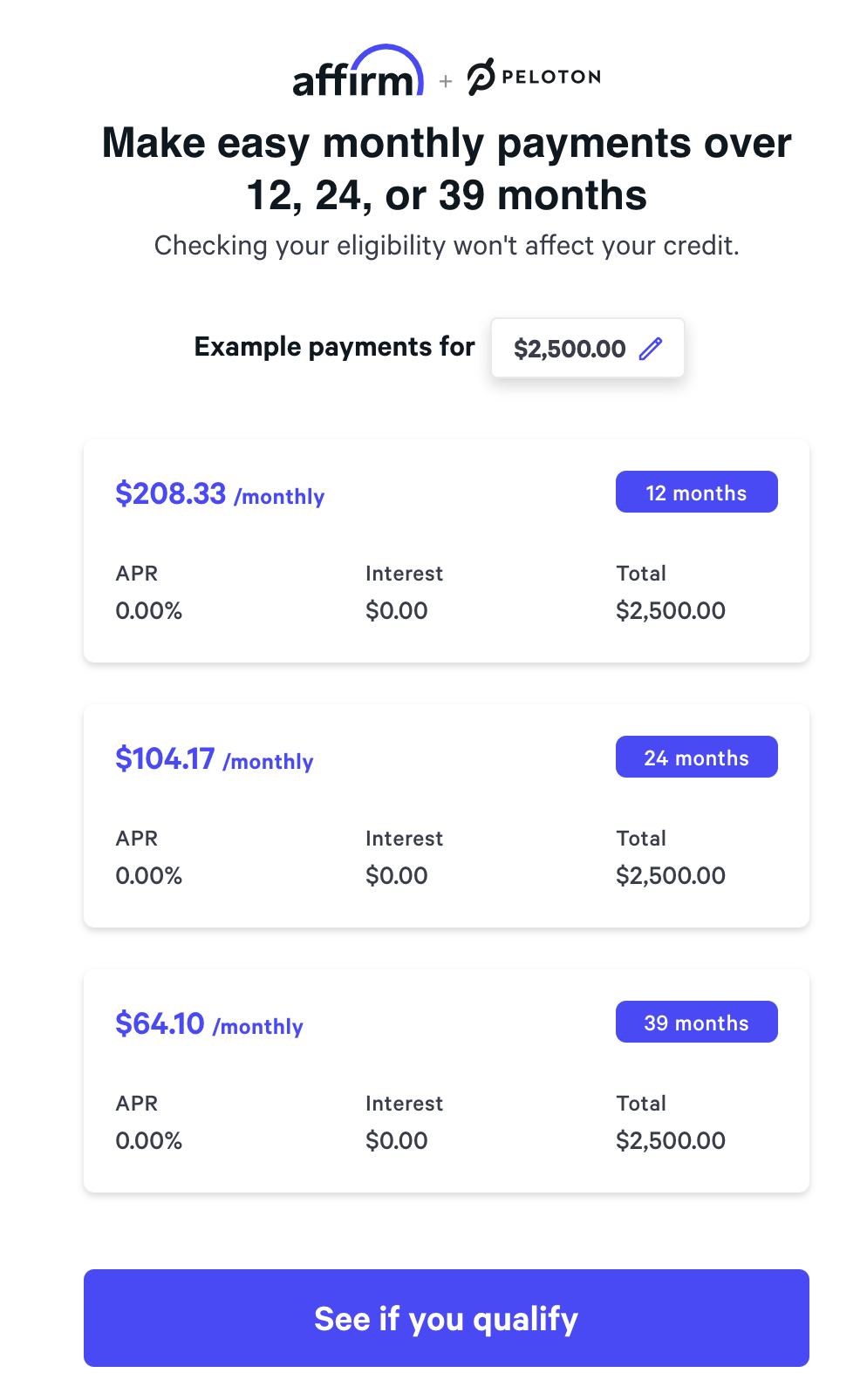

How to BNPL

I've written about Peloton a few different ways, like here and here. Figured I'd share how my wife and I justified the purchase to begin with, and what the numbers look like now that we're done paying it off.

BNPL has become a hot fintech buzzphrase. It stands for "Buy Now Pay Later." Although buzzy, it's not actually new. I worked at a company called BillMeLater (now called PayPal Credit) well before Affirm or AfterPay existed. It offered a similar value prop to both consumers and merchants.

Affirm is the perceived leader in the space. They've done a killer job partnering with amazing consumer brands such as Peloton over the past few years.

