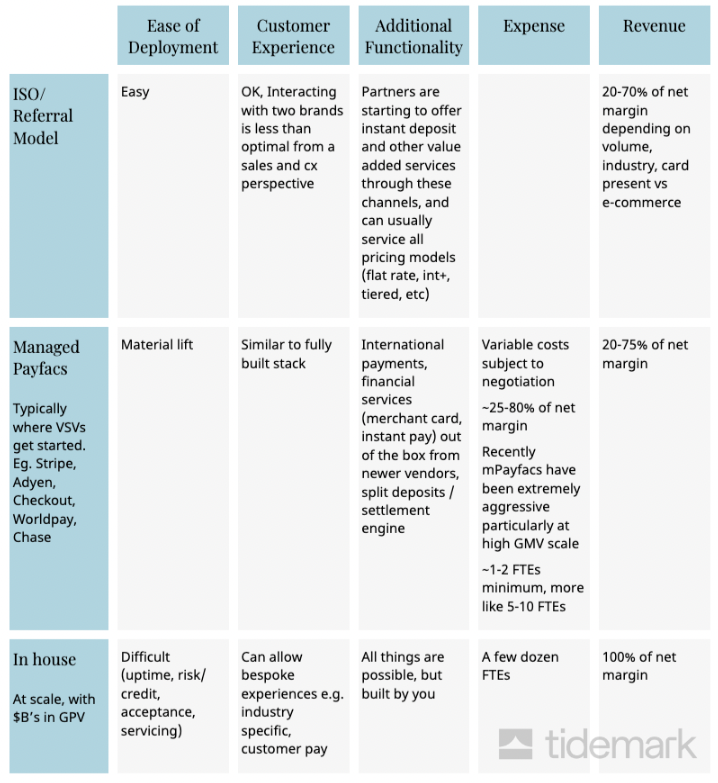

Payments Plus

Some of the most generational fintech companies are those which I prefer to categorize as "Payments Plus." Payments are core to their value prop, and as a byproduct, the business model relies heavily on transactional revenue. But they also provide value aside from facilitating transactions. These companies usually use payment processing as a wedge to onboard businesses onto their grander software stack. In many cases, it's vertical SaaS meeting payments. In some cases, a Payments Plus company may partner with a payment processor and refer customers for a referral fee while in others or at least down the line, they build completely in-house for improved monetization.

While these businesses are gorgeous in hindsight, it takes many years to create a sensible, functional, full-fledged product suite and flywheel.

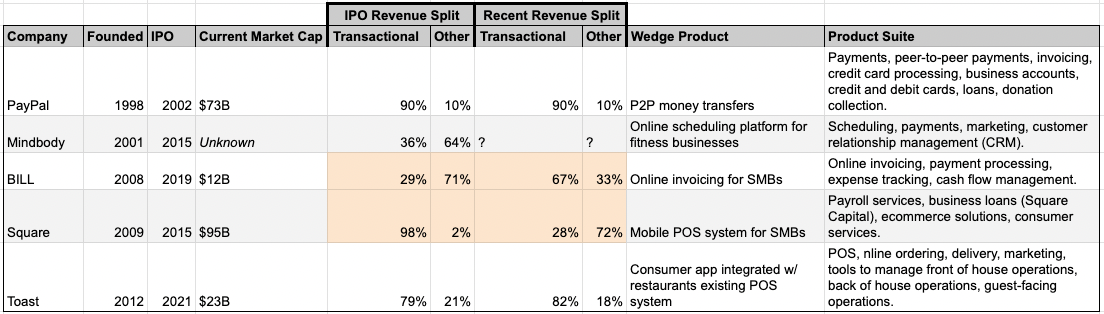

In the table above and throughout the rest of this post, I highlight some of those generational companies – PayPal, Mindbody, Bill.com, Square, and Toast. Each started with a single product and value prop. Over the decade(s), each has grown their product suites as they've grown market dominance.

