Cycles

6/ Lean on Bogleheads.

The single most impactful actionable advice I can give to anyone is to spend as much time on bogleheads.org as you do on Facebook. Your life will be altered for the better, even though you may not realize it for 10yrs.

7/ I’m not advocating for die-hard Bogleheadism; Im advocating for perusing the forum & seeing how far down the rabbit hole you go. Altho Ive been heavily influenced by Boglehead philosophies, I’m more practical & open minded than those who confuse low risk/costs for deprivation.

8/ “There’s no such thing as a free lunch.” Bullshit. There’s actually free lunch & free trips. We’ve been to Greece, Vegas, Florida, Colorado… for free. It’s called Credit Card sign up spend bonuses. They’re awesome and well worth it. Check out @thepointsguy & @Drofcredit.

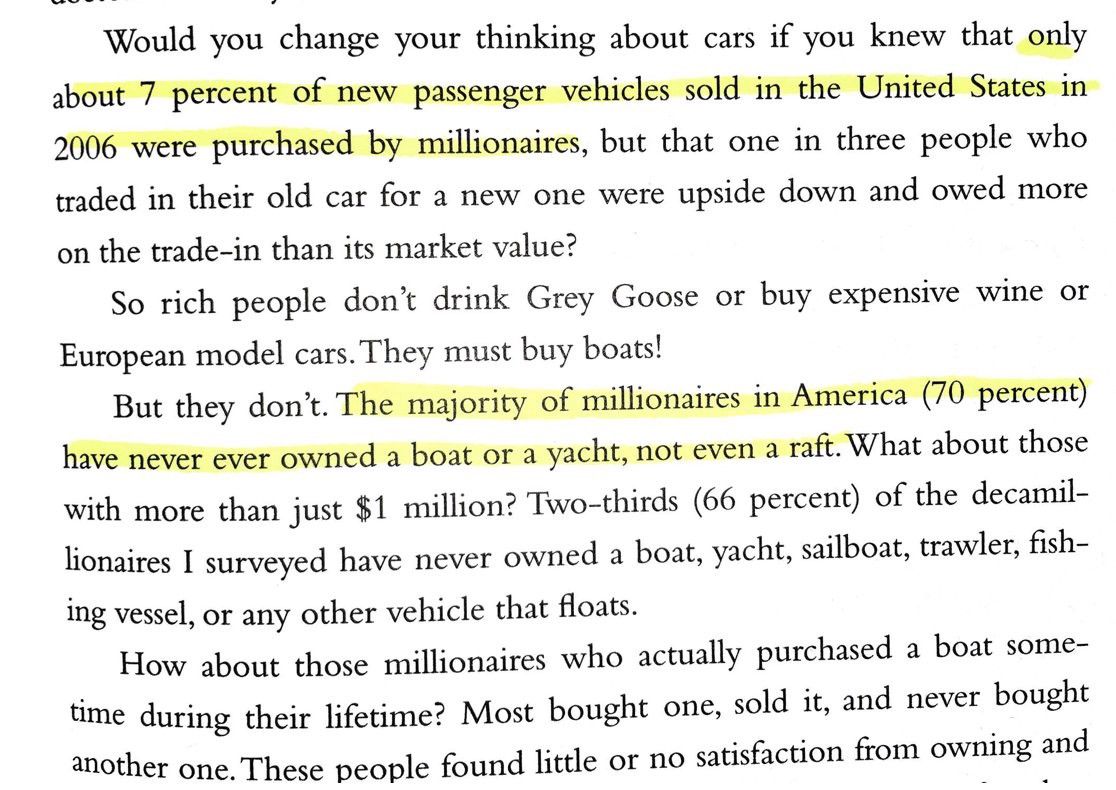

9/ I bought a used 2014 Honda Accord 🚘 in 2017 from @CarMax. It’s perfectly sufficient and will be much cheaper to maintain over the years than a sexier BMW, Audi, Mercedes… Also, CarMax really is on the path towards being the way car buying should be. Simple, in, and out.

10/ PSA: U dont need to buy a 🏡 .

Renting isnt ‘throwing away money’ & it actually has many advantages (financial & otherwise) over owning. Homes aren’t good financial investments historically. Renting is Throwing Money Away … Right?

11/ Buying a 🏠 for the right reasons can make sense.

1. Plan to own it for 10+yrs

2. Strongly desire the lifestyle (especially understandable if u have a family)

3. Acknowledgement that u may not make money off it

Its hard for me to be concise when it comes to homeownership 😥

12/ Buying a property outright is owning it. That could be a good investment. But since when is borrowing hundreds of thousands of $$ from a bank & using it to buy something considered an investment?

Have u thought about the opportunity cost of the down payment?

Moving on!

13/ “If your plan is clear, it will be easier for you to stay on plan” — Charles Ellis. This quote has really influenced how I invest and how I build at work.

For investing, this means to buy & hold low cost broad market index funds primarily. The Elements of Investing: Easy Lessons for Every Investor

14/ He’s basically saying to avoid load funds, expensive mutual funds, & speculation in the form of individual stock picking. Overwhelmed? Well priced Target Date Retirement Funds are great also. See if your 401k offers these from a firm like Vanguard.

Simple, cheap, and clear!

15/ Re: Speculation.

The majority of my portfolio is in diversified cheap ETFs and index funds. But we live once & speculation is fun, so I’ve decided the risk/reward is there with small amounts. I’ve done really well with $FB ($23) and $SQ ($9). I’m more of a knife catcher.

16/ Speculation cont’d: I feel very disadvantaged w/ public stock picking so have never bought more than 1–2 in a given yr.

Now seems like the right time to intro crypto. Yes, Ive been stuck in the rabbit hole.

Buy some $btc or at least learn about it from Saifedean: The Bitcoin Standard: The Decentralized Alternative to Central Banking

17/ You’re not going to nail market timing. I struggle as much as the next guy with this..

Remember, cycles.. Things will take a turn down, but when? Im more on the sidelines now than the past 3yrs, which may be a bad decision. We’ll see.

Timely thread:

18/ Dollar Cost Averaging (DCA).

Struggling w market timing? DCA in or out. If you dont know what this means but are contributing to an account like a 401k every paycheck then don’t worry… you’re averaging in.

19/ Time… solves a lot of problems in life. Its also 1 of the biggest factors in investment returns. Time in the market can make up for years of poor market conditions.