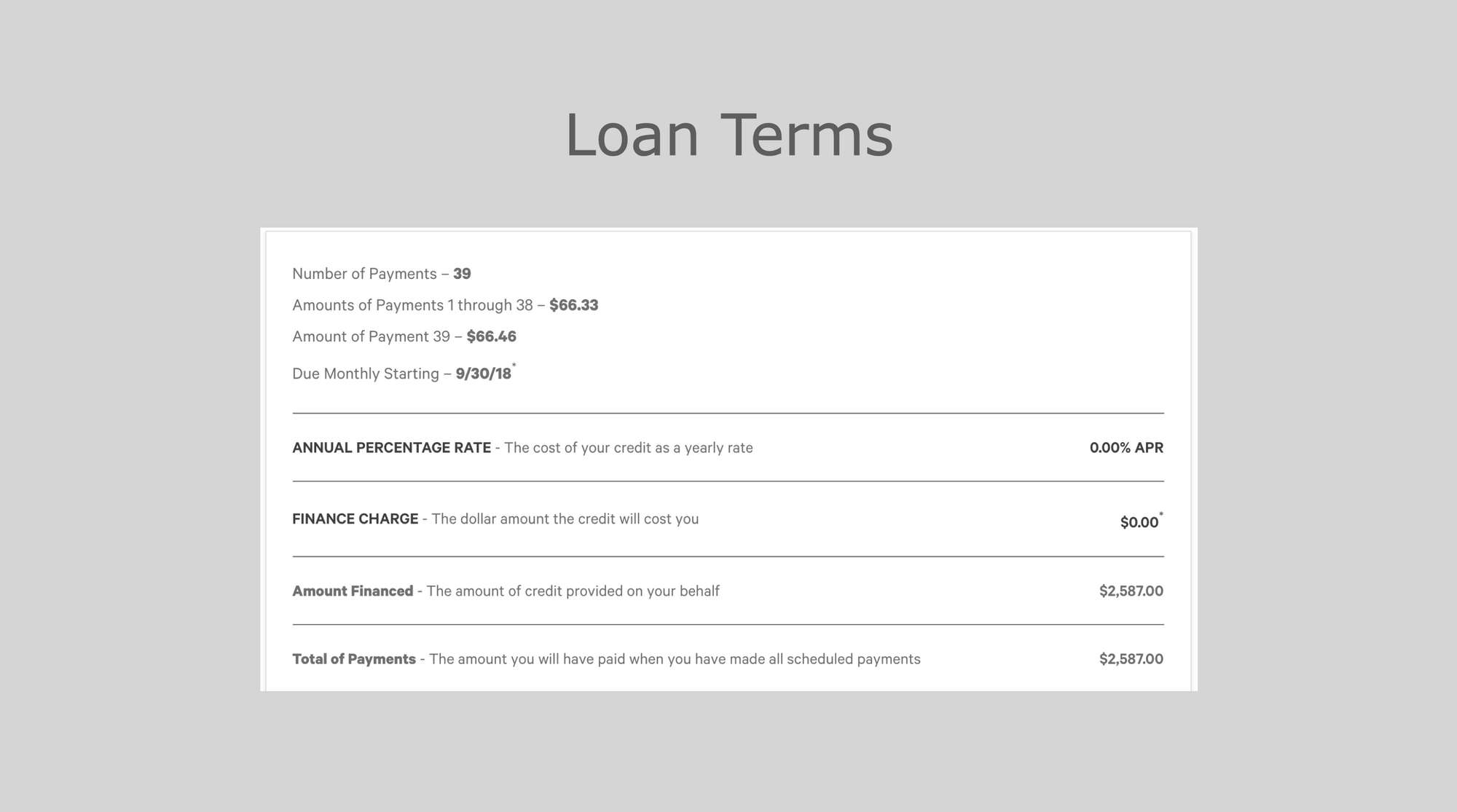

This post is a good example of how to responsibly leverage this type of financing as a consumer. We are a BNPL success story. The reason I personally find these types of offerings intriguing is because they can be a true win-win-win for all parties involved. Affirm won, Peloton won, and my wife and I won. With that being said, I know people use credit for different purposes, and qualify for different terms. This post just focuses on my example.