I was curious how their evolving product suites impacted their revenue split. Both PayPal and Toast have remained steady from initial IPO to today. Squares revenue mix was heavily transactional when going public in 2015 but as of Q1 2023, is the minority of total revenue. Conversely, transactional revenue made up just 29% of BILL's when they went public in 2019, but has grown to 67% in their latest quarterly report.

While this post focuses on revenue splits, it doesn't really talk about revenue quality or margins. It's worth noting that margins on transactional revenue are lower than pure software. Using Toast as an example, 13% of revenue is the monthly SaaS fee with 70% gross margins. 82% of their revenue is transactional, which has 23% gross margins (similar to Shop Pay's margin profile). So overall, Toast's margins are around 30%.

Payments Plus businesses are beautiful at scale. They have strong staying power, powerful flywheels and network effects.

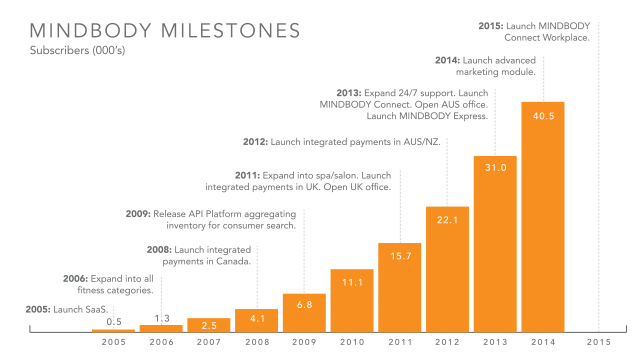

Mindbody

Mindbody started in 2003 with a business management SaaS product for the wellness industry, initially targeting yoga and pilates studios. Mindbody eventually expanded to fitness centers, dance studios, spas, salons, and beyond. They then broadened services to include payment processing, marketing, website development & hosting, and a marketplace for discovering and booking fitness classes. Mindbody is a great example of attacking and dominating a niche.

As stated in their S-1, "our integrated cloud-based business management software and payments platform is specifically designed to address the unique requirements of the wellness services industry. We help our subscribers simplify their operations, focus on their consumers and grow their revenue by enabling them to attract and retain consumers." Later, they articulate the case for integrating software and payments, hence Payments Plus or software-led payments: "The seamless integration between our business management software and payments platform provides a convenient one-stop solution for our subscribers. Subscribers save time and resources by avoiding the use of a separate payments platform and the associated burdensome manual reconciliations of transactions that result from a lack of automation. We believe that this integrated software and payments capability leads to higher subscriber engagement with our platform and a larger recurring revenue stream for us. Our payments platform enables swiped transactions at the front desk between consumers and subscribers, transactions with securely stored credit card data and ecommerce transactions through web and mobile interfaces. This integrated capability vastly simplifies back office administration and accounting, while enabling our subscribers to boost their revenue."

Here's a shot of their evolution from their S-1:

Obligatory flywheel slide:

Unlike PayPal, Square, and Toast, revenue was dominated by subscriptions (64%) even though they became an ISO relatively early to increase payment processing margins. Unfortunately, I'm unsure of their current revenue split since they were taken private by Vista in 2018 for $1.8b.