Long time horizon w/ a windfall? May be better off not DCA if u can stomach it: Investing a Lump Sum at All-Time Highs

20/ Are u or a family member on a high income medical professional path? Med student, resident, dentist, doctor…? You’re in a unique position. High income (eventually) but super high debt.

The earlier you discover @WCInvestor, the better.

Buy this 📕: The White Coat Investor: A Doctor’s Guide To Personal Finance And Investing

21/ Follow strategist @RyanDetrick from @LPL for insightful, thought-provoking market updates. He frequently shares interesting trends and patterns. You shouldn’t use this info to try to time the market, but you also shouldn’t be ignorant to cycles.

22/ One of my favorite beginner investment planning books is by @awealthofcs of @RitholtzWealth.

He hosts a dope podcast focused on current financial events w @michaelbatnick called Animal Spirits. Shoutout to @ritholtz while we’re at.

Buy the 📖: A Wealth of Common Sense: Why Simplicity Trumps Complexity in Any Investment Plan (Bloomberg)

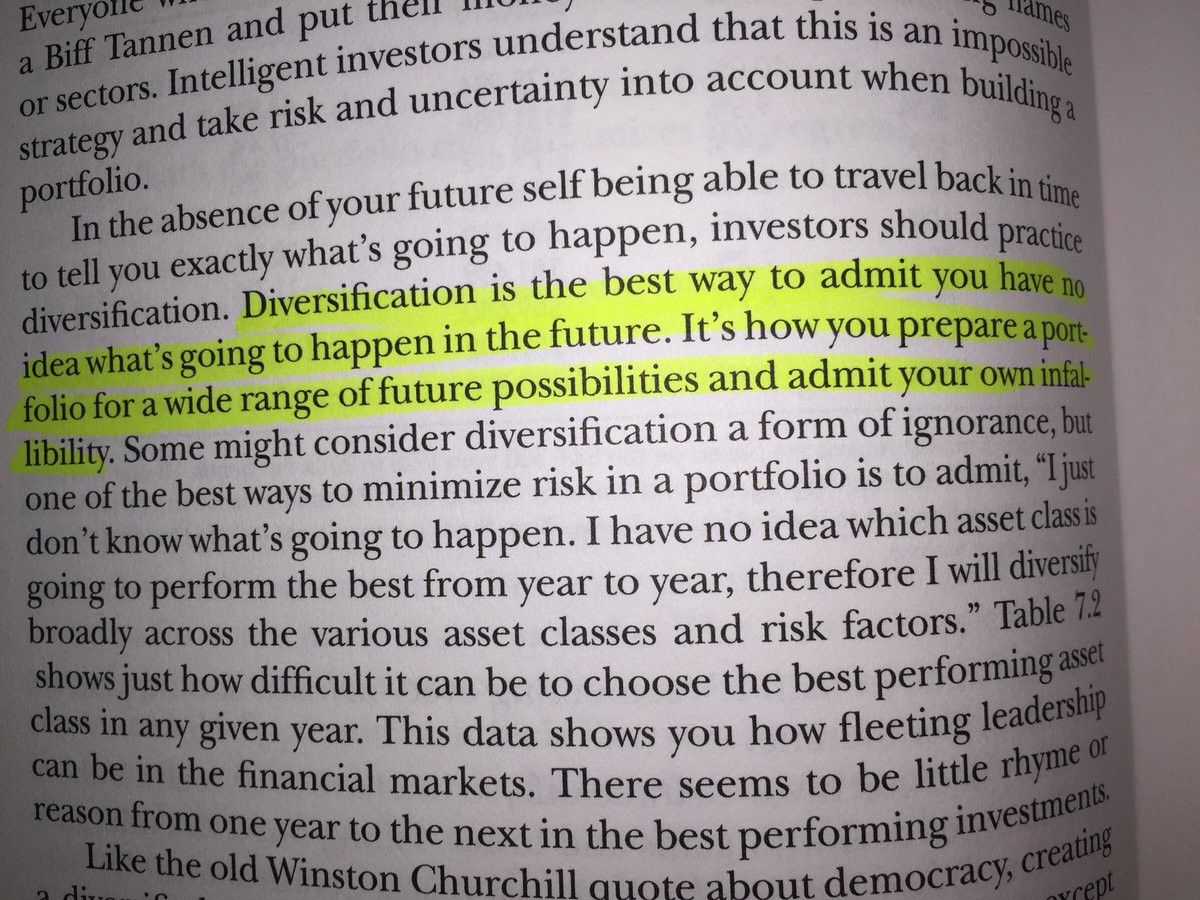

23/ How do I sleep at night? Exercise, 🐶x2, melatonin, and Diversification.

Diversification is key. Diversify investments across industries, geographies, etc. Diversify income streams. Diversify hobbies.

Diversity lowers risk.

From @awealthofcs:

24/ Diversification deserves 10 tweets but I cut homeownership off after a few so I’ll do the same here.

The chart on this @Wealthfront blog post shows why you diversify & why u shouldn’t chase returns. The Benefits of Diversification – Blog – Wealthfront

25/ When talking about Diversification & @Wealthfront, u have to talk about Burton Malkiel (their chief investment advisor). He wrote one of the best investing books of all time.

“‘The Get Rich Slowly but Surely’ strategy. “

Buy the 📖: A Random Walk Down Wall Street: The Time-Tested Strategy for Successful Investing

26/ Time to touch on Robo advisors 🤖.

We have accounts w both @Wealthfront & @Betterment. As previously stated, time in the market is hugely important. If you’re young & on the sidelines due to decision paralysis w how/where to invest, just choose 1 of them. You’ll be fine. Wealthfront | Betterment

27/ @Betterment’s Director of Behavioral Finance and Investments @daniel_egan is a must follow.

Since we just touched on Diversification… he puts out 🔥 posts like: Portfolio Diversification: Winning the War by Losing Battles

28/ It’s healthy to be humbled & made aware of how much of a disadvantaged u r compared to really smart people. @CathieDWood of @ARKInvest is 1 of those 👩💼 who u listen to & are reminded to KISS & just index.

Listen to her on @patrick_oshag podcast: Cathie Wood – Investing in Innovation – [Invest Like the Best, EP.97]

29/ @ARKInvest puts out some interesting white papers and emails a daily newsletter.

U may be interested in following some members of @CathieDWood’s team at @ARKInvest.

@yassineARK, @wintonARK and @jwangARK Innovation White Papers | Original Research on Innovation

30/ Life insurance ✅

Bad shit happen to good ppl. Lifes unfair. Fuck cancer.