Prior to Applying & Buying

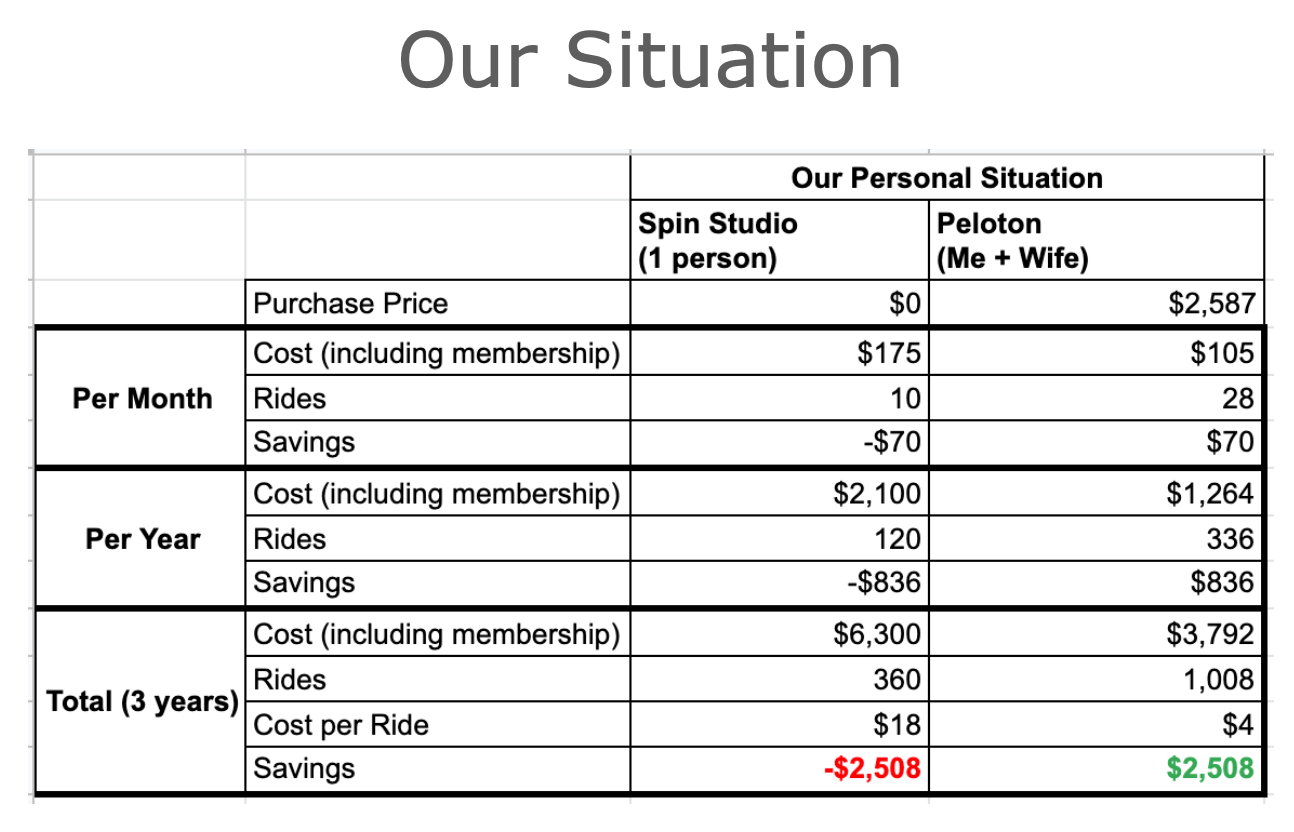

- I was paying $175/month for an unlimited spin studio membership. I found myself attending 2-3 classes per week. I wanted to attend more often but schedules didn't line up well enough.

- I had a desire to introduce other types of 'spinning' such as endurance/zone 2 rides, but studio classes are always just super high intensity.

- My wife had never gone to a spin class at a studio, despite having a desire to introducing spinning into her life. As a type 1 diabetic, there's a lack of predictability that you have to live with. Timing things like working out is far more difficult for people like her than it is for the rest of us.