BILL

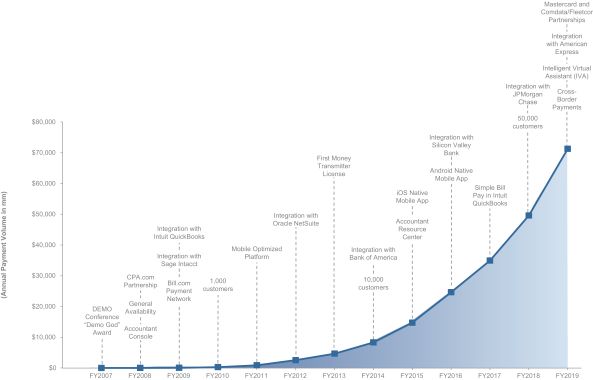

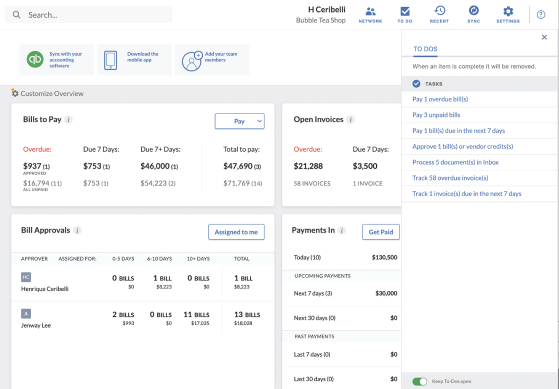

Bill.com began as an online business payments network for SMBs. The platform now supports AP / AR automation, international payments, virtual card support, workflow management, and integrations of these processes with accounting software like QuickBooks and Xero. During a time when 'most SMBs were still dependent on manual accounts payable and accounts receivable processes,' BILL provided digitization and automation so customers could manage their financial workflows end-to-end, placing BILL near the center of an SMBs financial operation.

Here's a shot of their evolution from their S-1:

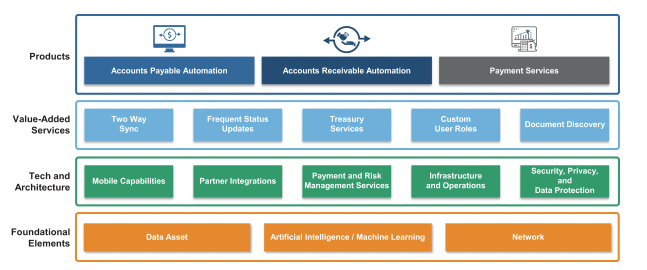

And a shot of their product platform:

BILL generates revenue by charging subscription fees, transaction fees, and by earning interest on funds held in trust on behalf of customers while their transactions are clearing. Unlike PayPal, Square, and Toast, transactional revenue was the minority when going public, making up just 29% of total revenue. However, it has reversed, and today transaction revenue is 60% of total revenue when excluding Divvy and Invoice2go, and 67% when including them.

Square

(I still can't bring myself to call them Block)