I have a 10 yr term policy w option to extend later thru @NewYorkLife.

Fortunate to be healthy enough to qualify? Married or have kids & make 🍞? Stop delaying; it’s simple.

31/ Don’t veer from simplicity. Opt for Term Life Insurance instead of Whole Life, Universal, Variable, an Annuity, etc. Don’t mix investing with insurance 🚫.

Complex, hard to understand products are not better. Similarly, more expensive doesn’t always mean better either.

32/ Crypto Twitter (CT) is a dirty, dirty place. Don’t trust anyone.

@AriDavidPaul of BlockTower Capital is 1 of the good guys.

Get to know him & the current state of the universe regarding token projects on @WhatBitcoinDid: WBD 031 – Interview with Ari Paul

33/ Understand basic Operational Security (OpSec). Dont need to be full-on paranoid, altho its not the worst idea in the world.

VPN, PW Manager, @protonmail > Gmail..

Great guide by @tayvano_ for businesses & most lessons can be applied to personal life: MyCrypto’s Security Guide For Dummies And Smart People Too

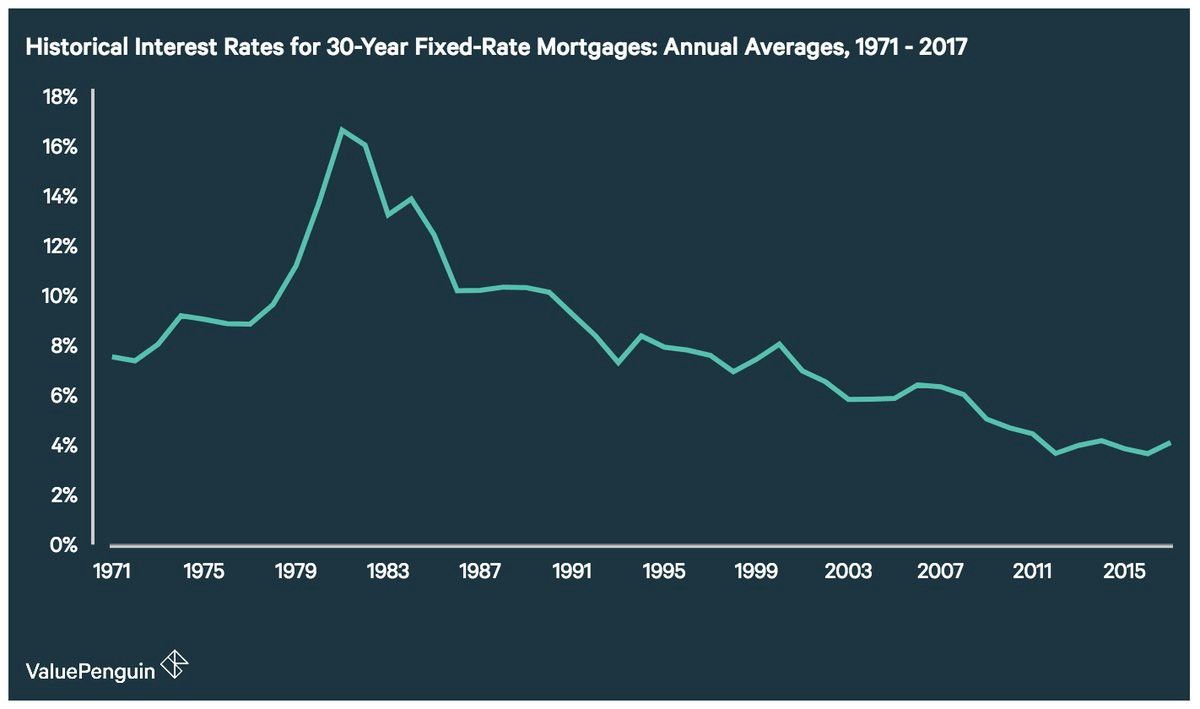

34/ Who you marry matters A LOT.

‘Marry 1 frugal spouse who shares ur dream of becoming financially independent. Weddings are about love & divorces are about money. Make sure that u & ur beloved r on the same page financially before signing up 4 life.’ If I Knew Then What I Know Now – Bogleheads.org

34/ “The Millionaire Next Door’ by @thomasjstanley (rip) could be 1 of the most important books u ever read.

Keeping up with the Joneses will destroy u. Screw the Joneses.

“Whatever your income, always live below your means.”

Buy the 📖: The Millionaire Next Door: The Surprising Secrets of America’s Wealthy

35/ I don’t buy into The Latte Factor. @Starbucks ☕️ & avocado toast 🥑🍞 likely aren’t to blame for your long term budget woes.

It’s the big things. Cars 🚗, houses 🏡 (size, location), college 👩🏽🎓, expensive brands…