Decision to Apply & Buy

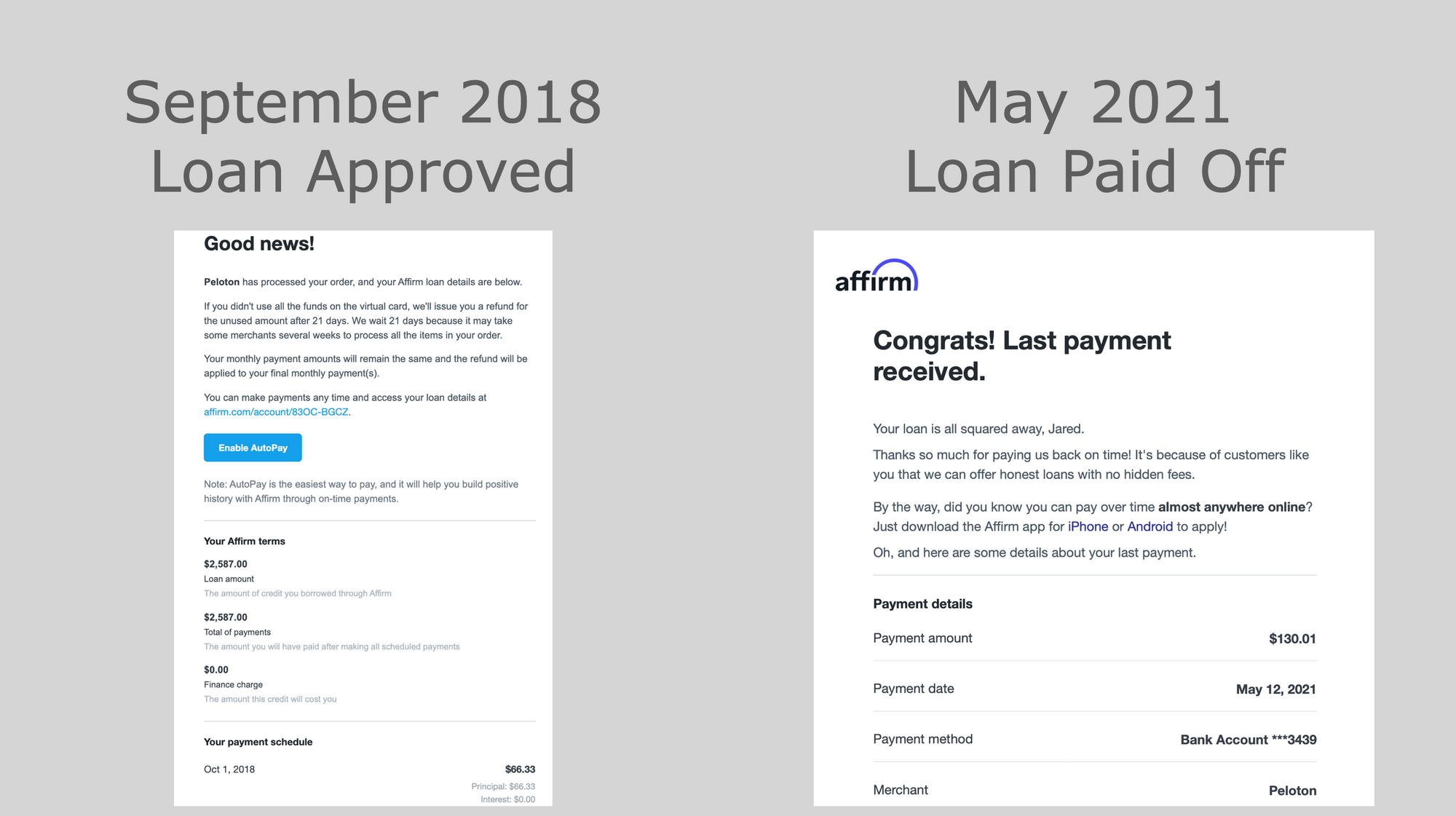

- We had nearly perfect credit so we knew we'd likely qualify for a 0% APR.

- I already knew that I'd work out a lot more if I had a bike at home than if I had to attend scheduled spin classes in person.

- My wife really wanted to start spinning, and this would afford her the ability to work out when it was best for her. And if she needed to hop off, she could without feeling guilty of wasting an in-person class.

- I was already spending $2,100/yr for my studio membership, which wasn't too far away from the price of a new Peloton bike.

- The $39/month Peloton membership also grants you access to other types of workouts (running, yoga, strength, etc.).