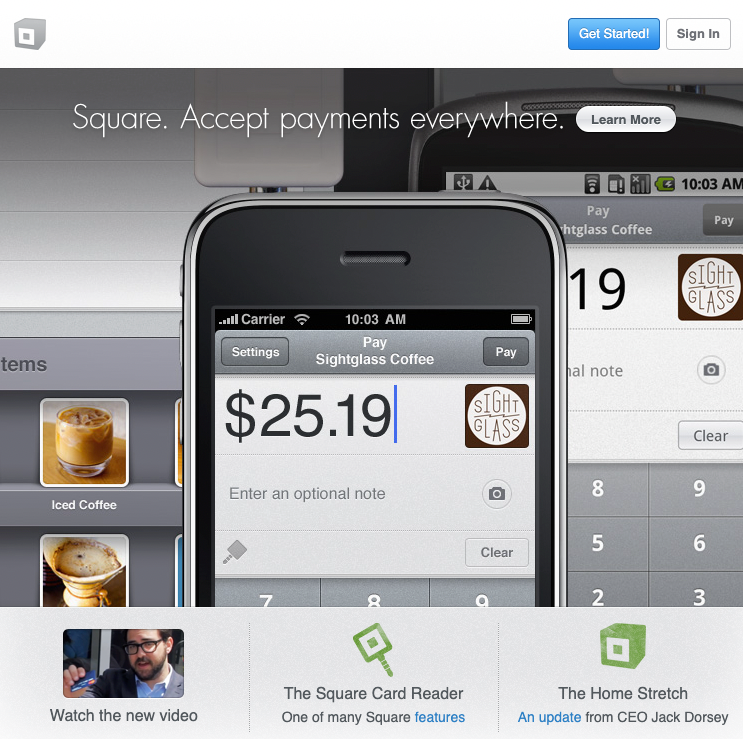

Square began as a mobile payment company that provided a small, square-shaped credit card reader that plugged into a smartphone. I almost didn't lay it out like that but then realized some readers may be so young that they don't remember how fucking cool and transformative this was – enabling anyone with an iPhone to swipe a card. For many of us who have worked in fintech for most of our career, Square was our north star. They brought a level of craftsmanship that most of us could only dream of inside our organizations. Square's suite expanded to include full point-of-sale systems, online payments, business financing (Square Capital), employee management, and consumer-oriented services.

Yes, this was considered pretty back in 2010. But more importantly, the entire experience as a merchant, end-to-end, was magical.

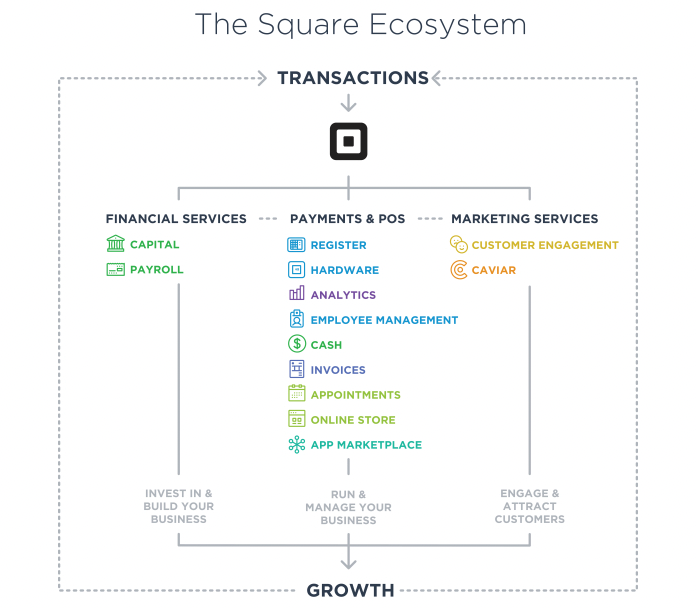

The Square suite was quite comprehensive by the time they went public in 2015:

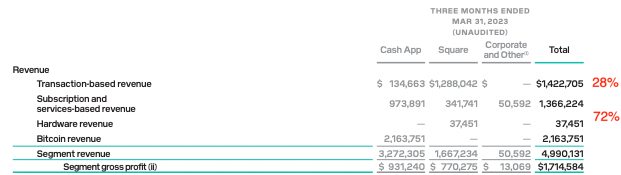

Unlike Mindbody and BILL, transactional revenue dominated their income when going public at 98%. However, that changed dramatically over the years. They're split today at just 28% transactional vs. 72% other. It's worth noting that total revenue in this case incorporates Cash App and Bitcoin. Without either or both of those, transactional is much higher.

Post-publishing update: my friend Samir highlighted that much of Cash Apps transaction revenue rolls into the Subs and Services bucket, whereas one would think on the surface that it would be in the transaction-based revenue. He has a great relevant thread here on "contribution profit."