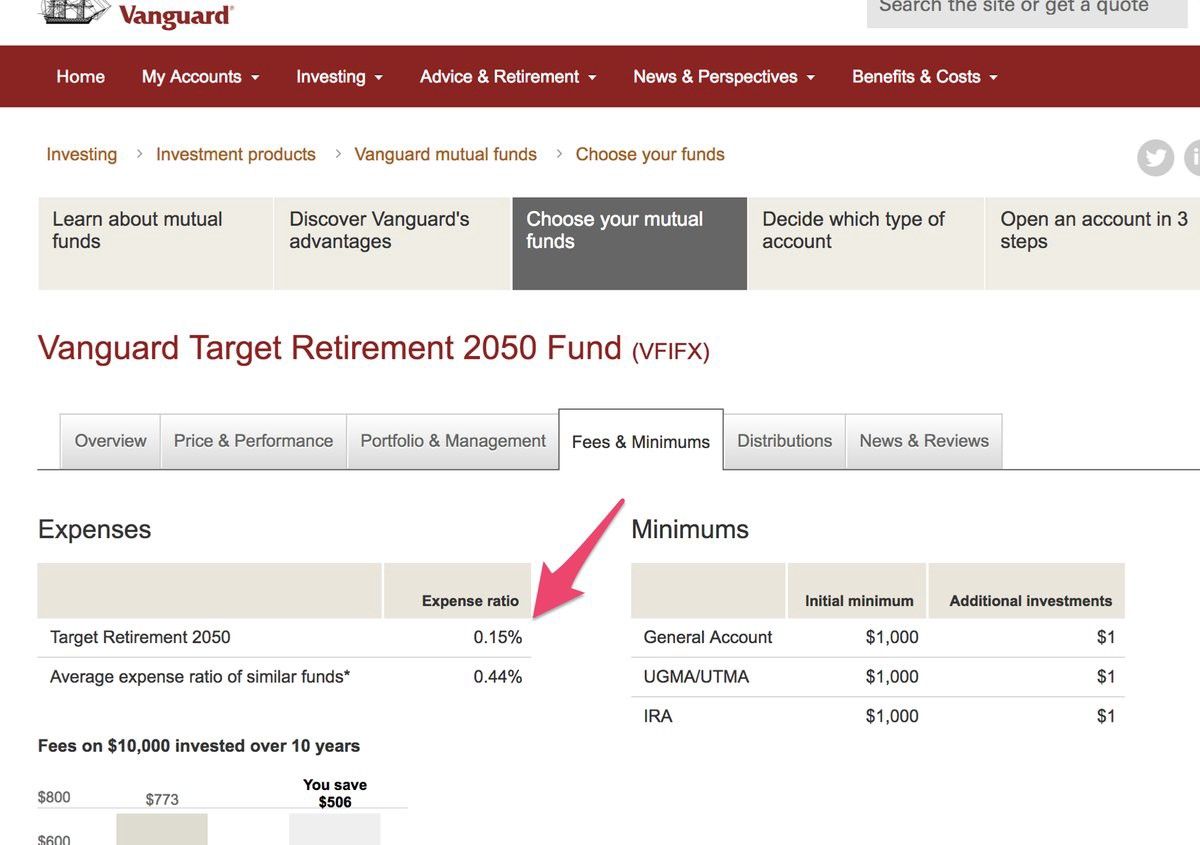

36/ Understand Account Types & their features.

- Tax-free, Tax-deferred, Taxable

* Roth, Traditional

* Contribution limits, Eligibility

* 401k, IRA, 403b, 529, HSA, ….

* Employer matches

* Fees

h/t @DavidNWaldrop Tax-deferred vs Tax-free Investment Accounts

37/

* Tax-Free: Pay taxes on the income now, withdrawal investment tax free later.

* Tax-Deferred: Defer taxes until withdrawal, ideally when ur in a lower tax bracket.

* Taxable: Withdrawal at any age without penalty. Pay taxes on the income in the year received.

38/

* Roth: Taxed now; not at withdraw.

* Traditional: Decrease taxable income now; pay taxes at withdrawal.

There are Traditional IRAs & 401ks.

There are Roth IRAs & 401ks.

Its likely wise to contribute to a Roth 401k if avail & to a Roth IRA if eligible (under the income limit).

39/

* 401k/403b: Employer sponsored retirement plan.

* IRA: Individual retirement account.

* HSA: Health Savings Account.

* 529: College savings plan.

All of these tax advantages account types have unique eligibility requirements, limits, and benefits.

40/ We’re not contributing to a 529. May change our minds later, but the longer we delay, the lower the appeal (remember, more time in the market, more 🧀).

Consider contributing if u know you’ll have a kid(s), believe in the future of college, and are maxing out elsewhere.

41/ Pro tip: You can actually open & begin contributing to a 529 Account even if you don’t have a child yet. Only do this if you’re confident that you’ll want to fund 1, and r OK if something gets in the way of conceiving, knowing that a niece or nephew can use it instead.

42/ Banking is changing. High school /college aged kids arent attracted to going to a bank to open their first checking or savings accnt.

@CashApp & @venmo offer them their expected experience. It’ll be a wild when they start getting their direct deposit there, buying $btc…

43/ 🐶 Dogs are great but also expensive & a pain the ass. We have 2; 1 by choice & 1 due to life being unfair and forcing us to inherit.

Be advised: Food, vet visits (always $200+), boarding for vacations, early mornings, random vomitting, mucho 💩…

44/ I’m indecisive when it comes to pet insurance. We have it for 1 of our 🐶 and it hasn’t paid for itself over the last 8 years… but I know we’ll wish we had it if we canceled it now.

FWIW we have @NationwidePet

45/ Follow @WSJ Personal Finance Columnist @jasonzweigwsj

Writer of ‘The Devil’s Financial Dictionary’ & editor of the 📘 ‘The Intelligent Investor’ by Benjamin Graham.

@WarrenBuffett said it ‘is by far the best book on investing ever written.’ Jason Zweig

46/ Benjamin Graham was an economist & professional investor known as ‘The Father of value investing.’ He taught & hired a guy named Warren Buffet.

His philosophy stressed investor psychology, debt minimization, buy-and-hold investing, FA…

Buy the 📙: The Intelligent Investor: The Definitive Book on Value Investing.

47/ Graham says Intelligent Investors:

* Know they can get ripped off easier by a dude with a pen than a gun

* Think IPO stands for ‘It’s Probably Overpriced’

* Understand margin of safety

* Refuse to spend too much for an investment

48/ Follow @Wu_Tang_Finance for a good laugh and some big knowledge bombs💣. He/she will get you thinking outside the 📦.

49/ Who doesn’t wonder how they’re doing compared to everyone else?

@StatusMoneyUSA enables you to anonymously compare net worth, spend, and income by age range, income range, geo, etc. Status Money

50/ A friend asked me to expand on y Im not funding a 529:

* Cant borrow💲as easily for retirement as 4 education

* Can borrow against 401k if really needed

* IRA earnings can be withdrawn penalty free 4 education

* Roth IRA contributions can be withdrawn penalty free + tax free

51/ I took a pay cut to join a very early stage (day 0) startup so I used this as an opportunity to cut unnecessary expenses.

1. Serial impulse @amazon 📚 buyer? Start utilizing the ‘Wish List’ feature. Saves💰

2. Review @AppStore subscriptions: How to cancel an App Store subscription

52/ The concept of Antifragility is fascinating (h/t @nntaleb).

My budgeting & investing decision making process revolves around positioning myself to: comfortably withstand extended bear markets (or job loss)

53/ I ❤️ this quote from the @netflix culture deck: “Prevent irrevocable disasters”

Sums up my personal risk management goals pretty well.

Similarly, ❤️ this line from @lil_dill @lyft:

54/ ‘Retire Secure’ by @rothguy is 1 of the best retirement books Ive read. Dont wait until your 50s to read it.

It’ll get you thinking about social security, healthcare, & withdrawal strategies; a topic I still need to learn a lot more about.