Savings & Benefits

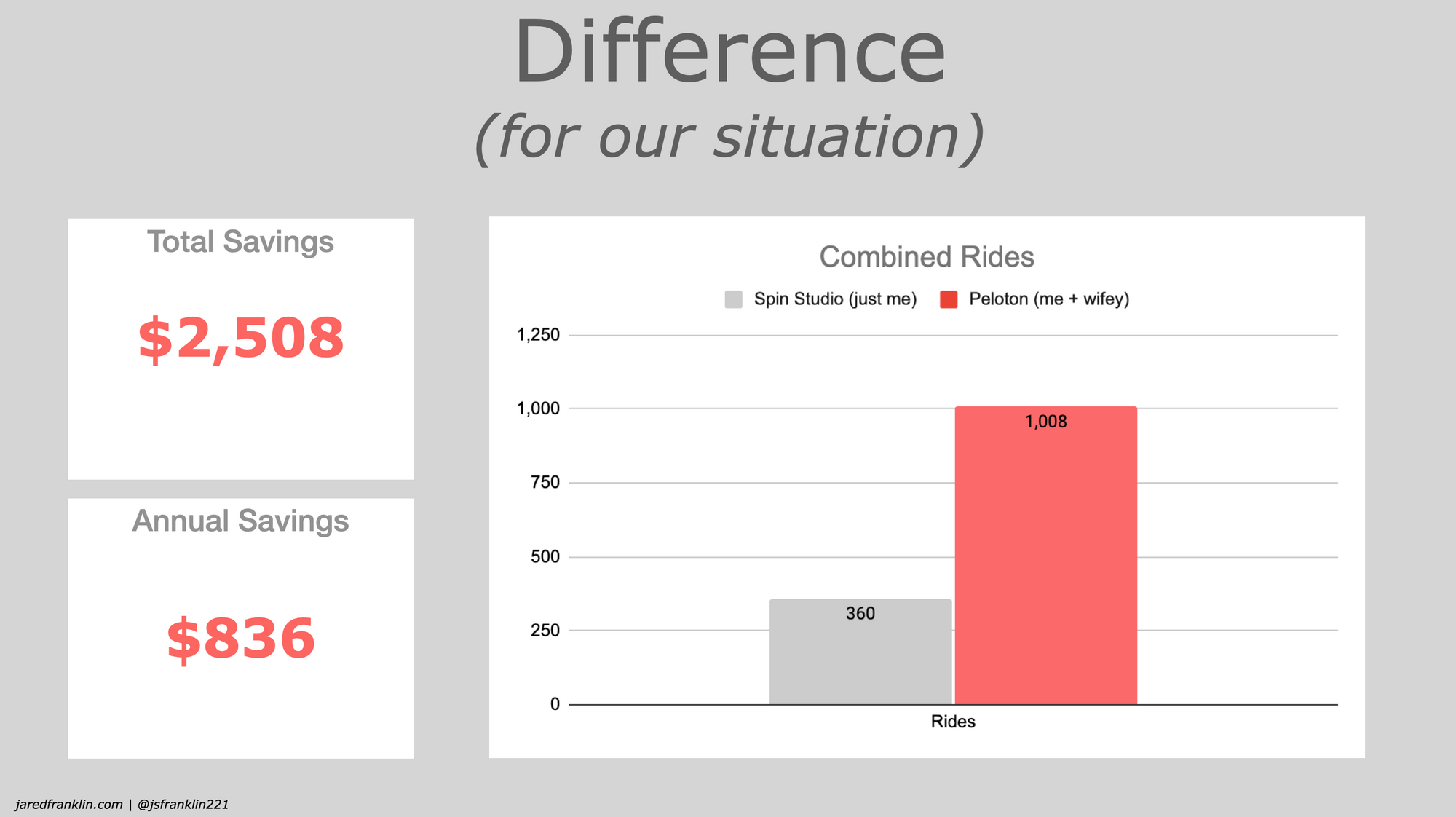

- We saved a total of $2,508 over the life of the 3 year installment plan by buying a Peloton that both of us used vs. just myself continuing with my spin studio membership. And we own the actual bike outright which tends to hold a really strong resale value.

- Combined, we did about 1,000 rides by owning the Peloton vs. just myself doing about 360 rides if I just continued attending a studio by myself.

That 2nd bullet is probably the biggest benefit and key point in this entire post. We both exercised significantly more than we would have otherwise. In fact, I wouldn't be surprised if I would have ended up canceling my membership when I moved and never restarting again. Not to mention Covid – we could continue our routine without any interruption. We are both significantly healthier now. Owning and having the luxury of working out from our own house has been a huge win for us.