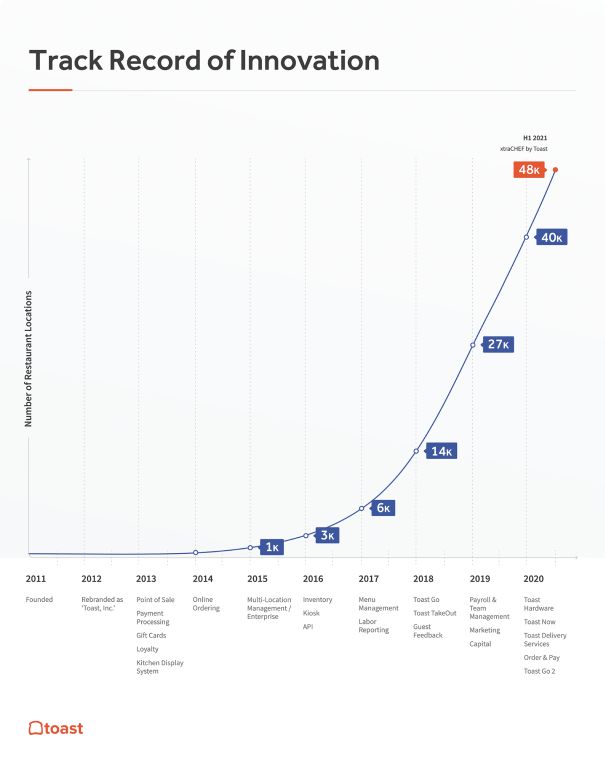

Toast

Toast began with a consumer app that integrated with a restaurants existing POS system. They expanded to restaurant-focused point-of-sale (POS) systems of their own and other capabilities around online ordering, delivery coordination, email marketing, and even payroll and team management. Like Mindbody, Toast was purpose built for their customers. "This suite of software and hardware products is integrated with our financial technology solutions, which includes payment processing and other products such as those provided by Toast Capital."

Here's a shot of their evolution from their S-1:

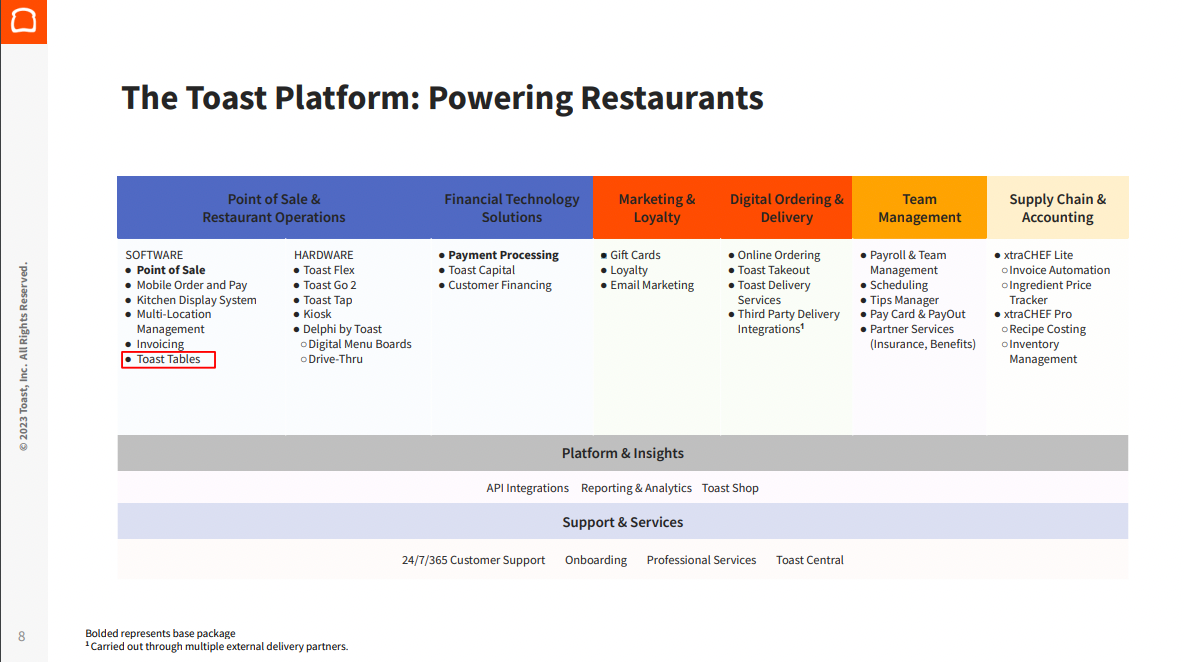

And a more recent shot of their current product suite:

Obligatory flywheel slide:

Toast breaks revenue out by subscription, financial technology solutions, hardware, and professional services. They define financial technology solutions as fees paid by customers to facilitate payment transactions. It also includes fees earned from marketing and servicing working capital loans through their Toast Capital offering.