Buy the 📖: Retire Secure!: A Guide To Getting The Most Out Of What You’ve Got

55/ ‘The Bogleheads’ Guide to Retirement Planning’ by Taylor Larimore and @bogleheads is another good retirement planning book as well.

Buy the 📖: The Bogleheads’ Guide to Retirement Planning

56/ “Compound interest is the 8th wonder of the 🌎” — Einstein

Takes a long time to feel like ur making investing progress. Takes time to earn interest & then for ur interest to earn interest.

Your 1st $100k is a b*tch — Charlie Munger Charlie Munger: The First $100,000 is a B*tch – Four Pillar Freedom

h/t @4PillarFreedom

57/ “Compounding is the engine that will make our portfolios grow, time is the fuel. The key to compounding returns is they have a much larger influence on our fortunes later in life than they early on.”

– ‘Millennial Money’ by @patrick_oshag

Buy the 📖: Millennial Money: How Young Investors Can Build a Fortune

58/ Be responsible if you’re a parent. After making an educated decision on life insurance, get your estate in order.

Make sure to review/update it every few years. Tragedy strikes unexpectedly & it’s unfair for younger 1s left behind to have to fight for what you’d want.

59/ Estate Plan Primer (h/t @Wealthfront): How a Simple Estate Plan Pays for Itself

60/ Crypto throws a 🔧 into estate planning. ‘Cryptoasset Inheritence Planning’ by @pamelawjd is a good primer. I think a service like @CasaHODL will play a role in this eco a few yrs from now, as well as other services that dont yet exist.

Buy the 📖: Cryptoasset Inheritance Planning: A Simple Guide for Owners

61/ U will not be a successful trader. If u need to be taught this lesson, then I hope u do it when ur young while u have less 💸 to lose.

If u decide to speculate or trade (public stocks, crypto) then the rule of thumb is to limit the amount to < 5% of your portfolio.

62/ ‘Buy & Hold’ is a passive strategy that helps u ride out volatility & protect u from urself. It just means that u buy & don’t sell for a very long time regardless of market fluctuations.

I think of it as much as a mindset. It takes patience, humility, and strength 💪🏽.

63/ Credit plays a big role in personal finance in the U.S. You need to ‘build credit’ and maintain a healthy score. Understand the factors:

* Card utilization

* Payment history

* Account count

* Inquiries

* History age

Services like @creditkarma & @creditsesame are great. Credit Karma

64/ We live in a debt driven society. Responsible credit use is 🔑.

Credit cards 💳 are great:

* Builds credit

* Sign up bonuses = very valuable

* Buyer protections

* Dont need to carry cash (phsyical security)

* Waterproof

* Easy

* Rewards

65/ My Credit Card Strategy:

* @Blispay 4 everyday purchases (2% cash back) & big spend like vet bills, my 🚲, taxes, etc. (for longer term financing). Blispay

* @Chase, @AmericanExpress, @Citi cards just for sign up bonuses, redeemed later for travel 🌎.

*just use responsibly*

66/ @FlyerTalk is a great resource for travel planning and learning about hotel/airline rewards programs ✈️. Miles&Points

67/ Personal Finance is a skill that can & needs to be learned.

“It’s an intimidating topic because we have no idea where to start, and it’s hard to talk about money 💵 because it’s such a taboo topic.” — @thewildwong

h/t @timherrera @nytimes What to Do When You’re Bad at Money

68/ ‘Your Money Ratios’ by Charles Farrell was a surprisingly useful book (I expected it to be cheesy BS for some reason).

* The Capital to Income Ratio

* Savings Ratio

* Debt Ratios

* Investment Ratio

* Life Insurance Ratio

* …

Buy the 📘: Your Money Ratios: 8 Simple Tools for Financial Security at Every Stage of Life

69/ Our strategy as new dual-income married 👫: Separate Accounts but Joint Allocation & Tracking

* A little friendly competition can be healthy

* Consolidation requires high [enough] switching costs with little upside

* Treat as 1portfolio

More details:

https://www.quora.com/How-do-married-couples-handle-finances-together/answer/Jared-Franklin

70/ Very sensible, not overly technical. That’s how I’d describe the book ‘Four Pillars of Investing.’

1. Theory

2. History

3. Psychology

4. The Business

Buy the 📙: The Four Pillars of Investing: Lessons for Building a Winning Portfolio

Read it a while ago, but I attached a screenshot of my notes.

71/ Follow @cullenroche. He wrote a pretty good book called ‘Pragmatic Capitalism’.

It covers a wide range of topics from how Reserve Currencies work, why the US gov cant go bust, market myths, and more.

Buy the 📘: Pragmatic Capitalism: What Every Investor Needs to Know About Money and Finance

72/ I don’t have a ‘financial advisor’ 🕴️. Hard to find + trust. I’m confident w investments but could use for estate & retirement planning, alt investments, etc..

Supposedly @GarrettPlanning can be useful for finding 👍 hourly-fee based CFP’s. Financial Planner Directory – Find Financial Planners

73/ More 💰 opens more doors. Investment opportunities & money managers (many require multi-mil portfolio mins).

Accredited Investor rules are BS 🖕. Conceptually 👍 but implemented 👎. Im educated enough for riskier opportunities.

(h/t @financialsamura) What Is An Accredited Investor And Is The Definition Fair?

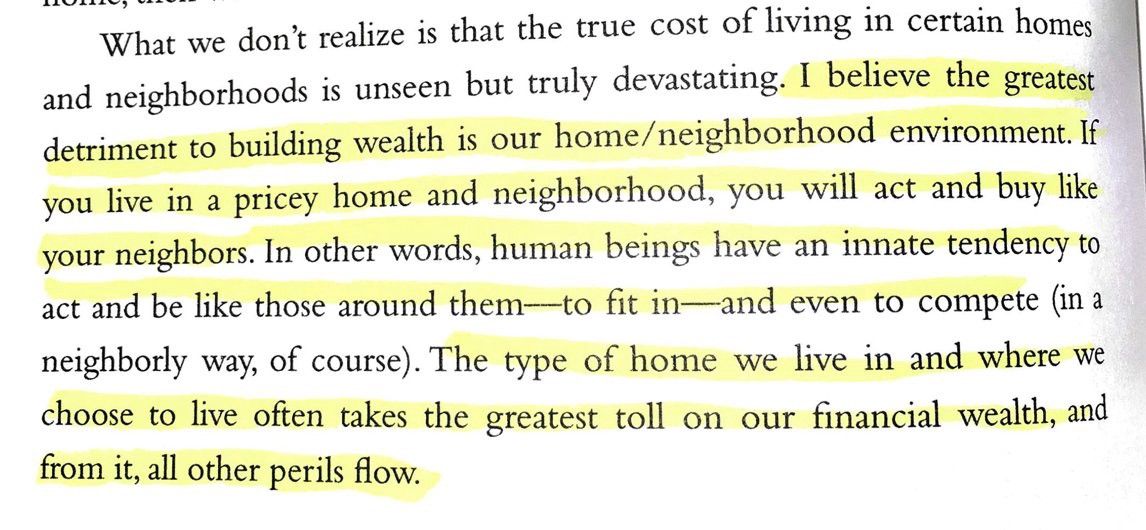

74/ “The type of home we live in and where we choose to live often takes the greatest toll on our financial wealth, and from it, all other perils flow.”