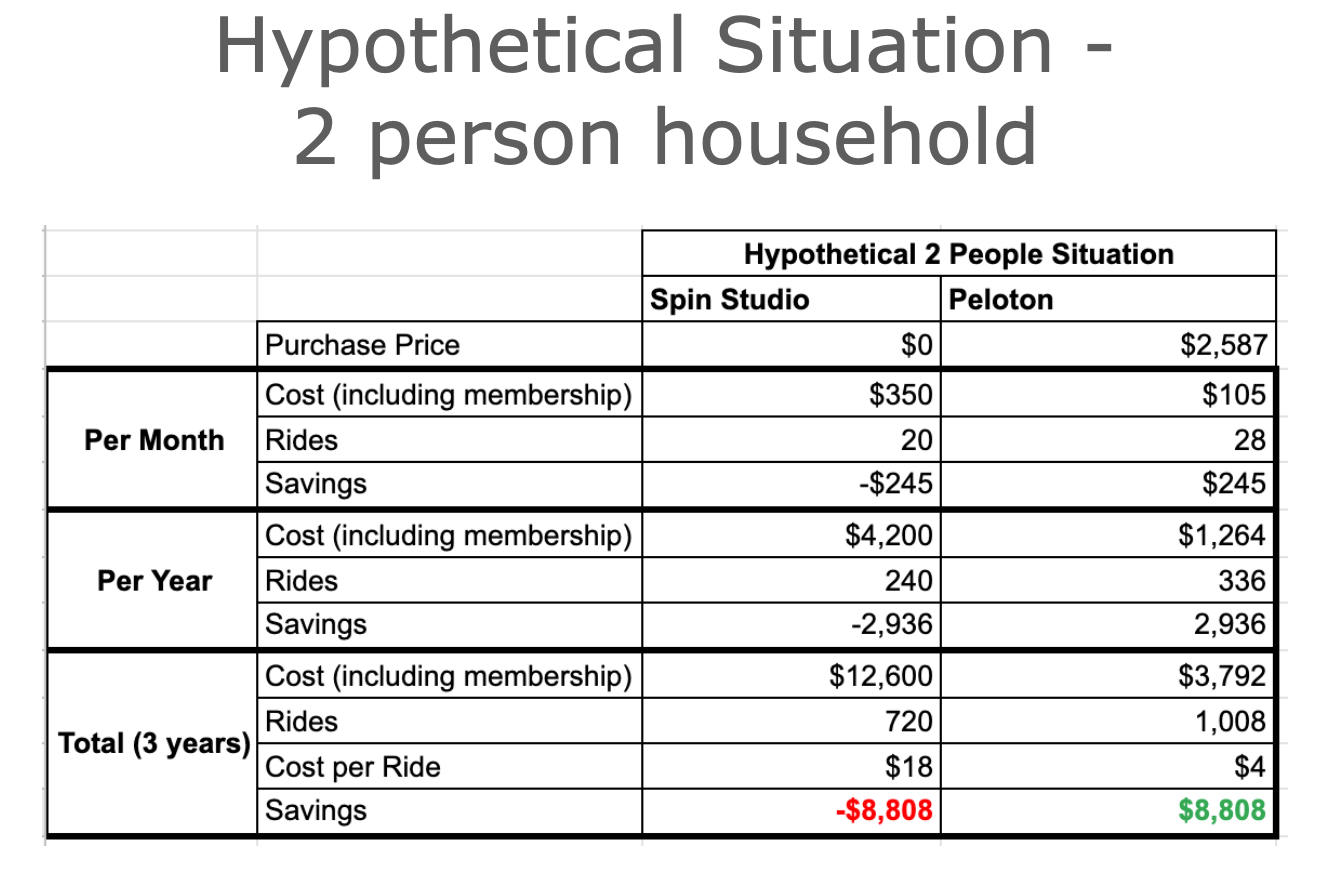

If you hypothetically play this out with a household of 2 people who are comparing a Peloton (for which you pay a single membership) vs. a studio that both would be willing to go to, the savings would actually be $8,008 over the 3 year period!

Takeaways

- BNPL can be used different ways based on different peoples needs. It can get a negative review when people talk about it very generically – you know, questioning why someone needs to break a $140 pair of shoes into 4 installments. It's important to segment the types of users and use cases when analyzing whether it's 'good' or 'harmful' form of credit for consumers.

- We're both significantly happier and healthier for having bought the Peloton. We kept up with it and couldn't imagine life without it. And we wouldn't have bought it without Affirm offering a 0% APR installment program to us.

- Things start to get really exciting in year 4 where the only Peloton cost for us is the $39/month membership fee. So it'll cost a total of $480 for my wife and I, opposed to the $2,100 a studio would have cost me, or the $4,200 it would cost the hypothetical duo.

Next up... Tonal.

$4,001.80 loan | 48 monthly payments of $83.37 | 0% APR