Similar to PayPal but unlike BILL and Square, Toast revenue split has remained pretty steady since going public, despite adding a lot more software. Revenue was 79% transactional when going public and is currently 82%.

PayPal

PayPal didn't necessarily start with a clear vision of what they wanted to be given its non-conventional start. But an early experiment morphed into a way to beam money around. They essentially started as a company that offered software to facilitate peer-to-peer money transfers and soon graduated to a trusted way to transact between buyers and sellers on eBay. They went all-in on this use case. PayPal was the GOAT fintech, innovating in growth hacks and risk management. They went public early on, were quickly acquired by eBay, and eventually spun out to become a public company again in 2015. It's worth recognizing the impact of living within eBay and its role as a verticalized payment product for the marketplace. Over time, PayPal developed a comprehensive suite of services, including merchant services, cross-border transfers, business and consumer credit, and even fundraising tools. In addition, acquisitions such as BillMeLater ($945m), Braintree ($800m), Xoom ($1b), and Venmo ($26m, well, by Braintree) broadened PayPal's services. Today, there's $40b sitting in PayPal balances which is pretty mind-blowing when you think about it.

Peep 2005 PayPal.com:

Now look at all they offer:

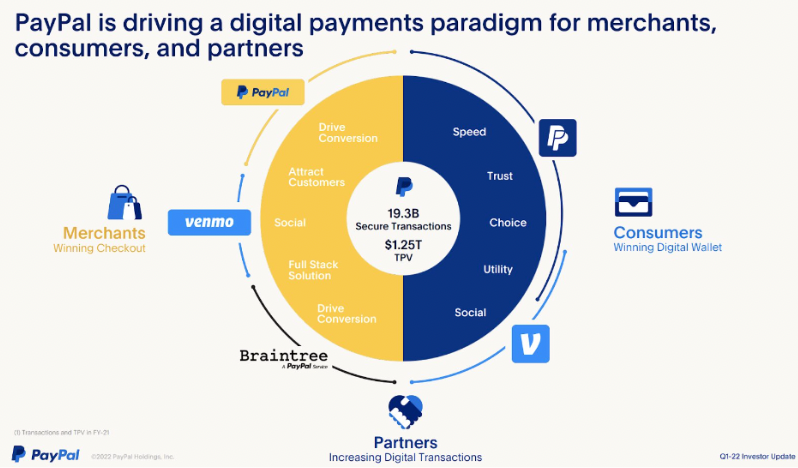

Obligatory flywheel slide:

When PayPal split from eBay, they made $2.80 for every $100 transaction whereas today, it's closer to $1.88. This is mostly due to the rise of P2P and Venmo, as well as a narrowing of take rates from any merchant acquirer across the greater ecosystem. American Express started with nearly 5% take rates but are near 2% today. Many Payments Plus companies will have to fight the headwind of taking less from each transaction each year, but they can make it up with volume, which should grow as they build an ecosystem of products that add additional value to customers.