– 1 of my fav takeaways from the book ‘Stop Acting Rich’ by @thomasjstanley

Buy the 📘: Stop Acting Rich: …And Start Living Like A Real Millionaire

75/ No kids for us, yet. We’ve decided that we hope to just have 1 👶. We think this will provide us with optimal balance in life.

The decision far from just money driven, but 💲 is certainly a factor.

(h/t @awealthofcs)

76/ Career Management.

Your job is likely the biggest contributor to ur earnings & has a huge impact on your life. We spend as much time with coworkers as our significant others.

* [Try] Choose a fulfilling career path

* Negotiate

* Understand at-will employment

77/ Choose a fulfilling career.

My wife is a peds nurse practitioner 👩⚕️& always knew she wanted to go down that path.

Feeling fulfilled is very valuable💲. Obviously most people dont really ‘choose their path’ (myself included). But its a luxury to not hate work.

Seek 😃

78/ Negotiate.

It’s uncomfortable & awkward but expected. There was a great passage in a 📖 that I’ll always remember but can’t find right now. Went something like:

You won’t get what u don’t ask for. Ask for what youwant. Ask until its beyond uncomfortable. Be told no and ask again.

79/ At-will Employment.

Most people think they’re married to their company (and that their company is married to them). False 🚫 because your contract is likely at-will.

Basically, u can leave & they can let you go. Don’t be scared by it; embrace it. At-will employment – Wikipedia

80/ I work at a “tech startup” & compensation includes salary + equity (among other benefits).

Equity is an incredible motivator but assume your startup will not become the next $FB or $GOOG.

This guide by @HollowayGuides is the best I’ve come across: The Holloway Guide to Equity Compensation

81/ Not all ‘startups’ are created equal (actually, none are). People assume startups are risky. False 🚫.

I view huge companies as risky, ready to do layoffs at any moment.

I break startups into 2 camps: pre & post product/market fit. Post is really just a small company to me.

82/ Schools of economic thought: Austrian vs Keynesian vs Chicago. I plan to focus some attention to this area in the near future.

I’m not educated enough yet to ‘take a side’, but I have to say that fractional reserve banking seems & feels… icky. Fractional Reserve Banking

83/ Our monetary system is undoubtably consumption & debt based, and it influences our entire culture.

Follow @real_vijay and @saifedean if you’re interested in questioning if this is how it should be.

Good primer podcast (h/t @villageglobal).

84/ Earning requires working and work is usually really hard. Even if work isn’t that hard, I appreciate people who do.

The only none finance book I’ll mention in this thread is called “Grinding it Out — the Making of McDonald’s” by Ray Kroc himself. Grinding It Out: The Making of McDonald’s

85/ Inflation.

It’s the reason people say you’re losing 💸 by letting it sit in a checking account (aside from the opportunity cost).

As inflation increases, each $ buys less. If its 2% in a year, u should demand a raise of at least 2% to keep up. All About Inflation

86/ Interest Rates.

The % charged by a lender to a borrower. The only time this will be favorable to u most likely is in ur savings account.

They’ve been low recently. This appears beneficial for u when you borrow 💸 for a mortgage. Don’t be surprised when they increase soon.

87/ “Beating inflation is the only way to increase your wealth.” — @AlderCoveCap Personal Finance 101 in a Single Picture

88/ The book that started it all for me was “I Will Teach You To Be Rich” by @ramit during my 1st year of full time employment. Great personal finance primer.

Bit dated now but buy the 📘 for a younger loved 1: I Will Teach You To Be Rich

89/ Emergency fund 🚨.

Rule of thumb is to have 6 months of living expenses (rent/mortgage, utilities, food, etc.) set aside for when it 🌧. Savings accounts r a good place to stash it. @GoldmanSachs $GS Bank, @AmericanExpress Personal Savings, @capitalone 360, @allyfinancial

90/ Pay to take care of yourself.

You want to be able to take advantage of the freedom FI provides. @PeterAttiaMD teaches lifespan (length) & healthspan (quality). @classpass played a role in my journey to discover a routine 🚵🏼♀️.

h/t Patrick O’Shaughnessy How to Live a Longer, Higher Quality Life, with Peter Attia, M.D. [Invest Like the Best, EP.27]

ClassPass

91/ Don’t overspend on gifts (including cash).

Don’t gift based on what the Joneses are or on what you think they are. You’re not the Joneses, and it’s likely that they’re giving more than they should responsibly give anyway.

92/ Charity 👍. Make yourself feel good and give $10 to @JDRF right now:Make a Donation – JDRF

93/ Last @thomasjstanley book rec… ‘The Millionaire Mind’

The book highlights a lot of survey results re: millionaires such as GPA (2.9/4.0), SAT scores (1190/1600), and the ability to always show up.

Such a great book: The Millionaire Mind

94/ Understand Expense Ratios. Primary comparison metric between similar funds. Deciding between a Target Date Retirement Fund between @Vanguard_Group & @AmericanFunds? Look at the ER. Lower = better. FYI u can usually trust that @Vanguard_Group will be 👍.

95/ “Show me the incentives and I will show you the outcome” — Charlie Munger.

Concisely explains a driving force behind everyones actions; especially sales forces. Be wary of what anyone is selling u, or advising you of. Try to understand what their incentives are 🔎.

96/ Successful investing is counterintuitive.

Don’t be a follower; be a contrarian. You’ll doubt yourself when you press the submit button for a buy when everyone else is selling. Be 🆗 with discomfort.

97/ Investment Risk.

* Systematic: aka Market Risk. Reaction of individual stocks to market swings.

* Unsystematic: Variability independent from the market movements. Result of factors peculiar to an individual company like accounting fraud, labor trouble, etc.