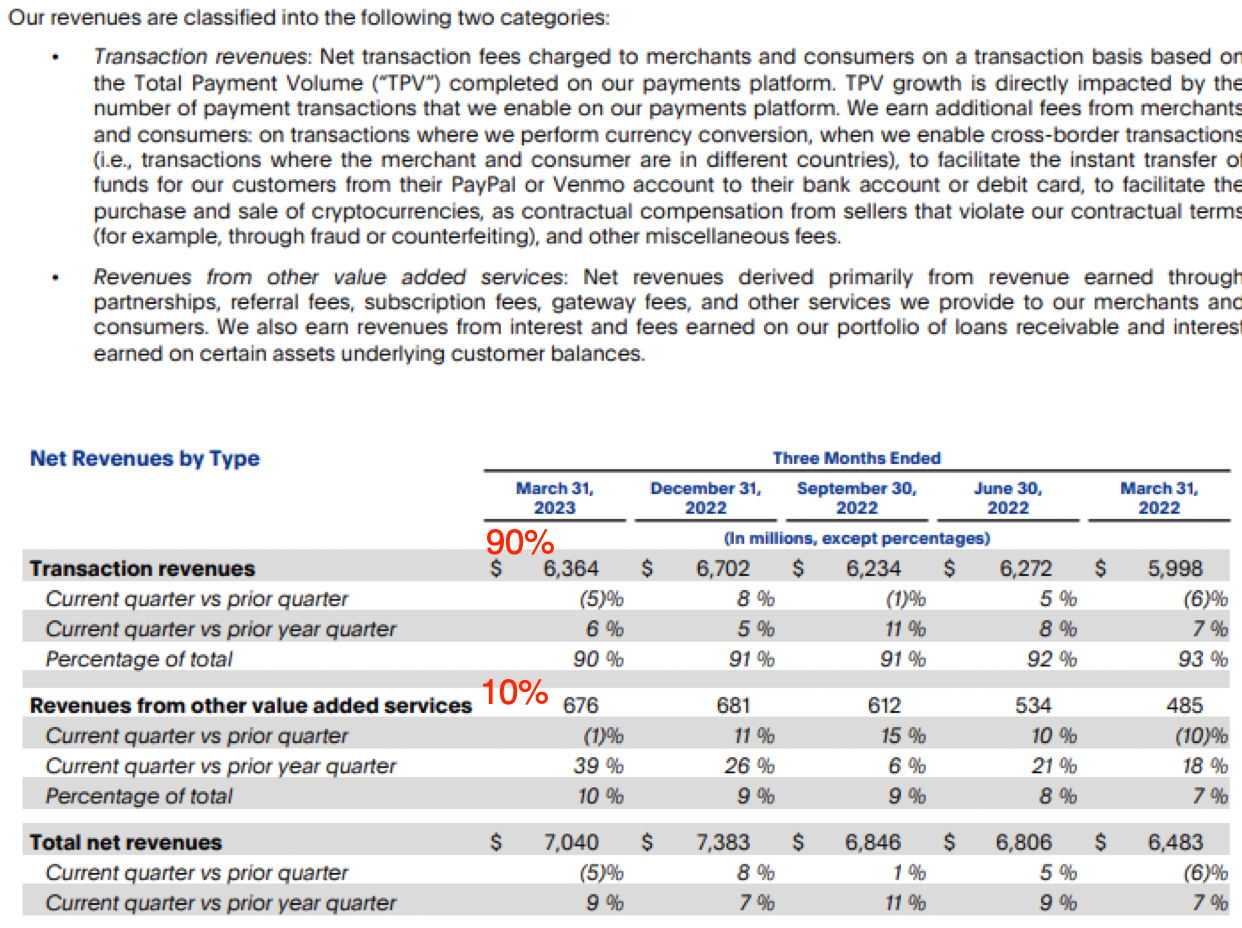

PayPal breaks revenue out by transactional vs. other value added services. Similar to when they originally went public, 90% of the revenue today is still from transactions.

Disclaimer: I'm aware that PayPal doesn't quite fit this category as well as the others. But I wanted to learn more about the fintech goat so, I included it :).

References

- Mindbody S-1

- Mindbody Bessemer memo

- Square S-1

- Square Q1 2023 shareholder letter

- BILL S-1

- BILL 2023 financial results

- Toast S-1

- Toast Q1 2023 financial results

- Toast Inc — Pivot, Growth, IPO and Beyond

- Tidemark: A World Powered by Payments

- PayPal S-1

- PayPal Q1 2023 earnings release

- PayPal Business Breakdowns pod ep