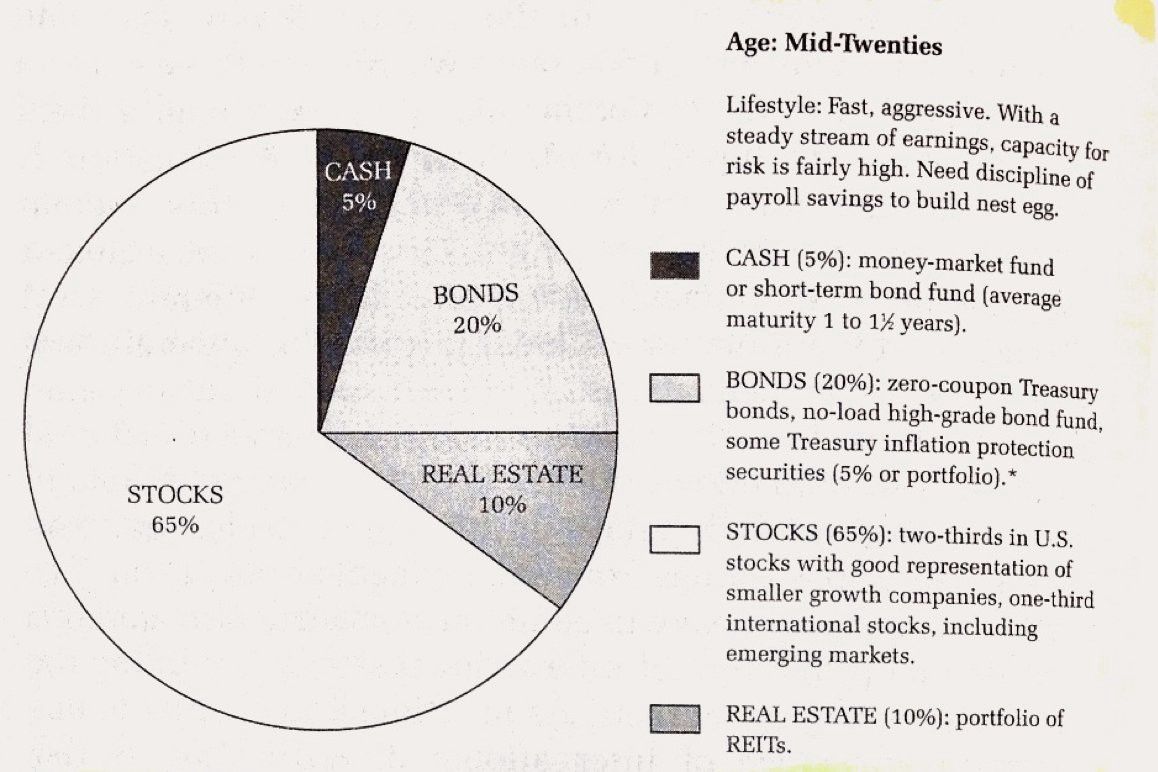

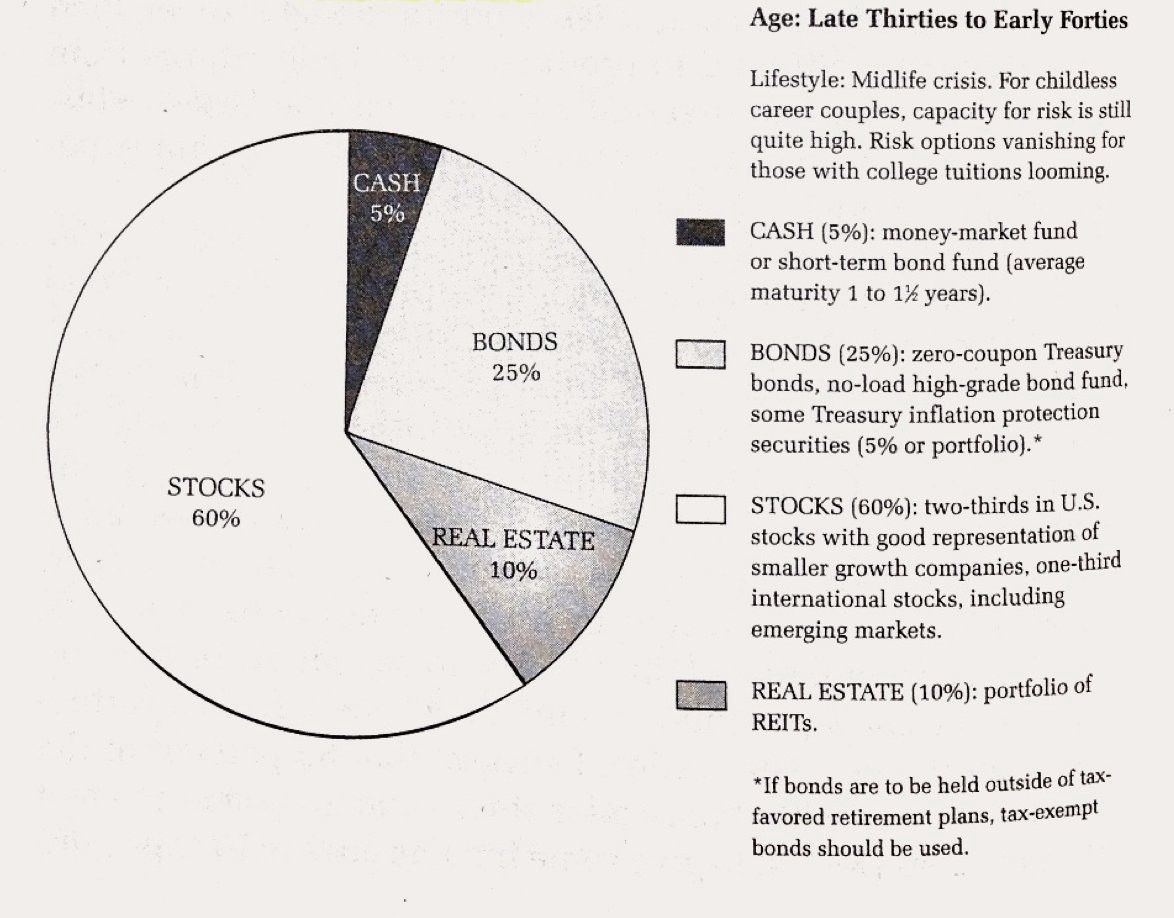

98/ Asset Allocation 🍕.

How you’ve divided your investment 💲. Super personal — dependent on age, risk tolerance, economic outlook, retirement goals, spend needs… Attached examples from ‘A Random Walk on Wall Street’

99/ Taxes.

Pay them. Don’t F around. I’ve done them myself using @turbotax in the past but I prefer to pay a trusted friend now (easier + accounting fees are deductible). Follow @CryptoTaxGirl (congrats on Y Combinator)

100/ Fam & friends + business = 🚫 For me at least. It’s so much simpler and safer that way.

101/ Place Credit freezes with @Experian_US, @TransUnion, and @Equifax.

Just remember to temporarily lift them prior to applying for any sort of loan.

Heres how data breaches made a big business out of buying & selling personal information online: How the dark web makes identity theft easier

102/ Social Security ☠️.

Calculated by averaging your top 35 earning years (adjusted for inflation).

But don’t count on receiving it if you’re young. Even if u end up getting some of it, it’s better to plan for not getting any. Which sucks… because you contribute a lot to it.

103/ Adam Nash covers most of the topics in this thread + more in his @Stanford CS007 ‘Personal Finance for Engineers’ course. The 2018 course material is available here:

CS 007: Course Material (2018)

104/ 13:30 starts a nice segment on the controversial topic of homeownership with @JLCollinsNH from his talk @Google

‘I’m not anti-homeownership… I’m anti believing the propaganda that it’s always a great financial decision…’

105/ Personal finance is considered a taboo subject, but is super important, sorely misunderstood and under-taught. If you have a solid grasp of the fundamental, then do like @abarrallen and help educate others.

106/ If you found this thread useful, then you owe it to yourself to learn about the history of @Vanguard_Group and Jack #Bogle. Here’s a thread on his last book/memoir before he died in January 2019:

107/ Recognize where you are in your earning years. Making a lot of money? Be a conservative planner. High income ‘too shall pass’ like everything else.

108/ Don’t blow money on stupid shit. ‘Stupid shit’ is subjective but I’ll include jewelry in that classification.

109/ “If I knew then what I know now” by Michael LeBoeuf is 1 of the best posts I’ve ever read on the bogleheads forum. Great advice for college students or anyone early in their careers.

https://www.bogleheads.org/forum/viewtopic.php?f=2&t=161092#p2418254

10/ Be an ‘owner’ (of a business & yourself).

This epic post by Danielle Morrill embodies the importance of owing a piece of a business (in her case, being an early @twilio employee), as well as to own your life instead of letting outside forces own it. Post-Startup Life: Reflecting on My First 18 Months Living in Denver

111/ Free $$. Take advantage of Referral codes (give + get).

- @onepeloton: 3TWTMH

- Wealthfront

- Betterment

- Fundrise

- @CashApp

112/ Enjoy this thread & want to read more?

Michael Flaxman has you covered. His epic post covers many of the same topics + more (investing, taxes, asset classes, robos, psychology, timing, credit cards, life insurance…).

113/ Investment firm memos are awesome reads. This 1 from Semper Augustus is pretty amazing.

“Mistakes in life and in investing make you better, particularly if you force yourself to learn from them… Hard work makes you better, but it only allows you to keep up.”

https://static.fmgsuite.com/media/documents/db18a736-5a8c-410d-9ae2-55b21bf773e2.pdf

114/ Be different. Unless you’re fortunate enough to have family bankroll a pricey wedding w/out negative impacts to their financials, dont take out loans or spend the national average of $35,000. We did a destination & it was significantly cheaper.

115/ Buffet FAQ / @CNBC. Get lost in these archives.

116/ @jdstein hosts a podcast called Money Like the Rest of Us. A recent episode recommended a new book called @ChooseFi by @caniretire_yet. Typical ultra-frugal FIRE’rs arent for me but it was actually really enjoyable. Have u had an awakening yet?

117/ Q3 Investor Letter from O’Shaughnessy @patrick_oshag “… cheap public companies—a category that has done very poorly since the financial crisis—appear as attractive relative to the market as they have since 2000.”

https://osam.com/pdfs/research/Q3%202019%20Investor%20Letter.pdf

118/ Auto loans & leases are at ATHs ($1.19T)! 33% of trade-ins have negative equity (also an ATH). Know what’s cool when it comes to cars? LOW CAR PAYMENTS and reliable cars that will last a long time. See tips from @awealthofcs regarding SUVs.

https://awealthofcommonsense.com/2018/07/are-suvs-ruining-retirement-savings/

119/ I’m a big fan of @stephonee. She’s sharing her net worth progress and tracking methods. Similar to the reasons I started this long thread, she says ‘this site offers no “get rich quick” schemes… the goal is to put you in a better financial position.’

120/ “Family Inc.” by @doug_mccormick is 1 of the most important Personal Finance books alongside @ramit’s “I Will Teach You to be Rich.” I highly recommend young professionals check it out. Your Family CFO manages:

1. Temporary labor biz

2. Asset mgmt biz

121/ “Ten Things I Wish I Had Known in My 20s” by @BlairReeves is that post you read when you’re young & agree with but brush off 40 seconds later. In your 30s? Then you’re prob mature enough. It’s still relevant and isn’t too late.

http://blairreeves.me/2018/03/20/ten-things-wish-i-had-known/

122/ Accumulating is only part of the battle. Draw down strategies are complicated & you should start thinking about it well before retirement. This thread by @millerak42 covers an example of considerations regarding social security & target date funds.

123/ I’ve been waiting for the ‘perfect’ @dollarsanddata blog post to add him to this thread but every single one is great. Follow him and spend some time on his blog. His latest: https://ofdollarsanddata.com/the-biggest-lie-in-personal-finance/

124/ Feeling panicky? @awealthofcs explains why you likely don’t need to *panic* sell or panic buy this week or next. Take your time. Relax. “…every bear market in the history of U.S. stocks has led to new all-time highs…”

125/ Investment memos written in 2020 will be popular for decades. @HowardMarksBook@Oaktree produces some of the best. “Even though there’s no way to say the bottom is at hand, the conditions that make bargains available certainly are materializing.” https://www.oaktreecapital.com/docs/default-source/memos/weekly.pdf

126/ 2020 is fucking wild! This is 1 of those uncertain times that you only experience 2-5 times in a lifetime. And I’m capturing the moments in this living doc for future reference. /2020/03/25/2020-corona-crash-or-everything-bubble-pop/